11月特朗普在美国总统大选中获得决定性胜利引发各类资产的“特朗普交易”。美国股市因减税和放松监管的预期而大幅上涨,12月早期三大股指均创出历史新高。

11月特朗普在美国总统大选中获得决定性胜利引发各类资产的“特朗普交易”。美国股市因减税和放松监管的预期而大幅上涨,12月早期三大股指均创出历史新高。MetalsFocus released the December 2024 Precious Metals Monthly Report.

According to the Zhitong Finance APP, MetalsFocus has released the December 2024 Precious Metals Monthly Report, stating that due to various cumulative factors, investor interest in precious metals should rise from now until 2025. In light of this, MetalsFocus's forecast for precious metal prices remains unchanged, predicting that gold prices will reach new historical highs in the coming months, which will drive silver prices higher.

Current Status and Outlook of the Macroeconomy.

In November, Trump's decisive victory in the US presidential election triggered a range of assets in the 'Trump trade.' The US stock market surged significantly due to expectations of tax cuts and deregulation, with all three major stock indices reaching historical highs in early December.

In November, Trump's decisive victory in the US presidential election triggered a range of assets in the 'Trump trade.' The US stock market surged significantly due to expectations of tax cuts and deregulation, with all three major stock indices reaching historical highs in early December.

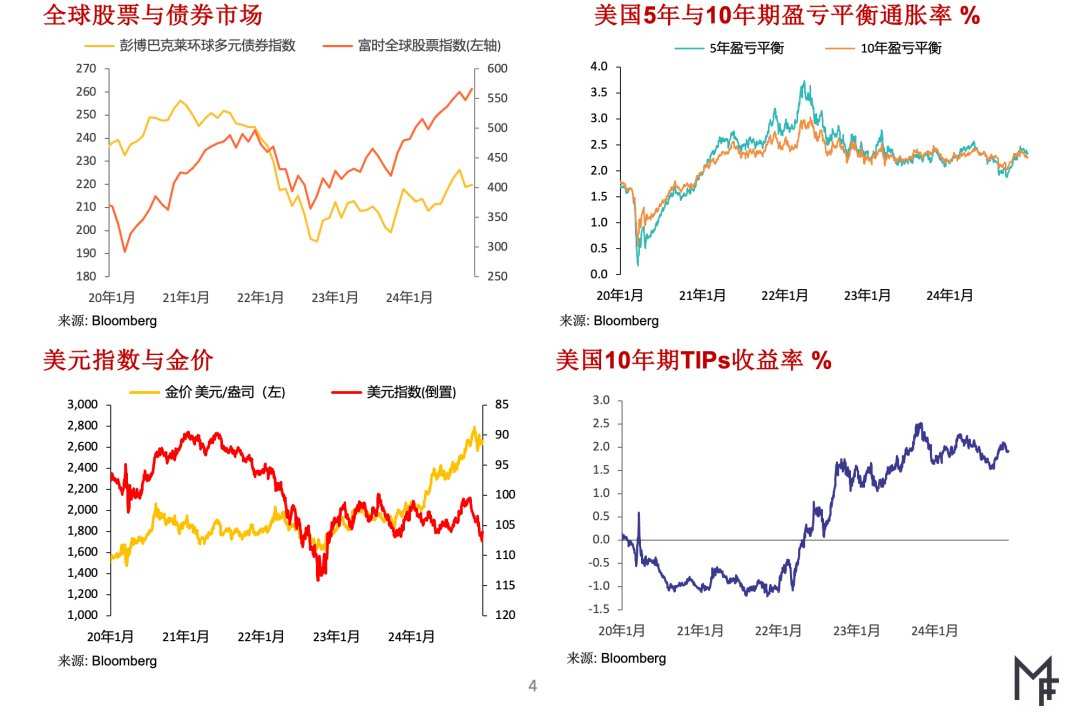

Due to increasing expectations that Trump will implement economic and political measures such as raising tariffs (which will lead to rising inflation) during his second term, the dollar and US Treasury yields soared sharply after the US election, resulting in a significant shift in the market's expectations for interest rates in 2025. In September, the market expected rates to drop to as low as 2.8% by the end of 2025, but currently, the Federal Funds Futures prices indicate that rates will be 3.7% by the end of 2025, which is more hawkish than its own interest rate forecast (range of 3.1%-3.6%).the Federal Open Market Committee

Aside from the 'Trump trade,' the strong dollar also reflects that other major reserve currency countries are busy dealing with their own challenges. Specifically, the ongoing political turmoil in Germany and France is increasingly pressuring the euro, with the deadlock in France's budget proposal causing the country's bond yields to surpass those of Greece for the first time.

