同时,该行将目标价从7.50美元上调至14.20美元,这一价格对应2025年和2026年预测市盈率分别为32倍和10倍,以及2025年预测PEG(市盈率相对盈利增长比率)为0.3倍,预计2025-2027年净利润复合年增长率达到114%。基于以上分析,花旗维持对禾赛的“买入”评级。

同时,该行将目标价从7.50美元上调至14.20美元,这一价格对应2025年和2026年预测市盈率分别为32倍和10倍,以及2025年预测PEG(市盈率相对盈利增长比率)为0.3倍,预计2025-2027年净利润复合年增长率达到114%。基于以上分析,花旗维持对禾赛的“买入”评级。Citigroup's research report firmly maintains a "buy" rating for Hesai and significantly raises the target price to $14.2.

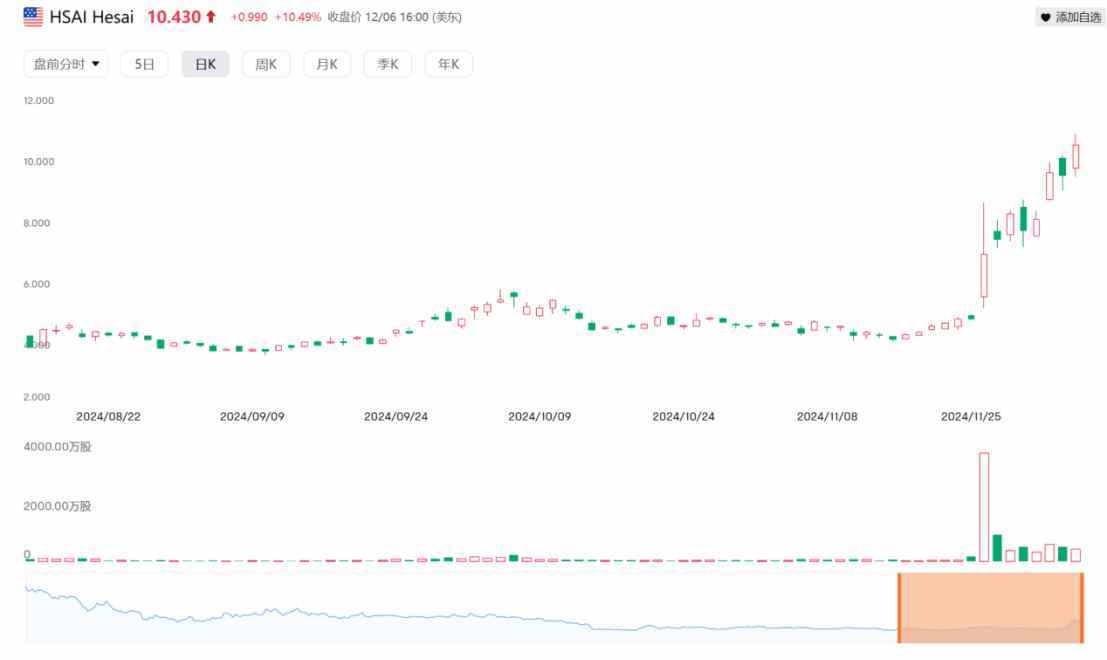

According to a report from a leading usa brokerage, Citigroup, it firmly maintains a "buy" rating for Hesai (HSAI.US) and significantly raises the target price to $14.2, which still has nearly a 40% upside compared to the closing price on December 6. Citigroup believes that considering the contributions to Hesai's lidar sales from companies like BYD, Xiaomi Autos, Chongqing Changan Automobile, and Leapmotor, the firm's cumulative shipment forecast for Hesai in 2025 has been raised from 1.17 million autos to 1.51 million autos, and the 2026 cumulative shipment forecast has been raised from 2.11 million autos to 3.56 million autos.

Given that the sales of rbob gasoline vehicles exceeded expectations in the fourth quarter of 2024, Citigroup expects a significant rebound in the penetration rate of new energy vehicles in china in the first quarter of 2025, which is likely to greatly improve investor sentiment towards the new energy fund industry. Therefore, Citigroup maintains a p/s ratio of 1.8 and shifts it to 2026.

At the same time, the firm has raised the target price from $7.50 to $14.20, which corresponds to forecast pe ratios of 32 times and 10 times for 2025 and 2026, respectively, as well as a forecast PEG (price-to-earnings growth ratio) of 0.3 times for 2025, with an expected compound annual growth rate of net income from 2025 to 2027 reaching 114%. Based on the above analysis, Citigroup maintains a "buy" rating for Hesai.

At the same time, the firm has raised the target price from $7.50 to $14.20, which corresponds to forecast pe ratios of 32 times and 10 times for 2025 and 2026, respectively, as well as a forecast PEG (price-to-earnings growth ratio) of 0.3 times for 2025, with an expected compound annual growth rate of net income from 2025 to 2027 reaching 114%. Based on the above analysis, Citigroup maintains a "buy" rating for Hesai.

It is worth mentioning that in the third quarter of 2024, Hesai Technology achieved revenue of 0.54 billion yuan, a significant year-on-year growth. The company's lidar product delivery performance was strong, with a total of 134,208 units delivered, a substantial year-on-year increase of 182.9%. Among them, the delivery of advanced driver-assistance systems (ADAS) products was particularly noteworthy, reaching 129,913 units, a year-on-year increase of 220.0%.

In terms of market expansion, Hesai has reached mass production cooperation agreements with 75 models from 20 domestic and international auto manufacturers, including key progress in global mass production vehicle projects with top international brands and securing projects with leading car companies in the japan market, with further deepening cooperation with domestic manufacturers like Leapmotor.

Looking ahead, Hesai Technology has very broad development prospects and is expected to achieve an important milestone in the onboard lidar industry in the fourth quarter: quarterly revenue exceeding $0.1 billion and achieving a profit of $20 million (according to GAAP standards), as well as annual profitability (according to Non-GAAP standards).

Recently, Hesai Technology's impressive third-quarter financial report has led to a significant leap in its stock price, with an increase of about 80% on the day the quarterly report was released.