The sector has investment value and there are also stage-specific trade opportunities.

This article is from the Gelonghui column: China International Capital Corporation Research, authored by Chen Yan and Xu Yunyan

Looking ahead to 2025, we believe that coal is expected to maintain supply and demand balance. Although the central coal price may slightly decline year-on-year, it still remains at a historically relatively high level, supporting the industry's fundamentals. It is expected that the overall industry ROE will remain above 10% in a low-leverage situation (around 30% debt-to-capital ratio), making the sector an attractive investment with periodic trading opportunities.

Summary

Summary

Coal demand growth exceeds expectations. Looking ahead to 2025, we forecast steady growth in coal demand, up by +2.3% year-on-year. The reason is that, structurally, we believe the transformation from old to new energy will not happen overnight, and in the short term coal will continue to play a role in energy security. In terms of total quantity, the market expects energy demand to be significantly affected by the slowdown in traditional high-energy-consuming industries like steel and cement. However, we believe the energy demand elasticity coefficient may remain relatively high in the short term due to the rapid development of new high-quality production forces such as new energy, which also have considerable demand for energy. Additionally, the increasing electrification level of end-use energy is also promoting demand. Therefore, coal demand is expected to maintain strong growth momentum.

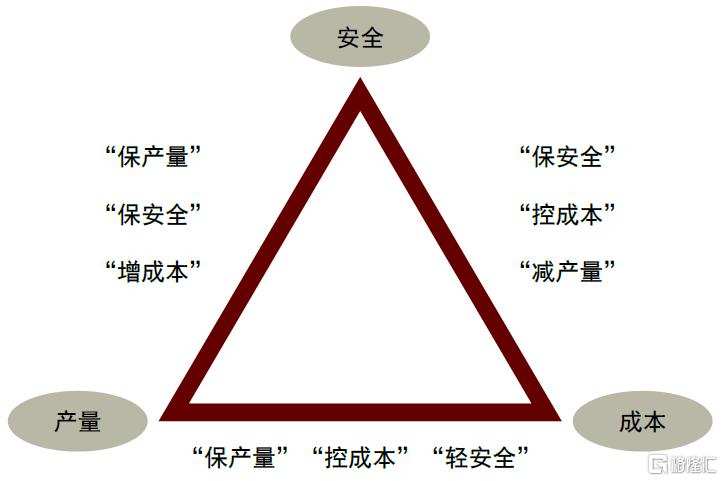

Limited potential for substantial increase in coal supply. Looking ahead to 2025, we forecast a slight increase in raw coal production, up by +1.2% year-on-year, with limited elasticity. This is because coal itself faces an 'impossible triangle,' with production, cost, and safety mutually restrictive. In the short term, we believe the three factors may maintain a weak balance, but in the long run, it may be difficult for all three to coexist. Therefore, under the background of stricter safety supervision and constrained coal prices, maintaining high production levels will face certain challenges. In addition, past underinvestment has led to a decrease in supply elasticity, and looking ahead capacity expansion is constrained by cost increases, carbon reduction policies, etc., hence the likelihood of disorderly growth in industry supply in the medium to long term is low.

Structural changes in credit bode well for the coal supply and demand fundamentals. In the financial cycle's 'second half,' the real estate credit's reduced ability to absorb funds leads to increased incremental capital flowing into various industries, directly and indirectly supporting the coal supply and demand fundamentals. Firstly, countercyclical stimuli benefit coal demand; secondly, the expansion of new high-quality production forces also supports coal demand; thirdly, the coal industry's entry barriers are increasing, and the investment transformation into supply has a long cycle, therefore the stimulating effect of credit changes on industry supply is relatively small.

Risk

Coal demand recovery is lower than expected; Coal supply exceeds expectations; International oil and gas prices fell more than expected.

The coal sector is "both offensive and defensive." Looking ahead to 2025, we believe that with increasingly clear policy signals and improving economic fundamentals, there is hope for coal demand to improve slightly, and coal is expected to maintain a supply-demand balance. Although the central coal price may slightly decrease year-on-year, overall it is still expected to remain at a historically relatively high level, supporting the profitability of the coal industry, with sector fundamentals stronger than many other industries.