The significant increase in the US dollar and US Treasury yields has led to a sell-off in Precious Metals. In the first half of November, gold prices fell by 9%, but have since recovered most of the losses due to the escalation of the Russia-Ukraine conflict. The trend for white Precious Metals is similar but has seen a larger drop than gold.

Looking ahead, multiple rate cuts in 2025 are expected to lead to lower Bond yields. Furthermore, the current market prices for Precious Metals have already reflected expectations for a significant slowdown in rate cuts in 2025, thus the Fed's cautious approach to rate cuts may have limited impact in the future.

Current Situation and Outlook of the Macroeconomy

Current Situation and Outlook of the Gold Market

After reaching a historical high of $2,790 per ounce at the end of October, gold prices fell sharply due to the surge in the US dollar and US Treasury yields, dropping a total of 9% (losing $250) to a new two-month low of $2,537 per ounce by November 14. Following this, gold quickly rebounded to above $2,700 per ounce due to intensified tensions in Russia and Ukraine, but this rise was short-lived, turning downward again after Israel and Lebanon signed a ceasefire agreement. At the time of writing this report, gold prices were fluctuating within the range of $2,600-$2,650 per ounce.

As mentioned in the previous 'Macroeconomic' section, market expectations that Trump's economic policies will drive up inflation have limited the Fed's room to cut rates, with Trump's victory being a key factor leading to the sell-off of gold in November.

Despite facing intensified bearish pressures in the short term, gold prices remain strong, finding good support near $2,600 per ounce after dropping to a two-month low. This price level has increased by 26% since the beginning of the year and remains at a high level. Essentially, this reflects the numerous economic and political uncertainties, giving investors ample reason to continue holding gold as an effective diversification tool in their investment portfolios.

In this context, the recent decline in gold prices may mainly be due to tactical investors reducing their long positions in Gold. In contrast, the willingness of investors to short Gold remains subdued, and in fact, some investors holding short positions have taken the opportunity of the price correction to cover their positions.

