当前市场主流观点认为,“谷子”之所以能爆火出圈,背后底层逻辑在于供给侧愈发丰富的优秀IP与需求端新生代消费者日益增长的悦己消费需求相适应,IP供给与精神消费共振下行业的景气度持续提升。

当前市场主流观点认为,“谷子”之所以能爆火出圈,背后底层逻辑在于供给侧愈发丰富的优秀IP与需求端新生代消费者日益增长的悦己消费需求相适应,IP供给与精神消费共振下行业的景气度持续提升。The "Guzi Economy" is booming; can Bluku capitalize on this trend to fulfill its capital dream?

Since late September, China's Capital Markets have significantly rebounded. With the market participants' risk appetite greatly increasing, equity Assets are highly liquid, and various Concepts continue to emerge. Among them, the newly surfaced "Guzi Economy" has particularly caught the attention of investors.

Guzi is a transliteration of the English word "goods," referring broadly to second-dimensional peripheral products derived from copyright works such as animation, comics, games, and novels. From the perspective of the Industry Chain, the "Guzi Economy" involves multiple links including IP development and design, Operation and communication, product manufacturing, and market sales.

Current mainstream opinion in the market suggests that the reason "Guzi" can gain immense popularity is that its underlying logic aligns with the increasingly rich supply of excellent IP on the supply side and the growing self-satisfaction consumption demands of the new generation of consumers on the demand side. The resonance between IP supply and spiritual consumption continues to enhance the prosperity of the Industry.

Current mainstream opinion in the market suggests that the reason "Guzi" can gain immense popularity is that its underlying logic aligns with the increasingly rich supply of excellent IP on the supply side and the growing self-satisfaction consumption demands of the new generation of consumers on the demand side. The resonance between IP supply and spiritual consumption continues to enhance the prosperity of the Industry.

According to Zhitong Finance APP, the "Guzi Economy" is gaining momentum, which may inadvertently provide a favorable opportunity for companies related to licensed derivatives.

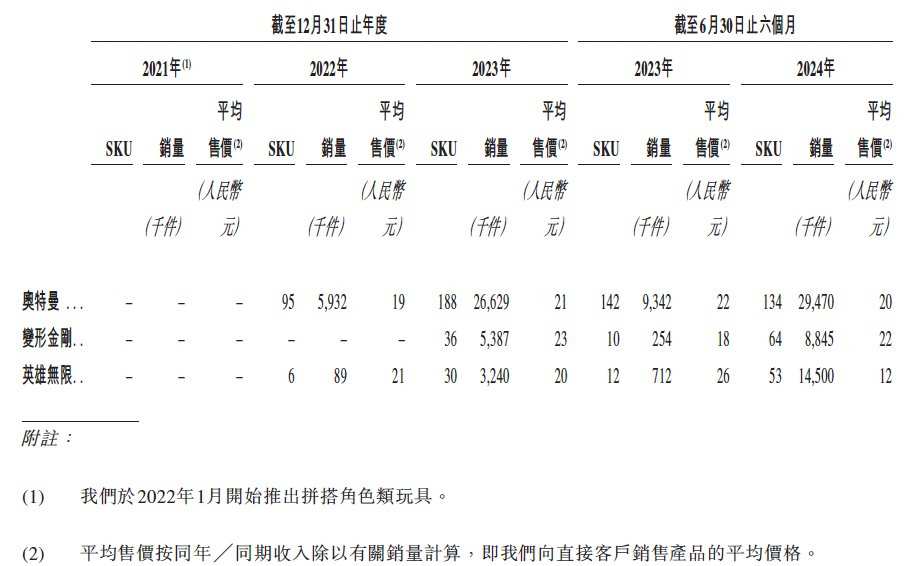

Take Bluku Group Limited (hereinafter referred to as "Bluku"), which recently resubmitted its application to the Hong Kong Stock Exchange. As a leader in the domestic building block toy market, Bluku has achieved rapid growth through over 500 patent layouts, original IP capabilities, and partnerships with about 50 well-known IPs, including Ultraman. Among these, the role of Ultraman IP is crucial, as over half of Bluku's current income comes from the sales of Ultraman IP products.

However, despite riding the wave, Bluku's fundamentals are not without concerns. For example, during the period from 2021 to the first half of 2024, the company has consistently struggled to effectively resolve the longstanding issue of profitability. Additionally, as of now, the performance contribution of Bluku's own IP is far less than that of externally licensed IPs like Ultraman and Transformers, which may increase external concerns about the sustainability of the company's growth.

With the support of Ultraman IP, "Briyno's Second Attempt" at the Hong Kong Stock Exchange.

Briyno's history can be traced back to 2014, and after ten years of development, the company has grown to become a leader in the Consumer building block toy segment in China. According to Frost & Sullivan, Briyno's GMV in 2023 was approximately 1.8 billion yuan (RMB, the same below), with a year-on-year increase of as much as 170%. By GMV, Briyno holds about 7.4% of the Consumer building block toy market in China.

