目前,铠侠的股权结构由贝恩资本牵头的投资者集团和东芝公司共同构成,前者持有约56%的股份,后者则持有约41%的股份。

目前,铠侠的股权结构由贝恩资本牵头的投资者集团和东芝公司共同构成,前者持有约56%的股份,后者则持有约41%的股份。The IPO of Kairui to the major shareholder Bain Capital is a tricky job.

Intelligence Finance learned that, according to informed sources, the preliminary price range set by Japan's storage chip manufacturer Kairui (Kioxia) for its initial public offering (IPO) is 1390-1520 yen. Based on calculations, Kairui will raise a total of 70 billion yen through the IPO. This poses a tricky job for the major shareholder Bain Capital, as the current low return rates of the listed company and Kairui's massive debt may deter potential new investors.

In 2018, a consortium including Bain Capital, Apple (AAPL.US), and South Korea's SK Hynix acquired this previously precious asset from the scandal-ridden Toshiba at a price of 2 trillion yen (about 18 billion USD at the time). This leveraged buyout was hailed as a milestone in the history of Japanese corporate development, especially due to its scale, complexity, involving parties, and Japan's strong opposition to foreign control of strategic technology. Nevertheless, Bain Capital ultimately succeeded.

Currently, Kairui's equity structure is jointly formed by the investor group led by Bain Capital and Toshiba Corporation, with the former holding approximately 56% of the shares and the latter holding about 41%. It is noteworthy that once Kairui successfully goes public, Bain Capital and Toshiba have expressed their intention to gradually reduce their shareholding percentages.

Currently, Kairui's equity structure is jointly formed by the investor group led by Bain Capital and Toshiba Corporation, with the former holding approximately 56% of the shares and the latter holding about 41%. It is noteworthy that once Kairui successfully goes public, Bain Capital and Toshiba have expressed their intention to gradually reduce their shareholding percentages.

The shares that Toshiba and Bain Capital plan to sell in the IPO will incur losses, excluding any dividends and expenses paid. Perhaps this will help drive the listing process. Regardless, completing this transaction is crucial to safeguarding Bain Capital's reputation in the world's hottest private equity markets.

As part of the IPO, Kairui plans to issue 21.6 million new shares, which will raise 31.4 billion yen at the midpoint of the offering price. Toshiba and Bain Capital's BCPE Pangea Fund will also sell a total of 50.4 million shares worth 73.3 billion yen at the same price. The company's stocks are expected to debut on December 18th.

Finding an exit from holding stocks is a tough task. Known for the cyclical collapse of the semiconductor market, Kairui had to shelve its IPO plans in 2020; last year, the merger with Western Digital (WDC.US) was rejected due to SK Hynix's opposition. According to sources, Bain Capital restarted the IPO process several months ago, but it was put on hold due to valuation differences with global investors.

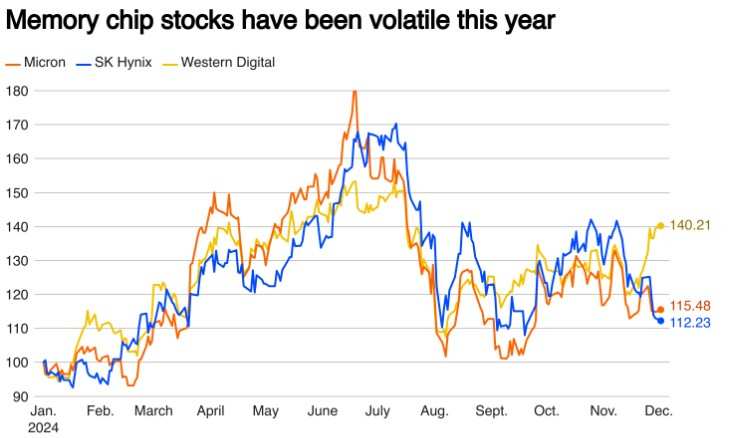

Now, the listing plan has been restarted. The issue is that, based on the midpoint calculation of the initial public offering (IPO) price, the market cap of Kaituo supported by Bain Capital will reach approximately 784 billion yen (about $5.23 billion), obviously much lower than the acquisition price six years ago, and even 20% lower than Toshiba's sale proceeds at that time. Reportedly, this is only half of Bain Capital's planned 1.5 trillion yen valuation when pushing for the listing in October, and according to LSEG's data, as of June, Kaituo's book value of the stock price is only 1.5 times, lower than SK Hynix, Western Digital, and Micron Technology (MU.US). However, the discount is necessary. In June, Kaituo's net debt was 1.2 trillion yen, 14 times the adjusted EBITDA as of the end of the fiscal year 2024.

Indeed, with the rise in storage chip prices, the company's outlook is improving. However, debt repayment will be a burden, especially when competitors are investing huge amounts in new technologies and factories. Analyst Nicolas Baratte, who published an article on SmartKarma, pointed out that over the past three and a half years, Kaituo has reinvested only 27% of its revenue in capital expenditures, lower than the main competitors' 37%.