如今,这家香港餐饮品牌转而选择美股上市,最终能否如愿,又是否能吸引到投资者用真金白银投票?

如今,这家香港餐饮品牌转而选择美股上市,最终能否如愿,又是否能吸引到投资者用真金白银投票?Will Hong Kong's dining brand succeed in going public on the US markets this time?

Recently, The Great Restaurant Development Holdings Limited (referred to as 'Yi Pin Chicken Hot Pot') from Hong Kong disclosed its prospectus and plans to list on the Nasdaq in the USA. Previously, the company had submitted a confidential filing to the SEC on September 15, 2023.

The rocky journey of Yi Pin Chicken Hot Pot towards going public can be traced back to 2019, when it submitted a main board listing application to the Hong Kong Stock Exchange under the name 'Yi Pin Development'. The company has updated its prospectus several times since, yet has never successfully listed in Hong Kong.

Now, this Hong Kong dining brand has chosen to list on the US markets; will it finally achieve its goal, and will it be able to attract investors to vote with real money?

Now, this Hong Kong dining brand has chosen to list on the US markets; will it finally achieve its goal, and will it be able to attract investors to vote with real money?

Revenue has continuously declined, raising doubts about ongoing operational capacity.

Public information shows that Yi Pin Chicken Hot Pot is a Chinese restaurant chain based in Hong Kong, specializing in various signature chicken hot pots. Since opening its first hot pot restaurant in Tsuen Wan in 2011, the company currently operates 7 restaurants in Hong Kong, covering commercial areas (namely Mong Kok and Causeway Bay) as well as residential areas (Tsuen Wan, Hung Hom, and To Kwa Wan).

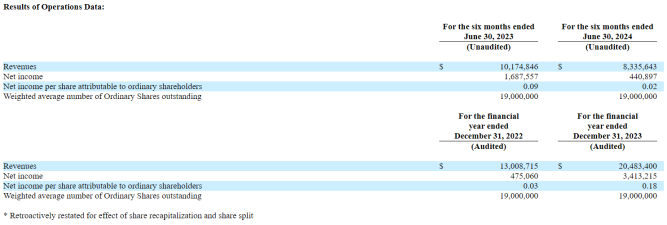

In 2022, 2023, and the first half of 2024, the company's revenues were $13.0087 million, $20.4834 million, and $8.3356 million respectively, with corresponding net incomes of $0.476 million, $3.4165 million, and $0.4439 million.

In the first half of 2024, the company's revenue declined by nearly 20% year-on-year, mainly due to: (i) economic instability affecting market sentiment, leading to consumers being more cautious in their daily spending; and (ii) customers choosing to travel overseas, which includes (a) China, providing affordable restaurant options; and (b) Japan, which has always been one of Hong Kong residents' favorite holiday destinations, especially during this period, with the yen depreciating against the dollar.

At the same time, the company's gross margin also dropped from around 26.7% in the first half of 2023 to about 16.1% in the first half of 2024, mainly due to rising inflation affecting food prices and labor costs.

However, while revenue "shrinks," the company's costs and expenses generally increased. According to Zhito Finance APP, in the same period last year and in the first half of 2024, the company's sales and marketing expenses were approximately $22,000 and $42,000 respectively, accounting for about 0.2% and 0.5% of total revenue for the same period; general and administrative expenses were approximately $0.1 million and $200,000 respectively, accounting for about 0.9% and 2.5% of total revenue for the same period.

In fact, the company submitted its application to the Hong Kong Stock Exchange back in 2019. According to the disclosed prospectus at that time, the company's revenue from 2016 to 2018 was 0.146 billion yuan, 0.165 billion yuan, and 1.74 billion yuan respectively. Based on the current dollar exchange rate (approximately 7.27), the company's revenue in 2022 and 2023 was approximately 94.66 million yuan and 149 million yuan, respectively, indicating that the company's revenue has not only not shown significant growth in recent years but has also experienced a slight decline.

The company admitted in its prospectus that due to operating deficits, questions exist regarding its ability to continue as a going concern. As of June 30, 2024, December 31, 2022, and 2023, the company's working capital deficits were $3.183 million, $3.92 million, and $2.201 million respectively, with positive cash flows generated from operating activities being $0.5868 million, $1.6045 million, and $4.1462 million respectively.

The Hong Kong dining market is performing poorly.

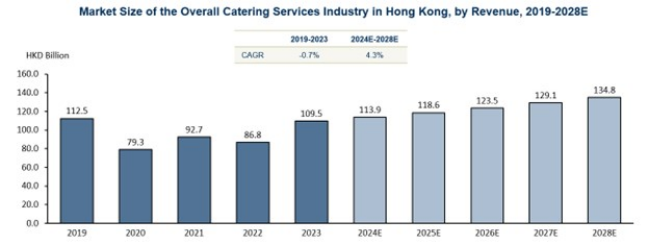

According to the prospectus, due to the pandemic and social control measures among other factors, the Hong Kong dining market has been severely impacted, with the overall market size of the restaurant service industry in Hong Kong experiencing a year-on-year decline of approximately 29.4% from 2019 to 2020. Since 2023, local demand has rebounded, with the recovery of the tourism industry driving the revival of Hong Kong's dining industry, and the market size is expected to reach 109.5 billion Hong Kong dollars in 2023. Looking ahead, the overall market size of the restaurant service industry in Hong Kong is projected to grow at a compound annual growth rate of approximately 4.3% from 2024 to 2028.