Currently, most of Briyno's revenue comes from products based on the three IPs: Ultraman, Transformers, and Heroes Unlimited. Among these, Heroes Unlimited is one of the two proprietary IPs launched by Briyno.

It is worth mentioning that prior to submitting the listing application to the Main Board of the Hong Kong Stock Exchange, Briyno had also submitted an application in May of this year, but at that time the company ultimately failed to pass.

In terms of financial performance, Briyno's results have structural highlights, but there are also several concerns. From 2021 to the first half of 2024, Briyno's revenues were 0.33 billion yuan, 0.326 billion yuan, 0.877 billion yuan, and 1.046 billion yuan, showing significant growth in company size.

Driven by revenue, Briyno's gross margin has seen substantial growth, increasing from 0.123 billion yuan in 2021 to 0.415 billion yuan in 2023, and soaring to 0.554 billion yuan in the first half of this year, with corresponding gross margins of 37.4%, 37.9%, 47.3%, and 52.9%.

Further analysis shows that Ultraman IP has played a crucial role in Briyno's rapid scaling. In the years of significant increases in revenue and gross margin in 2023 and the first half of this year, product sales revenue from Ultraman IP accounted for 63.5% and 57.4% of the company's total revenue, respectively. In other words, of Briyno's total revenue of over 1 billion yuan in the first half of this year, Ultraman IP alone contributed 0.6 billion yuan.

Although the Ultraman IP has boosted Bluco's scale, this is still not enough to help the company solve its longstanding profitability issues. During the reporting period, Bluco's net income was -0.507 billion yuan, -0.423 billion yuan, -0.207 billion yuan, and -0.255 billion yuan respectively. Judging from the trend, it seems there is still a considerable distance for the company to truly turn a profit.

The 'Millet Economy' is booming, will Bluco take advantage of it?

The fundamentals are a mixed bag, but as the enthusiasm for the 'Millet Economy' continues to rise in the secondary market, Bluco, holding a well-known IP, may be more eager than ever to quickly enter the Capital Markets and get a share.

If we set aside the thematic investments in the secondary market for a moment, from an industry perspective, Bluco indeed has considerable appeal. Data shows that as a fast-growing segment of the toy market, from 2019 to 2023, China’s building block toys have an average annual compound growth rate (CAGR) of 12.7%, far outpacing non-building block toys; additionally, it is forecasted that the CAGR for domestic building block toys from 2023 to 2028 will be 22.1%, with growth expected to further increase, potentially expanding this market size to 64 billion yuan by 2028.

The industry has great potential, and in recent years, the rising popularity of secondary-dimensional Consumer trends may further ignite the building block toy market. According to iResearch data, it is estimated that the market size of the secondary-dimensional market will grow from 18.9 billion yuan in 2016 to 221.9 billion yuan in 2023, with a compound growth rate of 42.17% from 2016 to 2023. Among these, the derivative market for secondary-dimensional peripherals will grow from 5.3 billion yuan in 2016 to 102.4 billion yuan in 2023, achieving a remarkable compound growth rate of 52.66% from 2016 to 2023.

In the face of a promising market for IP derivative consumption represented by the 'Millet Economy', since Bluco already has a first-mover advantage, it becomes particularly important to further consolidate its competitive edge based on its existing foundation.

The prospectus shows that Blokko is planning to continue expanding its product portfolio to cover a wider range of demographics and price ranges, including launching more SKUs based on well-known IPs such as Minions, Pokémon, and Detective Conan. The company plans to launch approximately 800 SKUs by 2025, a number that is double compared to this year; meanwhile, the company will also continue to expand its cooperation with well-known IP copyright holders. As of December 6, Blokko is in negotiations for IP licensing arrangements with over 25 well-known IPs.

However, it should be noted that with the booming 'Millet Economy', competition for well-known IPs among related companies may become even more intense. Additionally, considering that Blokko's licensing agreements typically last for 1-3 years and do not automatically renew upon expiration, this also means that if the industry becomes more crowded, it may impact a company like Blokko's ability to obtain licenses under favorable terms from IP copyright holders or licensors. In other words, if there is no positive change in the future reliance on a few licensed Intellectual Properties (IPs), the certainty and sustainability of Blokko's growth may still be in question.

In summary, leveraging external 'favorable winds', Blokko's performance imagination has improved significantly compared to the past. If it successfully goes public, the company's appeal to capital is also worth looking forward to. However, amid the noise, it must be acknowledged that Blokko's real 'value' also has significant room for improvement. If the company cannot resolve its continuous losses and high dependency on a few licensed Intellectual Properties (IPs), Blokko's long-term investment value may still be difficult for the market to recognize.