However, considering the strong performance of the coal sector in the market since 2021, if expectations for economic recovery strengthen, market attention may shift towards high-elasticity offensive allocations. But if the policy intensity falls short of expectations, the market may focus again on coal targets that are relatively stable in terms of profitability and dividends.

Overall, we believe that the cyclical coal sector will continue to have strong investment value after next year, while also presenting periodic trading opportunities. The core reason is the good supply-demand pattern in the industry, with demand resilience and tight supply being maintained.

► Coal demand growth better than expected. From a structural perspective, we believe the structural transition between new and old energy sources is not immediate. In the short term, coal will continue to play a role in ensuring energy security. Market expectations are that energy demand may be significantly affected by the slowdown in traditional high-energy-consuming industries such as steel and cement, but with the rapid development of new energy and other new quality productivity, the demand for energy is not low. At the same time, the increasing electrification level of end-use energy is also promoting demand. Therefore, coal demand is expected to maintain strong growth momentum.

► The possibility of a significant increase in coal supply is limited. One reason is the "impossible triangle" inherent in coal production, cost, and safety mutually constraining each other. In the short term, we believe the three factors may maintain a weak balance, but in the long term, it is difficult for all three to be balanced. Therefore, under the background of stricter safety supervision and constrained coal prices, sustaining high production levels will be challenging.

In addition, past underinvestment has led to decreased supply elasticity. Looking ahead, capacity expansion faces constraints such as increased costs and decarbonization policies. Hence, the possibility of disorderly long-term supply growth in the industry is low.

► Changes in credit structure are favorable for the coal supply-demand fundamentals. In the "second half" of the financial cycle, the real estate credit's ability to absorb funds is shrinking, with incremental funds flowing into various industries, directly and indirectly supporting the coal supply-demand fundamentals:

1) Countercyclical stimulus is bullish for coal demand. Under the countercyclical policy stimulus, the increase in funds absorbed by sectors such as infrastructure is expected to alleviate the weak demand situation in traditional high-energy-consuming industries to a certain extent.

2) Expansion of new quality production capacity is bullish for coal demand. Under the industrial transformation and upgrading, incremental funds flowing into the manufacturing sectors with good demand prospects are driving the rapid expansion of related industry capacity, leading to an increase in energy demand.

3) Coal has a high entry threshold and the risk of supply exceeding expectations is relatively low. With the overall decline in social investment returns, profit-driven capital is flowing towards industries that still offer returns, leading to the rapid expansion of supply in related industries. Although coal is also a relatively profitable industry in terms of investment returns, due to strict approval processes, increasing capital entry barriers, and the long conversion cycle from investment to supply, industry supply growth is more constrained.

Chart 1: The coal industry's ROE remains at a high level, better than most industries in the market.

Source: Wind, China International Capital Corporation Research Department.

Chart 2: Under the "impossible triangle" of coal, it is difficult to achieve a perfect balance among safety, production volume, and costs.

Source: Research Department of China International Capital Corporation

Chart 3: Since 2017, the proportion of new real estate loans has decreased, while the proportion of new loans related to infrastructure and manufacturing has increased.

Source: Wind, China International Capital Corporation Research Department.

Fundamentals support the valuation of the coal sector.

In the short term, coal prices are expected to remain strong. The central price may experience a slight decline next year, but will still remain at high levels.

Thermal Coal: Although demand related to the real estate chain has been relatively weak this year, the demand for power coal and chemical coal has continued to grow steadily. Due to the reduction in production in Shanxi, domestic coal supply has been disrupted. Despite the improvements in hydroelectricity affecting power coal demand this year, port coal prices have still fluctuated around 840-900 yuan/ton. Looking ahead, benefiting from the peak season for power coal and strengthened policy expectations, in the short term, we believe that coal prices are expected to remain strong during the heating season. If daily consumption recovers better than expected, prices may rise. Next year, considering that demand momentum may still mainly focus on gradual recovery, with marginal incremental supply, the central price of coal may experience a slight decline compared to this year. In the long term, a relatively healthy supply-demand pattern is expected to support power coal prices at historically relatively high levels.

