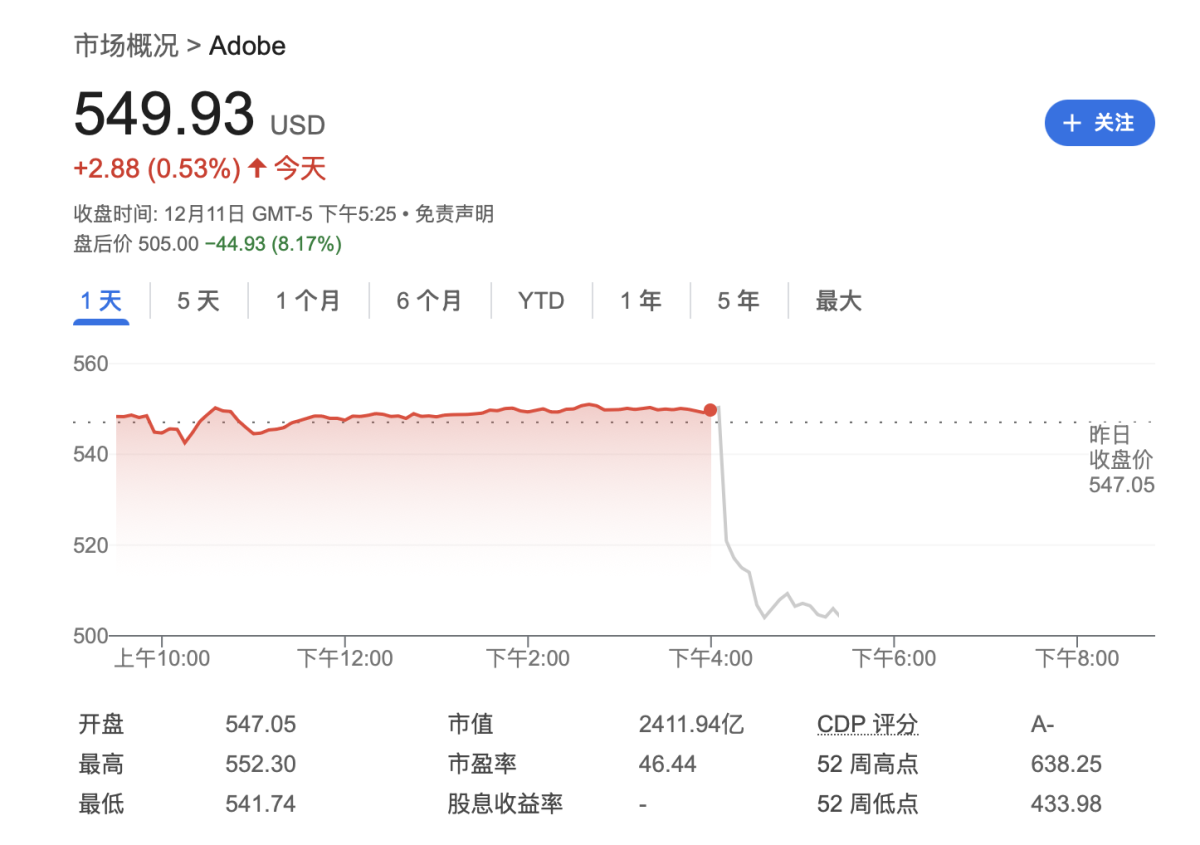

Adobe released its fourth-quarter results on Wednesday after Post-Market Trading, showing that although the company's adjusted EPS exceeded expectations for the fourth quarter, the guidance for fiscal year 2025 fell short of expectations. Adobe's stock dropped over 8% in post-market trading at one point. Analysts believe that Adobe's disappointing performance guidance has intensified market concerns about the company's potential impact from emerging AI startups.

Adobe released its fourth-quarter results on Wednesday after Post-Market Trading, showing that although the company's adjusted EPS exceeded expectations for the fourth quarter, the guidance for fiscal year 2025 fell short of expectations. Adobe's stock dropped over 8% in post-market trading at one point. Analysts believe that Adobe's disappointing performance guidance has intensified market concerns about the company's potential impact from emerging AI startups.

