根据芝商所FedWatch工具显示,截至周二,交易员已经将美联储12月降息25个基点的概率定为约86%,与缄默期开始前的情况几乎没有变化。

根据芝商所FedWatch工具显示,截至周二,交易员已经将美联储12月降息25个基点的概率定为约86%,与缄默期开始前的情况几乎没有变化。Federal Reserve observers indicate that the November CPI data is likely to present unexpected results, potentially leading to a deviation from the easing policy.

Federal Funds Rate.Futures tradingMembers are about 86% confident that the Federal Reserve will cut interest rates by 25 basis points next week, which is generally consistent with the confidence level before historical policy decisions.

As pointed out by analysts at Industrial Bank in a report last week, when policymakers enter the so-called "quiet period," the market usually has more than 80% certainty regarding the actions of the Federal Reserve.

According to the CME FedWatch Tool, as of Tuesday, traders have set the probability of a 25 basis point cut in December by the Federal Reserve at about 86%, which has seen almost no change since the start of the quiet period.

According to the CME FedWatch Tool, as of Tuesday, traders have set the probability of a 25 basis point cut in December by the Federal Reserve at about 86%, which has seen almost no change since the start of the quiet period.

Expectations of interest rate cuts are a factor in the strong rebound of the stock market.$S&P 500 Index (.SPX.US)$and$Nasdaq Composite Index (.IXIC.US)$Last week, it reached record highs, with the Dow Jones Industrial Average first surpassing the 45,000-point threshold.

So far, everything is going smoothly. But what if things change? After all, there are still some quite important data to be released this week, the most noteworthy being the November CPI Index announced on Wednesday and the PPI Index on Thursday.

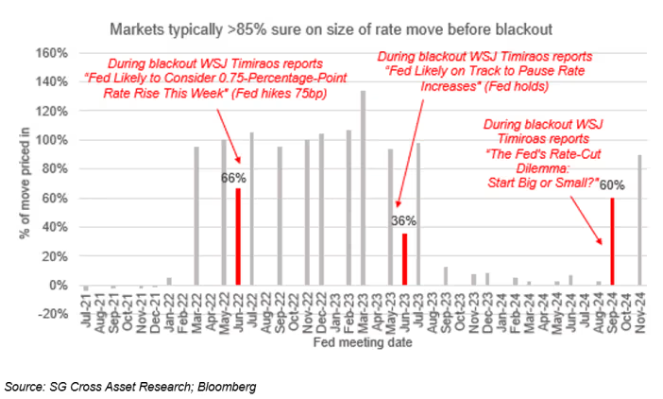

Of course, the Federal Reserve can let market participants infer things for themselves, as they have in the past. Or, as the analyst from Société Générale said, "there are also some exceptions and other means of communication." In the chart below, they listed some recent exceptions, where the Wall Street Journal correctly described the Federal Reserve's subsequent decision during the quiet period.

In September, there were some drastic fluctuations in the federal funds Interest Rates futures, oscillating between a 25 basis point or a 50 basis point rate cut. Subsequently, on September 12th, Nick Timiraos, a reporter from The Wall Street Journal known as the "Fed’s mouthpiece," emphasized in an article the Fed’s "dilemma" in deciding whether to cut rates by 25 or 50 basis points, which investors interpreted as a signal that the extent of the rate cut was still negotiable, leading to heightened expectations for a larger cut. The Fed announced a 50 basis point cut on September 18th.

The highlighted early silence period reports in the chart help clarify market expectations for the Fed's subsequent actions, including the massive 75 basis point hike in June 2022 and the pause in the 2023 rate hike cycle.

As indicated by market probabilities, to prompt the Fed to signal to investors to lower expectations for a rate cut next week, an unexpected event is required, and the threshold for such an event is quite high.

The market expects that the November CPI month-on-month growth rate, scheduled to be published on Wednesday, will rise from 0.2% in October to 0.3%, and the year-on-year growth rate will increase from 2.6% in October to 2.7%, while the core CPI is expected to maintain a year-on-year growth rate of 3.3%.

The minutes from the Fed’s November meeting indicate that strong economic data and inflation data exceeding expectations have led "many" officials to believe that a more gradual approach to rate cuts may be more appropriate. Powell also expressed this view, stating that the Fed does not need to rush to cut rates. This has led investors to lower their expectations for Fed rate cuts in 2025, with Fed watchers suggesting that after a rate cut in December, the Fed might cut rates once every other meeting next year.

Analysts state that the recent remarks by Fed officials, including Powell, have not been viewed as opposing the expectation of a rate cut in December. Fed Governor Waller stated last week that unless economic data surprises, he leans towards a rate cut, further solidifying those expectations.

The employment report for November released last Friday seems to further reinforce market expectations for a rate cut in December, and the November inflation data this week has become the last uncertain factor before the silence period begins.

However, Tom Essaye, founder of Sevens Report Research, noted in the report that despite a mild rebound in recent data, including CPI, most Fed members have been downplaying the inflation risks in the coming weeks.

Essaye and Others indicate that policymakers seem to believe that inflation is moving towards their 2% target, partly because they anticipate that housing inflation has been overestimated.

Jay Hatfield, CEO and portfolio manager of Infrastructure Capital Advisors, stated in a phone interview that if the CPI Index rises by 0.4% month-on-month, it could raise serious doubts about a rate cut next week, and it's hard to see where such strong data could come from.

Hatfield expects the Federal Reserve to implement a "hawkish" rate cut, which means it will reduce the federal funds rate while simultaneously signaling that it will slow the pace of easing. More importantly, the Fed's meeting in December will release the latest dot plot.

These predictions include each member's forecasts for future federal funds rates, which itself is a powerful communication tool. Hatfield mentioned that a dot plot showing limited rate cuts may help "keep the hawks at bay," thereby calming any dissent regarding actions in December.

Editor/Rocky