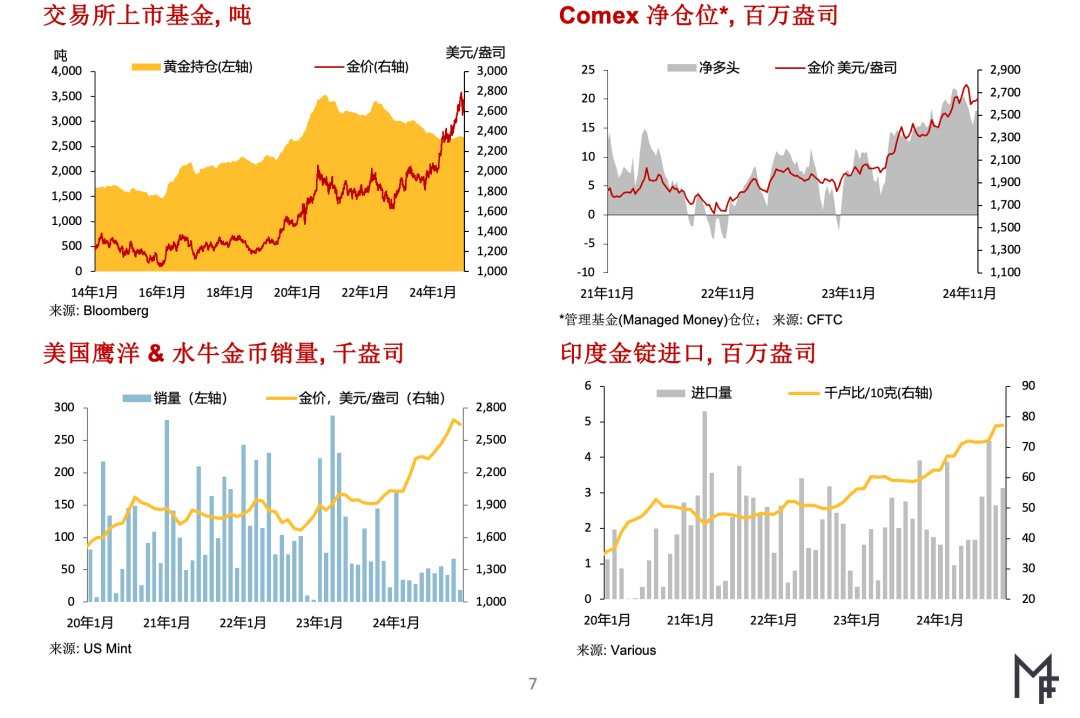

At the same time, the net purchases of gold by global official sectors remain at a high level. Although gold prices have risen to record highs, countries like India, Turkey, and Poland that typically buy gold have continued to steadily increase their holdings in October.

Looking ahead, MetalsFocus maintains its previous forecast. MetalsFocus believes that although short-term gold prices may face downward pressure, even if the current market expects fewer interest rate cuts in 2025, the interest rate reduction cycle in the USA will continue, which should benefit gold. The combination of interest rate cuts and current geopolitical conflicts, as well as worries about the USA's high debt levels, escalating political turmoil in Europe, and the continuous upgrade of trade war threats, will continue to support gold investments in the medium to long term.

However, MetalsFocus expects gold prices to begin to decline starting in the second quarter of 2025, as by then, most bullish factors will have been reflected in the gold price, but it is still expected to remain at relatively high levels by the end of the year.

After gaining a clear understanding of the economic policies following Trump's administration, concerns about the USA's high debt levels may further intensify. In Europe, France and Germany may continue to face political uncertainty in the coming months.

Despite the recent ceasefire agreement between Israel and Hezbollah, geopolitical tensions are unlikely to dissipate quickly.

Current Status and Outlook of the Gold Market

In China, during November, the Fill Price of gold on the Shanghai Gold Exchange was at a discount compared to the London market, with a daily average discount of $17/ounce. At the same time, the physical outflow volume from the exchange declined by 25% year-on-year and 8% month-on-month to 99 tons. This reflects the impact of high gold prices along with weak consumer confidence. Retail investment demand for gold has also decreased, though the decline is more moderate due to a rapid rebound in gold prices after a significant correction in the first half of November, which supported some investors' confidence.

In India, due to the current wedding and festival season causing a pullback in gold prices, the purchase of gold has slightly increased. In November, the average discount of domestic gold prices against landed cost narrowed from $15 per ounce in October to $12 per ounce. The official gold import volume in October also rose moderately compared to the previous month, reaching 97 tons. Due to large import volumes during the summer, India's gold imports have approached the total import volume for 2023 in the first ten months of this year.

In Turkey, domestic gold prices continue to rise, and physical gold demand in November continues to strengthen. The strengthened demand combined with limited supply (due to government-mandated monthly import quotas for gold) resulted in Turkish domestic gold prices trading at a premium of $100-130 per ounce over international gold prices for most of the month. In the last few days of November, as gold prices began to consolidate, the interest of domestic residents in purchasing gold decreased, leading to a reduction in the premium to $60-75 per ounce.

In Europe, in terms of net volume, European retail investment demand for gold continues to recover from a low base. MetalsFocus recently conducted field research in Germany and found that the recovery in demand is mainly attributed to the increased interest from investors in small gold bars (especially 10-gram and 1-gram bars), while demand for larger gold bars and coins lags behind. Individual investors slowing down profit-taking has also driven an increase in demand for newly minted gold products.

