One of the biggest stories of last week was how Vera Bradley, Inc. (NASDAQ:VRA) shares plunged 25% in the week since its latest quarterly results, closing yesterday at US$4.25. It looks like a pretty bad result, given that revenues fell 18% short of analyst estimates at US$81m, and the company reported a statutory loss of US$0.46 per share instead of the profit that the analysts had been forecasting. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. With this in mind, we've gathered the latest statutory forecasts to see what the analysts are expecting for next year.

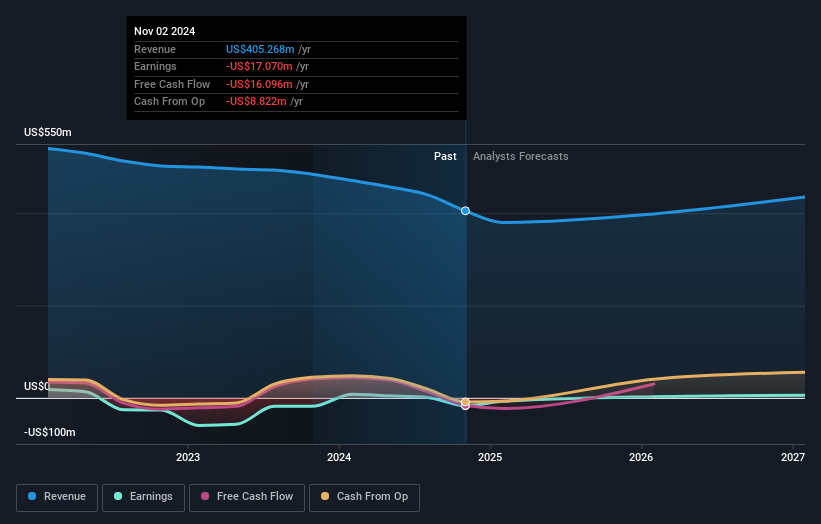

Following last week's earnings report, Vera Bradley's dual analysts are forecasting 2026 revenues to be US$398.5m, approximately in line with the last 12 months. Vera Bradley is also expected to turn profitable, with statutory earnings of US$0.10 per share. Before this earnings report, the analysts had been forecasting revenues of US$442.2m and earnings per share (EPS) of US$0.32 in 2026. From this we can that sentiment has definitely become more bearish after the latest results, leading to lower revenue forecasts and a pretty serious reduction to earnings per share estimates.

The consensus price target fell 32% to US$6.50, with the weaker earnings outlook clearly leading valuation estimates.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Vera Bradley's past performance and to peers in the same industry. One thing that stands out from these estimates is that revenues are expected to keep falling until the end of 2026, roughly in line with the historical decline of 1.4% per annum over the past five years. Compare this against analyst estimates for companies in the broader industry, which suggest that revenues (in aggregate) are expected to grow 6.2% annually. So it's pretty clear that, while it does have declining revenues, the analysts also expect Vera Bradley to suffer worse than the wider industry.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Vera Bradley's past performance and to peers in the same industry. One thing that stands out from these estimates is that revenues are expected to keep falling until the end of 2026, roughly in line with the historical decline of 1.4% per annum over the past five years. Compare this against analyst estimates for companies in the broader industry, which suggest that revenues (in aggregate) are expected to grow 6.2% annually. So it's pretty clear that, while it does have declining revenues, the analysts also expect Vera Bradley to suffer worse than the wider industry.

The Bottom Line

The biggest concern is that the analysts reduced their earnings per share estimates, suggesting business headwinds could lay ahead for Vera Bradley. Unfortunately, they also downgraded their revenue estimates, and our data indicates underperformance compared to the wider industry. Even so, earnings per share are more important to the intrinsic value of the business. The consensus price target fell measurably, with the analysts seemingly not reassured by the latest results, leading to a lower estimate of Vera Bradley's future valuation.

With that in mind, we wouldn't be too quick to come to a conclusion on Vera Bradley. Long-term earnings power is much more important than next year's profits. We have analyst estimates for Vera Bradley going out as far as 2027, and you can see them free on our platform here.

Another thing to consider is whether management and directors have been buying or selling stock recently. We provide an overview of all open market stock trades for the last twelve months on our platform, here.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.