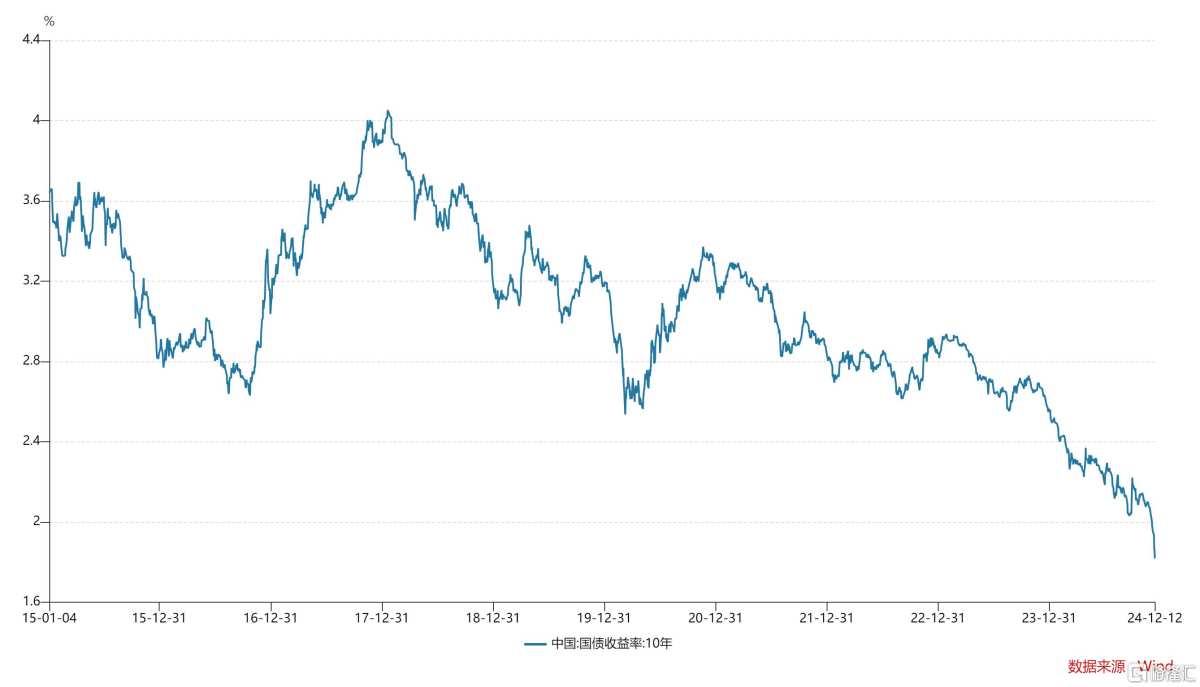

自2020年12月以来,10年期国债收益率从3.27%逐步下滑至2%以下。近一月,10年期国债收益率先后下破2.0%、1.9%、1.85%等关口,整体降幅近30bp。

自2020年12月以来,10年期国债收益率从3.27%逐步下滑至2%以下。近一月,10年期国债收益率先后下破2.0%、1.9%、1.85%等关口,整体降幅近30bp。Will the "debt bull" market continue?

The yield on the 10-year Treasury bonds continued to decline this week after historically breaking below 2% last week, reaching a new historic low.

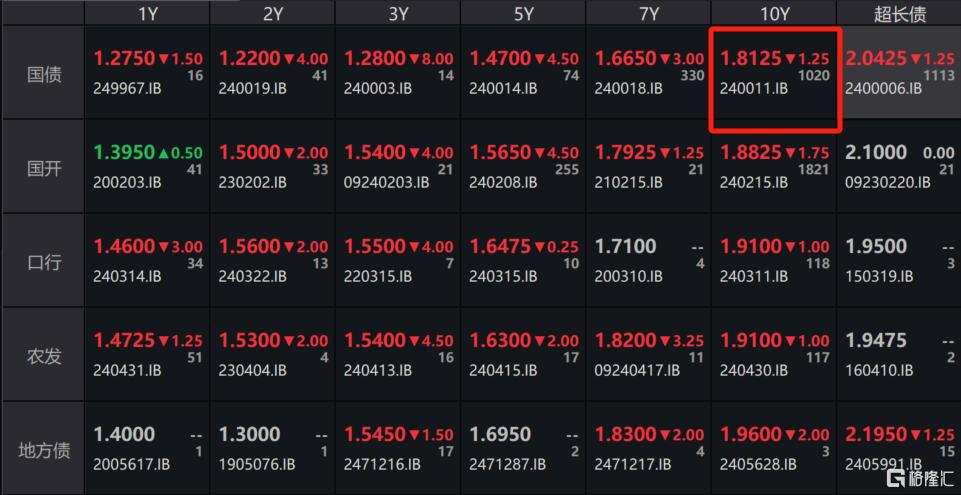

On December 12, the yield on the 10-year Treasury bonds further decreased to 1.8125%, setting another historic low. The yields on Treasury bonds of other maturities also fell.