Regarding gold supply from minerals, Newmont Corporation has agreed to sell its Musselwhite and Élénore mines. Orla Mining will acquire the Musselwhite mine located in Ontario for no more than $0.85 billion. Dhilmar Limited will acquire the Élénore mine located in Quebec for $0.795 billion. It is expected that through these two transactions and several other asset disposal agreements recently reached, Newmont Corporation will generate total revenue of $3.6 billion.

Risk factors for price forecasting: In terms of upward risk for gold prices, a sharp escalation of geopolitical tensions or a more dovish stance from the Federal Reserve could significantly boost gold investment. Growing concerns over the level of US government debt will also give global central banks and institutional investors ample reason to increase their gold allocations. On the downside, an inflationary spiral and delayed interest rate cuts could suppress gold prices.

Current status and outlook of the gold market.

Current status and outlook of the gold market.

Current Status and Outlook of the Silver Market

After reaching a twelve-year high of $34.90 per ounce on October 22, silver prices began to fluctuate and decline, accelerating downwards after the USA elections. On November 14, the silver price hit a two-month low of $29.65 per ounce, while gold prices also reached a monthly low on the same day. Subsequently, silver prices quickly recovered to the $30 mark, fluctuating within the range of $30-$31.5 per ounce until early December.

Similar to the situation in previous months, silver prices in November followed the trend of gold prices. A clear example is that the gold/silver price ratio fluctuated between 83:1 and 88:1 during the month, still within the dominant volatility range of 80:1 to 90:1 since 2023.

Silver has dual attributes of Precious Metals and Industrial Metals, and the decline in prices of both after the USA elections has resulted in a severe dual impact on it. On one hand, many recent Bearish factors (as mentioned in the 'Gold Market' section) have affected silver.

Similar to the situation with gold, tactical long investors taking profits have also triggered a decline in silver prices. In late November, the total long position in silver futures held by managed funds on CME Group had decreased by 31% from the October highs, while total short positions had increased, although the absolute quantity remains low due to the low base. In contrast, the total holdings of silver ETPs (Exchange-Traded Products) in November only saw a slight decrease of 1% compared to the previous month, with investors mainly being long-term individual investors, making the holdings stickier.

Looking ahead, although the economic policies proposed by Trump will suppress the global economic growth outlook, the industrial demand for silver is still expected to remain strong in 2025, while silver supply will face a significant shortfall for the fifth consecutive year compared to demand. However, the existing above-ground stock of silver remains large and will continue to be so next year. If there are no signs of tight physical silver supplies, MetalsFocus doubts that investors will be able to feel excited about silver's strong fundamentals.

It is expected that silver prices will continue to follow gold prices (the main factors influencing investor sentiment in the gold market are macroeconomic factors and geopolitical developments). Therefore, MetalsFocus maintains its forecast that silver prices (and gold prices) will peak in the first quarter of 2025. Once the reasons for investing in gold and silver begin to weaken in late 2025, silver prices are likely to come under pressure.

Current Situation and Outlook of the Silver Market

Continuing the trend of previous months, US retail investment demand for Silver remained weak during November. As stated in the October monthly report, many silver investors in the USA tend to favor the Republican Party, and Trump's victory may strengthen their expectations that the new government can 'better' manage US political and economic affairs, which will lead to a corresponding decline in the demand for defensive assets like silver. In the short term, the stock market reaching record highs, along with the surge in cryptocurrency prices, may also shift individual investors' interest from silver to other assets.

After a 10% drop in domestic silver prices, the demand for silver related to festivals and weddings in India surged in November. At the same time, investment demand remained strong, particularly notable is that after a moderate increase in 2022-2023, funds accelerated inflow into Indian Silver ETPs in 2024, with total holdings skyrocketing 170% to over 1,100 tons. Against this backdrop, after officially importing about 6,900 tons of silver in the first ten months, it is estimated that India imported 400-500 tons of silver in November.

Regarding industrial demand for silver, partly due to strategic inventory management by industrial enterprises before the year's end, demand slowed in November. Within the photovoltaic industry, after successfully introducing the non-owner grid technology in the fourth quarter, the amount of silver filling per watt of electricity generated further declined. The reduction in silver filling, combined with the slowing growth rate of global photovoltaic installed capacity, has led to December's silver powder order quantities from industry enterprises falling below expectations. In other industrial sectors, although the sales of consumer electronics are steadily rising with the large-scale launch of new AI-related products, supply chain manufacturers have prepared sufficient inventory for the year's end sales peak.