Coking Coal: The decline in coal production in Shanxi this year has caused significant disruption to the domestic supply of coking coal. However, the substantial growth in imported coal, especially Mongolian coal, has eased the tight supply situation domestically. With the recovery in production in Shanxi since May and weak downstream demand, the pressure on coking coal prices has increased, with the main port coal prices touching 1,700 yuan/ton, returning to pre-COVID-19 levels. Looking ahead, considering the possibility of a more relaxed real estate policy and stronger fiscal policy, we believe that the situation of weak demand for coking coal may improve, supporting stable coal prices. However, with the possibility of increased supply next year, the central price of coal may also decline compared to this year.

Chart 4: Quarterly Performance of Major Coal Varieties Prices

Note: As of November 22, 2024, 4Q24

Data Source: Coal Resources Network, IHS McCloskey, China International Capital Corporation Research Department

Coal enterprise profit expectations stabilize, supported by a healthy balance sheet that facilitates dividend distribution.

The decline in coal enterprise profits narrows, with profit expectations improving. Due to factors such as the downward shift in coal prices and production cuts in certain regions, the operating profit of the coal mining and washing industry in 1-3Q24 decreased by 21% to 473.7 billion yuan. At the level of our sample listed companies, the net income attributable to the parent company decreased by 22% to 117 billion yuan year-on-year. Despite the narrowing decline in coal prices, industry profitability is gradually stabilizing, with listed companies' net profit attributable to the parent company in 3Q24 at 38.9 billion yuan, a year-on-year/half-yearly change of -9.3%/+3.9%. Single-quarter profits still exceed the levels of the same period before 2021.

Coal enterprises have relatively ample cash flow and maintain healthy debt levels. Although coal enterprise cash flow has declined from its historical highs in 2022, it remains at a relatively high level overall. The combined operating net cash flow of sample listed coal companies in 1-3Q24 decreased by 4.5% to 218.4 billion yuan year-on-year, with more than enough coverage for investment and interest expenses. Against this backdrop, the industry's overall debt levels remain relatively low, with an overall interest-bearing debt ratio of approximately 30% for sample listed coal companies as of 3Q24, a net debt ratio of about -3%, and a net debt ratio after excluding China Shenhua of only 7%.