Here are the key points from Adobe's Earnings Reports:

Key financial data:

Key financial data:

Revenue: Adobe achieved revenue of 5.61 billion USD in the fourth quarter of fiscal year 2024, a year-on-year growth of 11%, exceeding analysts' expectations of 5.54 billion USD.

Operating profit: The GAAP operating profit for the fourth quarter was 1.96 billion USD, while the non-GAAP operating profit was 2.6 billion USD.

Net income: The GAAP net income for the fourth quarter was 1.68 billion USD, while the non-GAAP net income was 2.13 billion USD.

EPS: The adjusted diluted EPS was 4.81 USD, higher than analysts' expectations of 4.67 USD.

Business data:

Digital Media Sector: Revenue was 4.15 billion USD, a year-on-year increase of 12%. Document Cloud revenue was 0.843 billion USD, a year-on-year increase of 17%. Creative Cloud revenue increased to 3.3 billion USD, a year-on-year increase of 11%, in line with Analyst expectations.

New Digital Media: Annual Recurring Revenue (ARR) was 0.578 billion USD, with Digital Media ARR reaching 17.33 billion USD at the end of the quarter. Document Cloud ARR increased to 3.48 billion USD. Creative Cloud ARR increased to 13.85 billion USD.

Digital Experience Sector: Revenue was 1.4 billion USD, a year-on-year increase of 10% (calculated at reported and fixed exchange rates). Digital Experience subscription revenue was 1.27 billion USD, a year-on-year increase of 13%.

Full-year data:

Revenue: Adobe achieved revenue of 21.51 billion USD in fiscal year 2024, a year-on-year increase of 11%.

Operating Profit: GAAP operating profit was 6.74 billion USD, and non-GAAP operating profit was 10.02 billion USD.

Net income: GAAP net income was 5.56 billion USD, and non-GAAP net income was 8.28 billion USD.

EPS: GAAP EPS is $12.36, Non-GAAP EPS is $18.42.

Cash Flow: Operating cash flow for the year reached $8.06 billion.

Share Buyback: Approximately 17.5 million stocks were repurchased throughout the year.

2025 Fiscal Year Performance Guidance:

Revenue: Expected revenue for the 2025 fiscal year is $23.4 billion, below the analyst forecast of $23.8 billion.

EPS: The expected EPS is between $20.20 and $20.50, below the analyst forecast of $20.52.

Adobe is known for its software developed for creative professionals, and the company is currently adding generative AI features to its applications, such as embedding its proprietary model Firefly in products like Photoshop. However, some analysts point out that the launch speed of its AI video products is noticeably lagging behind OpenAI's Sora service.

At the annual user conference held in October, Adobe launched an AI tool for creating videos, which has been integrated into the editing application Premiere and is gradually being opened to the public. David Wadhwani, head of Adobe's creative business, stated that the company will soon launch a "new High Stock Price Firefly service," which will include video model capabilities.

The Chairman and CEO of Adobe, Shantanu Narayen, stated:

“Adobe generated record revenue in fiscal year 2024, reflecting strong demand for Creative Cloud, Document Cloud, and Experience Cloud, as well as the critical role these products play in driving the AI economy. Our highly differentiated technology platform, rapid pace of innovation, diversified market strategy, and integration of Cloud Computing Services provide a solid growth outlook for the coming year.”

However, the future of Adobe's AI transformation remains uncertain. Since the beginning of this year, Adobe's Stocks have declined by 7.8%, underperforming the software Industry Index's increase of over 30%. Concerns have repeatedly arisen among investors that AI-based creative tools from companies like OpenAI or Runway AI could capture market share from Adobe. Following the Earnings Reports announcement, Adobe's stock price fell more than 8% in Post-Market Trading on Wednesday.

Last quarter, Adobe stated that its strategy is to encourage customers to use AI features rather than directly profit from these tools. However, this strategy has begun to test investors' patience.

Citigroup Analyst Tyler Radke had previously lowered Adobe's Target Price, believing that due to Adobe's greater focus on expanding its user base rather than monetizing technology, its stock price may continue to fluctuate within a Range.

Hamilton Capital Partners Chief Investment Officer Alonso Munoz believes that Adobe needs to win customers' recognition through practical AI products like Salesforce.

"If Adobe's pricing can translate into growth this quarter and investors like this performance, then the stock price will see returns. If this goal can really be achieved, I think it will catch up with other AI stocks."