In terms of supply, Aya Gold and Silver has reduced the 2024 production guidance for its Zgounder mine located in Morocco. The mine is undergoing an expansion project but encountered issues during the trial production phase of the processing plant. Aya currently expects the silver production of this mine in 2024 to be between 1.6 million and -1.8 million ounces, significantly lower than the original production guidance median of 2.9 million ounces.

Price prediction risk factors: Similar to Gold, the main risk factors for upward silver prices include geopolitical risks and a dovish stance from the Federal Reserve (with the former having a greater impact).

Current Situation and Outlook of the Silver Market

Current Status and Outlook of the Silver Market

Current Status and Outlook of the Platinum Market

In November, the opening price of Platinum was $994 per ounce, briefly touching a monthly high of $1,007 per ounce on the same day. After reaching a high of $1,050 per ounce in late October, driven by the rise in Gold and Palladium, Platinum prices continued to fall. By mid-November, the Platinum price dropped to $930 per ounce, but later rebounded to above $970 per ounce as Gold prices surged sharply due to escalating tensions in Ukraine and the Middle East. The upward momentum of Platinum and Gold reversed as investors took profits, and when a ceasefire agreement was reached on November 27, the Platinum price fell to $925 per ounce, the lowest since early September. At the end of the month, Platinum closed at $950 per ounce.

MetalsFocus has lowered its price forecast for Platinum in 2025. However, considering the supply shortage of physical Platinum, MetalsFocus still maintains an optimistic outlook on the long-term prospects for Platinum prices. In the short term, due to ample above-ground stocks of Platinum and prices maintaining a range-bound trend, the upside potential will be limited. Given that Platinum ETP holdings exceed 3 million ounces, approaching new highs may trigger profit-taking by investors, hindering further increases, making it difficult to predict when Platinum prices will break upwards. For reference, Palladium prices only effectively fell below $1,000 per ounce after ETP holdings fell below 1 million ounces (about two-thirds lower than the historical peak).

In November, the total holdings of Platinum ETPs globally increased by 2% (an increase of 0.078 million ounces) to 3.297 million ounces. Unlike the usual pattern where holdings in a specific region dominate the changes in global total holdings, the holdings of Platinum ETPs across various regions increased moderately in November. Fund inflows mainly occurred in the early part of the month when Platinum prices were above $950 per ounce. For the entire year of 2024, there is a moderate positive correlation (correlation coefficient of 0.55) between Platinum ETP holdings and Platinum prices, showing that ETP investors follow trend operations, which is different from other investors who trade within a range (selling when prices are close to or above $1,000 per ounce, and buying when close to or below $900 per ounce).

At the beginning of November, the net long position in CME Platinum Futures held by managed funds was 1.092 million ounces, but by the end of the month it had sharply dropped to 0.348 million ounces, with a net sale of 0.743 million ounces during this period. Compared to the net long position of 1.461 million ounces at the end of October, the decline is even greater. The significant decrease in net long positions was mainly due to an increase of 0.56 million ounces in total short positions during November, with nearly half established in the first week on a speculative basis, shorting as Platinum prices approached $1,000 per ounce.

Current Status and Outlook of the Platinum Market

After a significant increase in August and September, the total net import volume of Platinum in mainland China and Hong Kong in October decreased to 0.117 million ounces, about half of the average monthly import volume for this year. The reasons for the decline in import volume may include that the previously imported Platinum is sufficient to meet demand, and the average price of Platinum in October ($1,001 per ounce) rose to a new high since May. Since 2022, China's monthly Platinum import volume has shown a moderate to strong negative correlation with Platinum prices (correlation coefficient of -0.60), indicating that importers buy when prices are low and reduce imports when Platinum prices rise above $1,000 per ounce.

