相较于老乡鸡,小菜园不管是业绩还是知名度都更为“低调”,此时上市,或要面临“市场冷淡”的挑战,小菜园有何优势?其基本面表现如何?

相较于老乡鸡,小菜园不管是业绩还是知名度都更为“低调”,此时上市,或要面临“市场冷淡”的挑战,小菜园有何优势?其基本面表现如何?After the acceleration of expansion, what was left for small vegetable gardens was “a great deal of sadness”

After Hometown Chicken Break, Xiao Caiyuan, a Chinese restaurant brand also from Anhui, knocked on the Hong Kong stock capital market.

According to the Hong Kong Stock Exchange's disclosure on December 4, Xiaocaiyuan International Holdings Limited (abbreviation: Little Caiyuan) passed the Hong Kong Stock Exchange hearing, and Huatai International and UBS Group were co-sponsors.

Compared to hometown chicken, Little Vegetable Garden is more “low-key” in terms of performance and popularity. If you go public at this time, you may face the challenge of a “lukewarm market”. What are the advantages of small vegetable gardens? How is its fundamental performance?

Compared to hometown chicken, Little Vegetable Garden is more “low-key” in terms of performance and popularity. If you go public at this time, you may face the challenge of a “lukewarm market”. What are the advantages of small vegetable gardens? How is its fundamental performance?

Annual revenue exceeds 4.5 billion yuan, and performance is growing rapidly

According to the prospectus, Little Vegetable Garden is one of the well-known chain restaurants directly managed by the Chinese public convenience Chinese restaurant market, and ranks among the top in the industry in terms of business scale and growth rate. Small vegetable garden dishes are mainly famous for Hui dishes such as farmhouse braised meat, crock pot chicken, and smelly mandarin fish. As of the last practical date, the company had 623 direct stores in operation, covering 135 cities or counties in 13 provinces in China. Currently, the company's main store operations are located in East China, and the company has also expanded its store network to other regions of China.

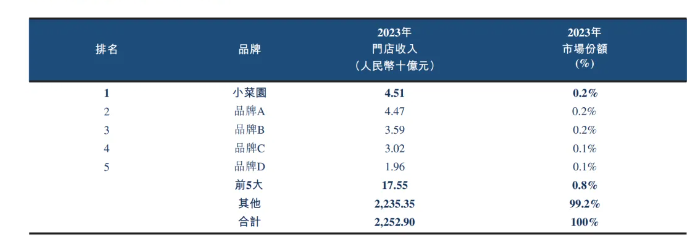

According to Frost & Sullivan's data, in terms of store revenue in 2023, “Little Vegetable Garden” ranked first among all brands in China's popular convenient Chinese restaurant market. The customer unit price ranged from 50 yuan to 100 yuan, accounting for 0.2% of the market share. In terms of revenue, the size of the popular convenient Chinese restaurant market with a customer unit price of between RMB 50 and RMB 100 was RMB 2252.9 billion in 2023, accounting for about 55.2% of the overall Chinese restaurant market.

Looking at it now, the small vegetable garden's performance is on a rapid growth channel. For the four months ended April 30 from 2021 to 2024 (hereinafter referred to as the reporting period), small vegetable gardens achieved revenue of about 2.646 billion yuan (unit: RMB, same below), 3.213 billion yuan, 4.549 billion yuan, and 1.68 billion yuan, respectively. In the same period, annual/period profits were approximately 0.227 billion yuan, 0.238 billion yuan, 0.532 billion yuan, and 0.194 billion yuan, respectively.

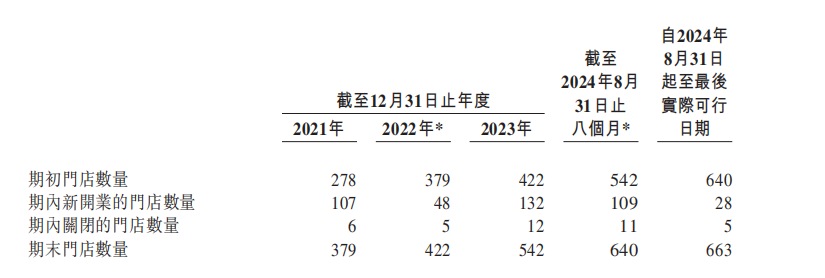

During the track record period, the company's revenue mainly came from “Little Vegetable Garden” brand stores, which accounted for 98.7%, 98.8%, 99.1% and 98.9% of the company's total revenue. Therefore, the reason for the increase in revenue from small vegetable gardens is mainly due to the expansion of the number of stores. During the period, the number of new stores added to Little Vegetable Garden was 107, 48, 132 and 28, respectively.

It is worth noting that as the number of newly opened stores increased, there was a decline in the single-store operation of Little Vegetable Garden. In the eight months ended August 31, 2024, same-store sales of “Little Vegetable Garden” stores decreased by 11.4% compared to the same period in 2023; the operating margin at the store level fell from 21.3% to 17.8%.

