12月6日,汇丰全球大宗策略师Kim Fustier、Sadnan Ali等发布研报称,OPEC+这一决定近期能给基本面起到支撑作用,预计将使月度超产量从之前的21万桶减少至不足14万桶。

12月6日,汇丰全球大宗策略师Kim Fustier、Sadnan Ali等发布研报称,OPEC+这一决定近期能给基本面起到支撑作用,预计将使月度超产量从之前的21万桶减少至不足14万桶。HSBC believes that if OPEC+ cancels the "extra voluntary" production cut plan as scheduled in March 2026, it will cause the overproduction of crude oil products to expand to 1.2 million barrels per day, further putting downward pressure on oil prices. This means that the situation where global crude oil market supply exceeds demand will continue until 2026, at which time OPEC+ may also have no "room" to cancel the production cut plan.

In light of weak demand and increased crude oil production in non-OPEC+ countries, OPEC+ issued a statement on December 5 local time, announcing the decision to extend the voluntary production cut of 2.2 million barrels per day originally set to expire at the end of December this year for an additional three months until the end of March next year, and to delay the full lifting of production cuts by one year until the end of 2026.

In addition, the UAE also adjusted its plan to restore production increases of 300,000 barrels per day to align with OPEC+, now set from April 2025 to September 2026, instead of the previously scheduled January to September 2025.

On December 6, HSBC global commodity strategists Kim Fustier and Sadnan Ali released research reports stating that OPEC+'s decision is likely to provide support for the fundamentals in the near term, expecting the monthly oversupply to decrease from the previous 0.21 million barrels to less than 0.14 million barrels.

On December 6, HSBC global commodity strategists Kim Fustier and Sadnan Ali released research reports stating that OPEC+'s decision is likely to provide support for the fundamentals in the near term, expecting the monthly oversupply to decrease from the previous 0.21 million barrels to less than 0.14 million barrels.

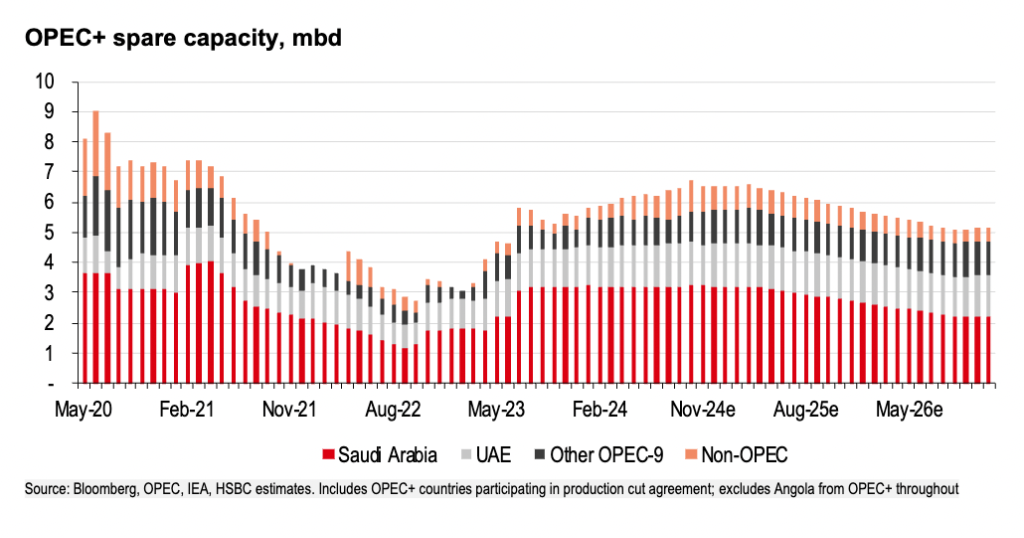

HSBC believes that the extension of the production cut plan by OPEC+ is merely a 'smoke-and-mirrors' tactic that does not address the underlying issue of overall oversupply. Considering that there are still two sets of production cuts yet to be lifted (not until at least the end of 2026), the report estimates that by the end of 2026, OPEC+ will still have around 5.2 million barrels per day of spare buffer capacity, which remains above the long-term average level.