Turning attention to the automotive industry's demand for Platinum, MetalsFocus estimates that due to a challenging political environment, there will be greater differentiation in the trends of automotive power systems in different regions globally. In Europe, during the first week of implementing the new legislation, the European Commission has allocated €4.6 billion ($4.9 billion) from the innovation fund to fund the research and development of net-zero emission technologies, electric vehicle manufacturing, and renewable hydrogen energy development. Regarding the automotive industry's demand for Platinum, this measure has a double-edged sword effect. The significant increase in electric vehicle production, expected to reach 16% of total global automobile production by 2025, will lead to a 4% decrease in Europe's demand for Platinum (to 0.983 million ounces). However, in the medium to long term, there are also some factors that could positively impact Platinum demand, including investments in hydrogen production that will promote the development of hydrogen transportation solutions. For example, Stellantis and Renault have announced plans to produce 3,200 hydrogen fuel cell light trucks by 2025.

Anglo American's subsidiary Anglo American Platinum South Africa (AASA) sold a 6.6% stake in Anglo American Platinum for approximately $0.527 billion, resulting in a total sale of 17.5 million shares at a price of 548 South African Rand per share. Anglo American is implementing a strategy to streamline its asset portfolio and increase the free float of Anglo American Platinum shares to complete its corporate spin-off by mid-2025, and this share sale transaction is part of that strategy.

Price prediction risk factors: After former President Trump takes office, the electric vehicle tax credit may be abolished, benefiting the rise in demand for traditional vehicles. On the other hand, if certain provisions of the Inflation Reduction Act are repealed, this could suppress demand in the hydrogen economy sector and investor confidence in the strengthening of Platinum, dragging down Platinum prices.

Current Status and Outlook of the Platinum Market

Current Status and Outlook of the Platinum Market

Current Status and Outlook of the Palladium Market

Similar to the trend of Platinum prices, at the beginning of November, Palladium prices also declined from the October high of $1,248/ounce (at that time, concerns over Russian Palladium supply triggered a short squeeze, pushing up Palladium prices) and fell for 11 out of 12 days. The opening price of Palladium in November was $1,112/ounce, reaching a monthly high of $1,142/ounce on the same day, and then continued to decline, hitting a monthly low of $921/ounce on the 14th, briefly reaching parity with Platinum for the first time since early October. Afterward, Palladium prices significantly rebounded to $1,047/ounce but failed to stabilize above $1,000, fluctuating narrowly within the range of $960-$1,000/ounce for the remainder of the month. At the end of the month, Palladium prices closed at $983/ounce, only $30 above Platinum.Short Squeeze

MetalsFocus's Palladium price forecast remains unchanged.

In November, the total holdings of global Palladium ETPs increased by 3% (an increase of 0.026 million ounces) to 0.911 million ounces, peaking at 0.954 million ounces on the 22nd, the highest level since October 2018 (when Palladium prices just broke above $1,000/ounce and then soared). The total holdings continued to rise after the increase in October, having risen by 53% (increased position of 0.315 million ounces) since the beginning of the year. Due to several downward revisions of electric vehicle production expectations last year, many investors (almost all of whom are USA Palladium fund investors) view Palladium as an asset to hedge against the trend of automotive electrification.

From early November to the end of the month, the net short position held by managed funds in CME Palladium futures rose from 0.27 million ounces to 0.663 million ounces, indicating that after the short squeeze in October (when the net short position fell drastically to 0.177 million ounces), investors re-established short positions. For background information, the average number of net short positions held by investors in 2024 is 1.069 million ounces. On November 19, the number of net short positions reached a monthly high of 0.789 million ounces, and in the last week, the total number of short positions declined, possibly indicating a stabilization of short positions, with investors' bearish sentiment weakening and expectations that Palladium prices are unlikely to fall further from the current level.

In October, the total net import volume of Palladium from mainland China and Hong Kong turned negative for the first time in history at 0.017 million ounces, with Hong Kong exporting 0.042 million ounces, the highest level since May 2010. Similar to the situation with Platinum, the import volume of Palladium in China is negatively correlated with Palladium prices, although the negative correlation coefficient is relatively low at -0.36.