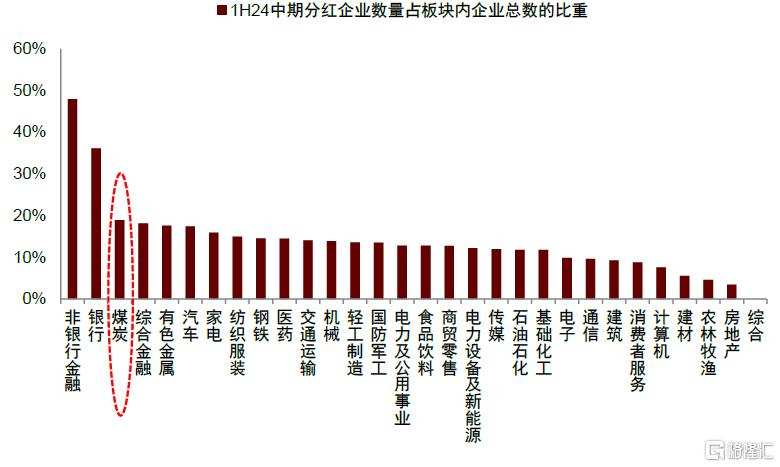

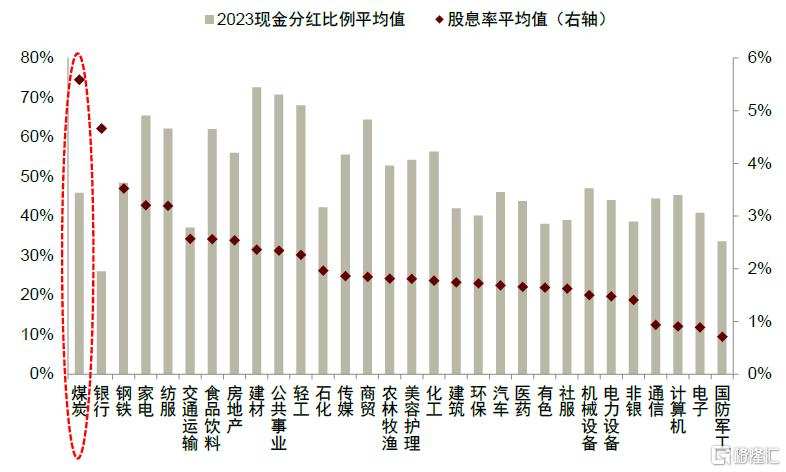

Stable and sustainable dividends. The proportion of coal companies implementing mid-term dividends in 2024 accounts for 19% of the total number of companies in the coal sector, second only to the non-banking financial and banking sectors. Some leading coal enterprises have also distributed mid-term dividends for the first time, reflecting the active response of coal companies to the regulator's call to reasonably increase investor returns. This also demonstrates the dividend distribution capability of coal enterprises. Looking ahead, on the basis of an overall sound fundamental outlook, we expect the coal industry to continue to provide stable and sustainable dividend distributions.

Chart 5: The decline in profits of the coal industry has narrowed.

Note: Samples are taken from 34 listed coal companies.

Source: Wind, China International Capital Corporation Research Department.

Chart 6: Cash flow of the coal sector.

Note: Samples are taken from 34 listed coal companies.

Source: Wind, China International Capital Corporation Research Department.

Chart 7: Healthy debt situation in the coal sector.

Note: The sample is taken from 34 coal listed companies, data source: Wind, China International Capital Corporation research department.

Chart 8: Proportion of mid-term dividend-paying companies in 2024 compared to the total number of sector companies.

Source: Wind, China International Capital Corporation Research Department.

Coal sector valuation remains attractive.