Since December 2020, the yield on the 10-year Treasury bonds has gradually declined from 3.27% to below 2%. In the past month, the yield has successively fallen below 2.0%, 1.9%, 1.85%, and other levels, with a total decrease of nearly 30 basis points.

Since December 2020, the yield on the 10-year Treasury bonds has gradually declined from 3.27% to below 2%. In the past month, the yield has successively fallen below 2.0%, 1.9%, 1.85%, and other levels, with a total decrease of nearly 30 basis points.

Data statistics Range: 2015/1/4-2024/12/12.

The yield on the 10-year Treasury bonds to some extent represents the risk-free return in the domestic market, and there is an inverse relationship between Treasury bond yields and Treasury bond prices. A decline in Treasury bond yields means an increase in bond prices.

Today, the 30-year, 10-year, 5-year, and 2-year government bond futures have once again risen, reaching new highs during the session. As of the close, the main contract for the 30-year government bond futures rose by 0.1%; the 10-year government bond futures closed up by 0.12%; the 5-year and 2-year government bond futures rose by 0.13% and 0.07% respectively.

Recently, the rise of bond ETFs has also been considerable, with several bond ETFs reaching new highs. Among them, Convertible Bonds ETF and HFT SSE Investment Grade Convertible Bond and Exchangeable Bond ETF have increased by 14.32% and 11.04% over the past 60 days.

How to understand the decline in government bond yields?

On December 2, the 10-year government bond yield fell to 1.98%, breaking below the critical 2% level, and continued to decline, reaching 1.81% by December 12.

Soochow Securities believes that the repeated new lows in the 10-year government bond yield are the result of the combination of three factors:

First, since early December 2024, expectations for a reserve requirement ratio cut have been brewing. At a meeting on September 24, the central bank governor Pan Gongsheng stated that a cut in the reserve requirement ratio would be timely within the year. 2024 will pass, and coupled with the recent substantial issuance of special bonds to replace existing hidden debts, the market expects the reserve requirement ratio cut aimed at supplementing the liquidity of the banking system to be implemented soon.

Secondly, the two initiatives of the market interest rate self-discipline mechanism announced on November 29 aim to guide broad interest rates downward. These initiatives mainly address bottlenecks in the monetary policy transmission process, such as high-interest non-bank interbank deposits and long-term deposit agreements for bank corporate clients. As a result, part of the allocation demand has shifted from deposits to Bonds.

Thirdly, based on the judgment that interest rates may decline in 2025, market participants are engaged in "grabbing allocations".

Feng Lin, executive director of the research and development department at Dongfang Jincheng, believes that the main reason for the continuous decline in the yield of 10-year government bonds may be the prevailing bullish sentiment in the current bond market, the persistent strength of the market, and the ongoing end-of-year allocation rush.

Will the "debt bull" market continue?

Since the beginning of this year, the asset shortage situation has continued, with the yields on 10-year and 30-year government bonds continuously declining, which has led the bond market to experience an epic "bond bull" market.

Approaching the end of the year, the demand for long-term and short-term interest rate bond allocations from small and medium-sized banks, insurance institutions, and asset management institutions is strong, which often drives government bond yields down.

Looking ahead to 2025, the demand from banks and insurance institutions for bond allocations may continue to increase, the growth rate of wealth management and Fund sizes becomes more uncertain, and the central bank's purchase of government bonds for monetary release will increase demand in the bond market, exacerbating the asset shortage. Furthermore, the initiative to optimize self-discipline management of non-bank interbank deposit rates means that interbank deposit rates tend to decline, continuing the downward trend in interest rates, under the comparative advantage, paying attention to the allocation opportunities in interbank certificates of deposit and high-grade duration Bonds.

Guolian Securities pointed out that from the yield curve perspective, the current curve shows a bullish flat trend, with further steepening space, and under the expectation of reserve requirement ratio cut, the certainty of short-term Bonds may be higher than that of long-term Bonds. In terms of variety strategy, the yield of interbank certificates of deposit may have some downward space, and amidst the backdrop of debt conversion, opportunities exist in urban investment Bonds.

Guolian Securities expects that the supply-demand gap in the bond market may widen compared to this year in 2025, while broad interest rates remain on a downward trend.

China Great Wall Securities believes that although the overall rate cuts and reductions in reserve requirement ratios next year are likely not to be weaker than this year, under the extremely strong "buying liquidity," the foundation of the bull market in bonds will not easily change, at least it will be difficult to change in the first half of the year. After a country's interest rate falls to 2.0% or below, the rate cuts in policy interest rates may have diminishing marginal effects on the decrease of risk-free rates, therefore the overall trend in the bond market next year may be "the trend remains, but the effect diminishes."