It can be seen that the growth of the local Dining market in Hong Kong is slowing down and becoming saturated, while the particularly high operating costs have also led to a crisis of declining profits for local Dining enterprises.

From the performance of the Dining industry in 2024, although the impact of the pandemic has dissipated, the local Dining market in Hong Kong remains bleak. The three main factors leading to a general decline in the performance of local Dining stocks are the consumption of Hong Kong residents in the north, the cautious consumer behavior of local residents, and the changing consumption patterns of visitors to Hong Kong.

According to the interim Earnings Reports disclosed by several listed local Dining companies in Hong Kong, CAFE DE CORAL H (00341) reported a 1.2% year-on-year decline in revenue in the first half of the year, while its net income attributable to the parent company fell sharply by 28.2%. This is also the first decline in revenue for CAFE DE CORAL H since the interim period of the fiscal year 2021 during the pandemic; FAIRWOOD HOLD (00052) saw a 57.26% year-on-year decrease in profit attributable to Shareholders, nearly halving; and TamJai International (02217) reported a 55.8% year-on-year decline in interim profit, down to 36.068 million Hong Kong dollars.

In the face of difficult circumstances, many enterprises, out of necessity, have chosen to expand into the mainland. For example, CAFE DE CORAL H has expanded its store network in the Greater Bay Area, and the number of its stores in mainland China has now exceeded its store count in Hong Kong; Tsui Wah Restaurants once had as many as 43 restaurants in the mainland market; as of August 24, TAI HING GROUP's subsidiary, Min Wah Ice Room, also had 28 stores in the mainland.

In contrast, Yi Pin Chicken Hotpot has not only refrained from expanding into the mainland but has even seen no new developments in its store opening plans in Hong Kong. As early as 2020, the company stated that it planned to open five new restaurants in Hong Kong residential areas during the three years ending December 31, 2023, and aimed to open six hotpot restaurants at a pace of one every six months, but as of the latest disclosure date, the number of restaurants under the company has not changed compared to 2018.

Can abandoning Hong Kong for the USA fulfill the dream?

Due to various factors such as policies and systems, overseas markets like the stock markets in the USA have become a popular choice for many enterprises to ' flock' to for listing.

According to Zhitong Finance APP, the listing conditions for US stocks are relatively lenient, and the requirements from the NYSE and Nasdaq for listing companies are not as strict as those for Hong Kong and A-shares. As an international market, it also has a higher appeal to capital. For companies with financing needs or looking to expand overseas, choosing to list overseas helps broaden financing channels and enhances the company's international competitiveness and brand influence.

Data shows that in the first half of this year, 29 Chinese concept stocks have been listed in the USA, among which 24 went public through IPOs, raising about 1.95 billion USD in total; 4 went public via SPACs, and 1 switched boards.

However, it should be noted that Yi Pin Ji Bao Hotpot does not belong to the popular industries such as Internet and Technology favored by US stock investors. As a company whose operations are limited to Hong Kong, if Yi Pin Ji Bao Hotpot chooses to list in Hong Kong, it may naturally receive more recognition from local investors. The current decision to abandon Hong Kong in favor of the USA may also be a reluctant choice due to multiple failed attempts to list on the Hong Kong stock market.

However, going public in the USA is not necessarily a smooth path. According to statistics from Huayi Capital, the amount raised in Chinese concept stock IPOs in the first half of this year was relatively low, with an average raised amount of 81 million USD, of which only 2 companies raised over 100 million USD, while 19 companies had a first-time fundraising amount of less than 10 million USD, accounting for as much as 79%. Furthermore, 3 companies raised only 5 million USD;

From the financial situation a year prior to listing, only 7 companies had a revenue exceeding 100 million USD in the past year, while 8 companies had a revenue of less than 10 million USD, accounting for 27.5%. Most companies' revenues were concentrated between 10 million and 100 million USD.

Meanwhile, over half of the Chinese concept stocks experienced a decline in their stock prices on their first day of listing, such as the Hong Kong-based caviar supplier, Tsinghua Unigroup (TWG.US), which dropped 51.50% on its first day, and the toner cartridge exporter and seller, Planet Image International (YIBO.US), which fell 30.25% on its debut.

It can be seen that as the Chinese concept stocks warm up to US listings, most of the listed companies are still low-revenue, small-sized entities, and the stock price performance after listing is not optimistic. With poor fundamental performance compounded by stagnant store expansion, Yi Pin Ji Bao Hotpot's path to listing in the USA may not be so simple.