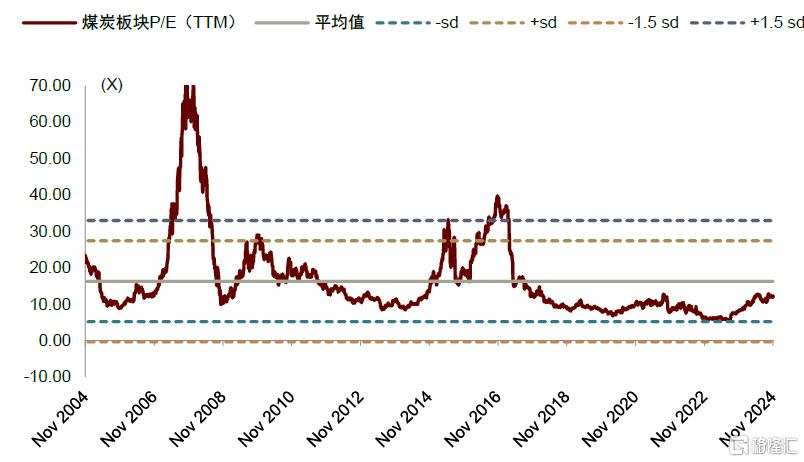

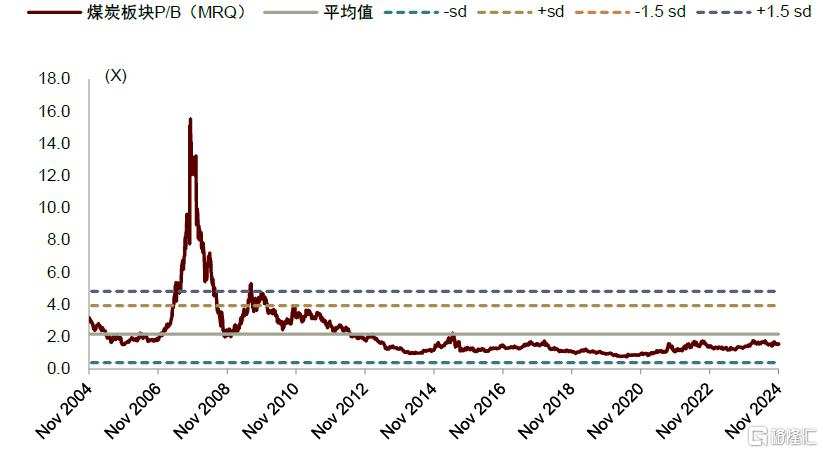

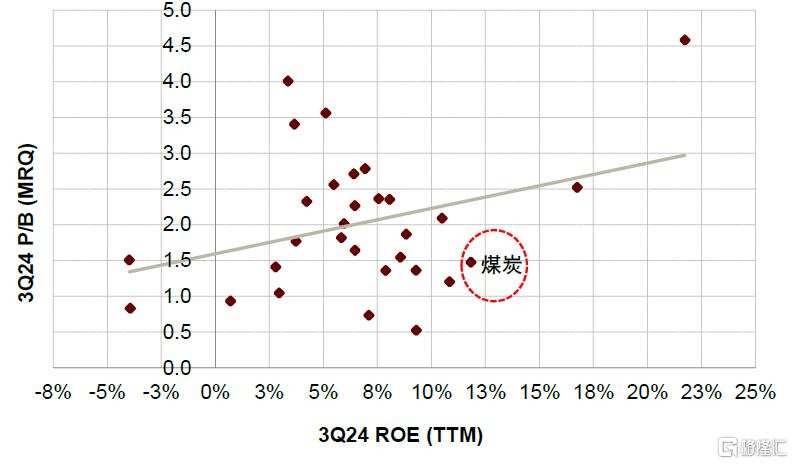

Coal valuation is not high. Vertically, the coal sector valuation is not high. As of November 22, the coal sector P/E (TTM) is 11.9x, lower than the 20-year average of 16.3x, at the 48th historical percentile, sector P/B (MRQ) is 1.5x, lower than the 20-year average of 2.2x, at the 48th historical percentile. Horizontally, the coal sector still holds investment value, with a comparison of ROE (3Q24 coal sector ROE (TTM) still at 12%). We believe there is still room for the sector's valuation to increase, additionally, the coal sector's dividend yield is ahead, providing a higher margin of safety.

Chart 9: P/E (TTM) of the coal sector in the past 20 years

Note: As of November 22, 2024

Source: Wind, China International Capital Corporation Research Department.

Chart 10: P/B (MRQ) of the coal sector in the past 20 years

Note: As of November 22, 2024

Source: Wind, China International Capital Corporation Research Department.

Chart 11: Sector PB (MRQ) vs roe (TTM)

Note: Valuation data as of November 22, 2024, Source: Wind, China International Capital Corporation Research Department

Chart 12: Sector Dividend Ratio and Corresponding Dividend Yield

Note: As of November 22, 2024

Source: Wind, China International Capital Corporation Research Department.

Coal demand is resilient

Steady growth in coal demand, with chemical industry supporting non-power coal consumption