According to the prospectus, the turnover rate and per capita consumption of Xiaocaiyuan stores in all tier cities are declining. Among them, the new first-tier cities have shrunk the most. The turnover rate in 2023 was 3.1 times, down 0.4 times from the previous year, and the number of dine-in customers dropped by 18.9%.

It can be seen that after the acceleration of expansion, there is still “a lot of sorrow” left for small vegetable gardens. To make matters worse, in the face of declining same-store performance, Little Vegetable Garden chose to continue running wild in the face of a blindfold.

Blindfolded to achieve the Thousand Stores Plan in 2026?

According to the prospectus, Little Vegetable Garden's next plan is to open 160, 190 and 230 new stores in 2024-2026, respectively, in order to achieve the goal of 1,000 stores by the end of 2026.

In fact, the practice of “sacrificing short-term profits in exchange for long-term shares” is not uncommon in the restaurant industry. For example, undersea fishing in the past. Hui cuisine, which is the main focus of the small vegetable garden, is far less popular and chain-based than that of cuisines such as Sichuan cuisine, Hunan cuisine, and Cantonese cuisine, and there are no competitors of the same level on the market. Now is a good time for them to hurry up and gain ground.

Simply put, what small vegetable gardens are looking for at this stage is to increase market share and establish a brand image in the corresponding segmented circuit to prevent the emergence of another strong competitor. It's like the story of Green Tea and Grandma's House, Kicha and Nayuki.

Furthermore, out of 640 small vegetable garden stores as of August 31 this year, 280 were distributed in third-tier cities and below. In first-tier cities, which have always been a contentious place in the restaurant industry, Xiaocaiyuan stores have only opened 97 stores. Among these, apart from the relatively large number of stores in Shanghai, which are located in East China, there are only about 20 stores in Beijing, while the number of stores in Shenzhen and Guangzhou is all in single digits. It can be seen that the small vegetable garden follows the “rural area surrounds the city” path.

However, it is always difficult for catering companies, especially Chinese food, to bypass first-tier cities. First-tier cities have customers with the strongest spending power, a more inclusive and open consumer atmosphere, and are closer to capital. If small vegetable gardens want to incubate more new business formats or sub-brands and increase brand influence in the future, they must also take root in first-tier cities. Although the share of small vegetable gardens in first-tier cities climbed to 17.6%, the number of stores in third-tier and third-tier cities (including county-level cities and counties) accounted for 41.4%, which is still an important cornerstone of the brand.

Of course, entering a first-tier city is also risky. In addition to higher rent and labor costs, there is also tougher competition. As mentioned earlier, the sharp increase in marketing expenses for small vegetable gardens is a sign worth watching.

Furthermore, since this year, the average daily sales volume and same-store turnover rate of small vegetable gardens in first-tier cities have all declined. The average daily sales of single stores in first-tier cities fell from 32,296.5 yuan in the first 8 months of 2023 to 28,325.7 yuan; during the same period, the turnover rate of same-store stores in first-tier cities dropped from 3.4 to 3.0. It can be seen that the company's profitability in first-tier cities is unstable.

Stores are unquestionably fundamental to the survival of catering companies. Let alone small vegetable gardens that are about to go public, urgently need to “prove” their growth to the market and investors.

However, catering companies are inherently an industry that is difficult to standardize. Even if the trend of industry chains and branding is strengthened, rapid expansion within a short period of time is still a huge test of the company's organizational management ability. Encouraging growth is not a good thing; efficient expansion may be the long-term solution.

If Little Vegetable Garden officially launches its ambitious store opening plan, whether its management, supply chain, service quality, quality control, etc. can keep up with its rapid development in the short term is a hidden concern behind its expansion.

Furthermore, the Zhitong Finance App noticed that Little Vegetable Garden also paid large amounts of dividends when it needed a large amount of capital to expand its business. In 2021, the company declared a dividend of 0.15 billion yuan; in 2023, it declared a dividend of about 0.135 billion yuan. For the four months ended April 30, 2024, the company declared a dividend of approximately $0.188 billion, accounting for about 96% of the current net profit.

The above dividends mainly go into the “pockets” of the actual controllers of the company. According to the prospectus, as of the last practical date, Wang Shugao controlled about 92.99% of Xiaocaiyuan's issued share capital through seven shareholding platforms including XCY Yongqing Limited.

What is intriguing is that in the face of rapid growth in performance, the debt scale of small vegetable gardens remains high. According to the prospectus, as of August 31, 2024, Xiaocaiyuan's total current liabilities were 0.654 billion yuan, total non-current liabilities were 1.239 billion yuan, and net assets were 0.813 billion yuan.

In this context, Xiaocaiyuan's large dividend before the IPO may raise market concerns about its financial health. The company's listing and fund-raising “supplements the blood” provides momentum for business expansion, but in the fiercely competitive environment of the restaurant market, whether the growth story of its rapid expansion can be realized with high quality also needs to be seen and seen.