Current Situation and Outlook of the Palladium Market

After Trump's victory, the electrification transformation of the auto industry in the USA may face significant obstacles during his second term, which is Bullish for internal combustion engine vehicles and supports the demand for Palladium. The repeal of certain provisions in the Inflation Reduction Act may lead to a 15%-20% reduction in the market share of electric vehicles by 2030 compared to current projections. Based on the automotive production forecast released by data analysis and consulting firm GlobalData for the third quarter of 2024 (which does not consider the potential impact of the repeal of certain provisions of the Inflation Reduction Act), the demand for Palladium will increase by 0.23 million ounces in 2025. Although the production of internal combustion engine vehicles may continue to rise, MetalsFocus still expects global Palladium demand to decline by 3% in 2025, to 8.3 million ounces.

Some regulations set by the EPA in the USA, especially those concerning emissions and fuel economy, are also likely to be repealed, including the repeal of the exemption for California's Advanced Clean Cars Regulation II (which has stricter emission standards than federal standards). Given that MetalsFocus assumes an increase in Palladium loading as new regulations are implemented when forecasting Palladium demand, the repeal of some regulations may further decrease Palladium demand.

On the supply side, Norilsk Nickel has raised its production guidance for platinum group metals in 2024, citing reasons including improved operational efficiency, sustained increases in mining output during the first nine months of 2024, and the completion of major repairs at its Nadezhda smelter. The Palladium production guidance has been adjusted upward from the previous 2.3 million-2.5 million ounces to 2.6 million-2.7 million ounces, while the Platinum production guidance has also been raised from the previous 0.5 million-0.6 million ounces to 0.6 million-0.7 million ounces. In the first nine months of 2024, the total production of Palladium and Platinum by Norilsk Nickel was 2.2 million ounces and 500,000 ounces, respectively.

Price Forecast Risk Factors: Significant tariff increases after Trump took office may drive up inflation, lead to rising interest rates, and suppress global auto demand, thereby pressuring Palladium demand and prices.

Current Situation and Outlook of the Palladium Market

Current Situation and Outlook of the Palladium Market

Current Status and Outlook of the Rhodium Market

The opening price of rhodium in November (Sell Price) was $4,675 per ounce, which was also the monthly high. The rhodium price remained stable until November 13, after which it dropped to the monthly low of $4,575 per ounce on the 27th, and closed at that price by the end of the month.

The average price of rhodium so far in 2024 is about $4,600 per ounce. In light of this, MetalsFocus has raised its average price forecast for rhodium for 2025. The price of rhodium is very stable at the current price level, and once it falls below this level, it receives strong support. It is expected that the physical rhodium supply shortage in 2025 will be 0.028 million ounces, which is likely to drive rhodium prices higher. However, in the medium to long term, an oversupply is expected, which will continue to weaken investor confidence.

In October, the total net import volume of rhodium in mainland China and Hong Kong rose to 0.031 million ounces, 33% higher than the average monthly import volume for the year to date. By the end of October, the total import volume had increased by 41% to 0.236 million ounces, setting a new high for the same period since 2016. Over the past three years, the negative correlation coefficient between China's rhodium import volume and rhodium price has been -0.51, which is between platinum (-0.60) and palladium (-0.37), highlighting the continuous speculative buying of these three platinum group metals by Chinese Institutions.

It is expected that the global automotive industry's demand for rhodium will decrease by 2% in 2025, falling to 0.944 million ounces. Although the production of hybrid cars is expected to grow by 17% in 2025, reaching 23.4 million units, the corresponding rhodium demand from hybrid car manufacturers will rise by 14%. However, due to a 7% decrease in the total production of internal combustion engine vehicles, down to 55 million units, the total rhodium demand in the automotive industry will still decline.

Price prediction risk factors: Similar to the situations with platinum and palladium, the potential increase in tariffs by the President-elect Trump in the USA and the cancellation of electric vehicle tax credits will affect rhodium demand. On the other hand, further delays in the rebound of rhodium recovery supply could widen the supply-demand gap in 2025, which might push rhodium prices higher.

Current Status and Outlook of the Rhodium Market