The report predicts that the growth rate of crude oil production in non-OPEC countries from 2025 to 2026 will continue to exceed the demand growth rate, with oversupply expected to exceed 1.2 million barrels per day in 2026, which may render a return to full lifting of the production cuts 'a distant prospect' and further exert downward pressure on oil prices.

If OPEC+ increases production as scheduled, supply may return to an oversupply situation.

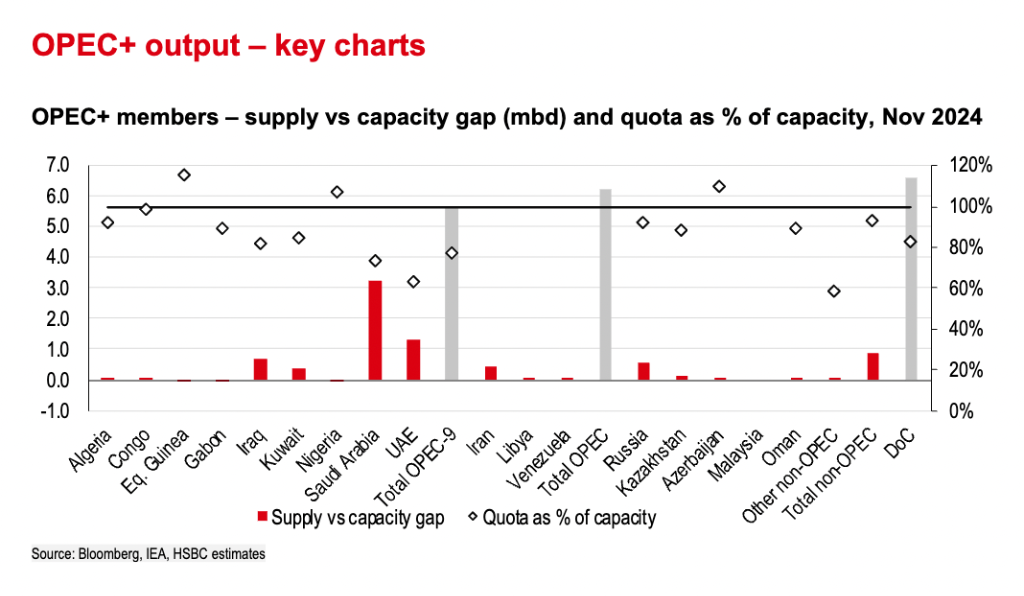

Currently, there are three sets of production cut measures being implemented by OPEC+, including the 'official' cut of 2 million barrels per day, the 'voluntary' cut of 1.66 million barrels per day, and the 'additional voluntary' cut of 2.2 million barrels per day. Prior to the meeting on December 5, OPEC+ had confirmed the extension of the first two sets of production cuts until the end of 2026.

Despite OPEC+ once again extending the third set of production cut plans, the report predicts that the global crude oil market will continue in a state of over-supply until 2026, which means that OPEC+ may not have the "room" to cancel production cut plans at that time.

In 2024, an excess production of 0.3 million barrels per day is expected;

In 2025, an excess production of 0.2 million barrels per day is expected, which is a narrowing compared to the previous expectation of 0.5 million barrels per day;

In 2026, a basic supply-demand balance is expected, but if OPEC+ cancels the production cuts of 2.2 million barrels per day as scheduled, the excess production will grow to 1.2 million barrels per day.

The report also states that although the issue of non-OPEC oil production growing too quickly has not been fundamentally resolved, OPEC+'s choice to gradually lift the production cuts can be seen as the "least bad" option for now; it is expected that Brent crude oil prices will remain at $70 per barrel and above in 2025 and beyond.

HSBC believes that for OPEC+, a possible hope lies in the fact that the new USA government might strengthen control over Iranian oil exports, which would provide space for OPEC+ to resume production increases.

Editor/Jeffy