10日周二,10年期国债活跃券“24附息国债11”(240011)收益率走低7.5BP,

10日周二,10年期国债活跃券“24附息国债11”(240011)收益率走低7.5BP,China Merchants Securities believes that the shift in monetary policy towards “moderate easing” means that interest rate cuts can be expected next year, opening up room for short-term interest rates to decline. Dongwu Securities said that there is a time lag at the inflection point of equity bonds. There will be a period of “stock and debt double bulls” before switching to “stocks, bonds, and bears.” It is expected that next year will arrive, and the yield on 10-year treasury bonds may drop to 1.5%.

The Politburo meeting of the CPC Central Committee held on December 9 continued the positive policy tone of the September Politburo meeting and sent multiple signals that exceeded expectations.

Among them, the conference's “moderately loose” monetary policy was re-stated for the first time in 14 years. Expectations for monetary easing and interest rate cuts suddenly heated up, driving medium- to long-term bond yields to a collective decline.

On Tuesday the 10th, the yield of the 10-year active treasury bond “24 interest-bearing treasury bond 11” (240011) fell by 7.5 BP, hitting an intraday low of 1.8225%, continuing to set a record low. The cumulative decline was 10 BP within two trading days, with a decline of 15 BP within a week.

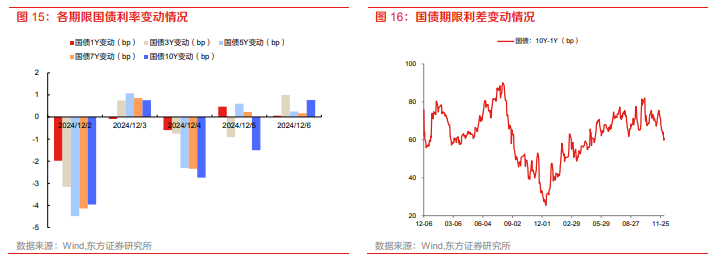

On Tuesday the 10th, the yield of the 10-year active treasury bond “24 interest-bearing treasury bond 11” (240011) fell by 7.5 BP, hitting an intraday low of 1.8225%, continuing to set a record low. The cumulative decline was 10 BP within two trading days, with a decline of 15 BP within a week.

The yield on the 30-year active treasury bond “24 Special Treasury Bond 06” (2400006) also declined, once falling 7 BP to 2.0450%.

In the futures market, treasury bond futures rose strongly throughout the day. The 30-year main contract closed up 1.37%, reaching a record high. 10-year, 5-year, and 2-year treasury bond futures all rose by varying degrees.

The treasury bond ETF market is all flourishing. The 30-year treasury bond ETF rose 1.87%, and the 10-year treasury bond account rose 0.58%.

Can the bond market continue to improve with the support of easy liquidity?

Since last week, the bond market has quickly interpreted the runaway market. Long-term interest rates have broken through the 2% key point downward, and then began a game between the short side and the take-profit side.

The arrival of yesterday's Politburo meeting once again ignited enthusiasm in the bond market, and the confidence of “debt bulls” was strengthened.

According to the analysis of China Merchants Fixed Income Zhang Wei's team, this Politburo meeting sent a signal that the growth policy continues to be strengthened. The shift in monetary policy towards “moderate easing” means that interest rate cuts can be expected next year, opening up room for short-term interest rates to decline, thus driving interest rates on 10-year treasury bonds and 30-year treasury bonds to a sharp decline at the end of today's session.

Judging from historical experience, since 2020 (excluding 2022), the bond market has often fluctuated 5-10 trading days before the December Politburo meeting, and the bond market tends to fluctuate and strengthen after the conference is held.

In terms of capital, China Merchants Securities said that although funding will be seasonally reduced in mid-late December, the impact on long-term bonds is manageable. Short-term interest rates are declining or blocked, and the interest rate curve is expected to flatten.

Investment Strategy Zhang Xia's team believes that in a situation where loose monetary policy is expected to continue in the future, the medium- to long-term interest rate center in the market may further decline, and the cost performance ratio of stock assets compared to bond assets will further improve. If the profit effect of the equity market continues to improve in the future and residents' deposits move to the equity market, in theory, there will be plenty of room for growth in A-shares.

Judging from market performance, from the beginning of December to the Politburo meeting, the Central Economic Conference, and 5 days, 10 days, 20 days, and a month after the Central Economic Work Conference, the probability of the market rising varies from the beginning of December to the Politburo meeting. However, as far as indices are concerned, major large-cap indices, such as the Shanghai and Shenzhen 300 and Shanghai Stock Exchange 50, all have a probability of rising by more than 50%, or about 67%; the probability that the GEM index will rise is about 50%, and the probability that the China Stock Exchange 1000 will rise is about 33%.

This has raised another layer of concern: will the rise in the stock market lead to a “seesaw in equity” effect, spurred by growth policies?

Dongwu Securities believes that taking the “stock bond seesaw” in 2020 as an example, the Shanghai Composite Index bottomed out and rebounded in March 2020, while 10-year treasury bond yields continued to decline during this period, and did not rise from a low point until April.

This phenomenon of unsynchronized switching can be understood using the monetary credit cycle. The inflection point of “stocks, bulls, and bears” usually occurs in the “broad money+easy credit” or “tight money+easy credit” stage, and it is necessary to wait until “easy credit” is verified. Compared to stocks, bonds are more faithful to fundamentals, and need to wait until continuous “easy credit” verification before entering a state where an inflection point has been established.

Dongwu Securities further stated that due to the time lag between stocks and bonds at the inflection point, there will be a period of “stock and debt double bulls” when shifting to “stocks, bonds, and bears.” Under the current loose monetary policy, next year may usher in a “double bullish equity” phase. Based on our judgment on drastic interest rate cuts, the yield on 10-year treasury bonds is expected to drop to 1.5%.