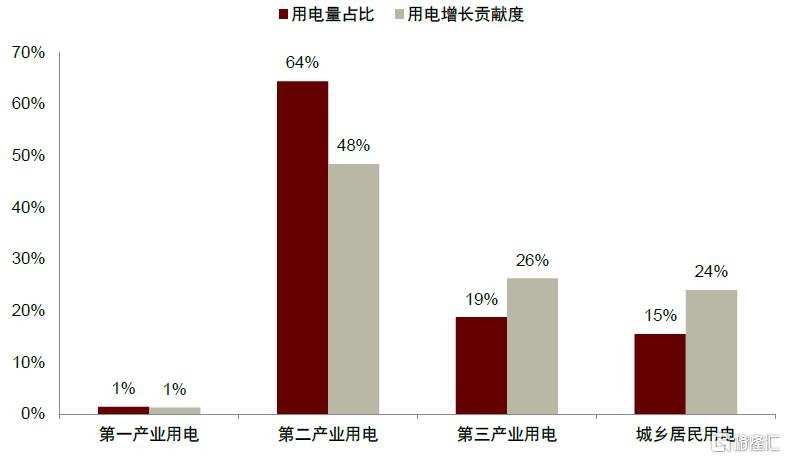

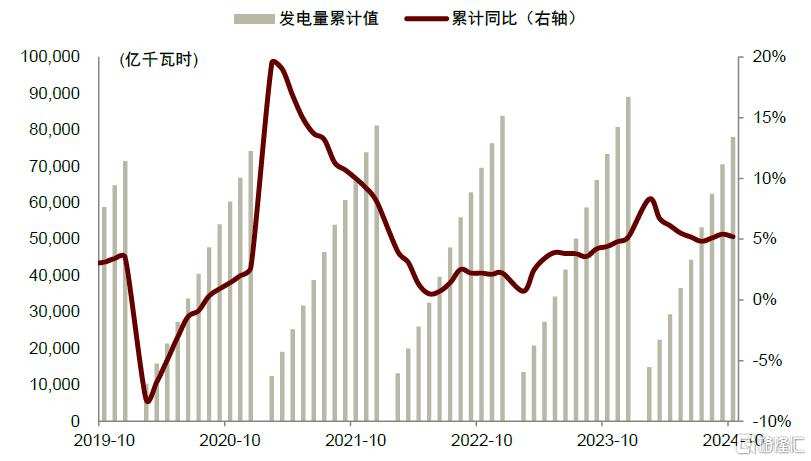

Electricity demand maintains rapid growth. In the period of January-October 2024, the total electricity consumption reached 8183.6 billion kilowatt-hours, a year-on-year increase of +7.6% (compared to +5.8% YoY in 10M23). Among them, second industry electricity consumption steadily increased by +5.6% to 5772.1 billion kilowatt-hours, accounting for 64% of the total national electricity demand, contributing 48% to the total electricity demand growth; third industry electricity consumption grew rapidly by +11.0% to 1531.5 billion kilowatt-hours, accounting for 19% of the total national electricity consumption, while the growth contribution rate reached 26%, reflecting to a certain extent the rapid development of industries such as information technology and new energy driving electricity demand. Electricity consumption for urban and rural residents also maintained rapid growth, increasing by +12.3% to 1265.9 billion kilowatt-hours, reflecting the improvement in electrification levels and the boosting effect of extreme weather conditions on electricity demand.

Chart 13: Total electricity consumption in January-October 2024 increased by +7.6% year-on-year

Source: Wind, China International Capital Corporation Research Department.

Chart 14: Total electricity consumption and incremental structure from January to October 2024

Source: Wind, China International Capital Corporation Research Department.

Thermal power is dragged down by hydropower, but hydropower weakened after July. From January to October 2024, the national cumulative power generation (above designated size) increased by +5.2% year-on-year to 7802.7 billion kilowatt-hours, of which thermal power generation increased by +1.9% year-on-year to 5223.1 billion kilowatt-hours. The main reason for the weak growth of thermal power is the improvement in hydropower. During the same period, hydropower generation increased by +12.2% year-on-year to 1110.1 billion kilowatt-hours, especially in the second quarter of 2024, hydropower generation increased by +38% year-on-year to 342.2 billion kilowatt-hours, and in the third quarter of 2024, it increased by +11% year-on-year to 451.4 billion kilowatt-hours. However, after July, the Yangtze River Basin experienced a rapid change in drought and flood conditions. According to water conservancy statistics, from August to October, the precipitation in the basin was 30% lower than the historical average for the same period since 1961. It was the second lowest since complete measurement data was available [1], and against this backdrop, national hydropower generation gradually weakened.

Chart 15: 2024 national cumulative power generation from January to October above designated size.

Source: Wind, China International Capital Corporation Research Department.

Chart 16: 2024 national cumulative thermal power generation from January to October above designated size.

Source: Wind, China International Capital Corporation Research Department.

Traditional demand for cement, steel, etc., is weak, and the contribution of the chemical industry to non-electric coal demand growth. 1) Cement shipment rate is in a low operation: Real estate is still in a process of stabilization, coupled with slow progress in infrastructure physical engineering, cement demand has been running at low levels this year. From January to October 2024, cement production was 1.5 billion tons, down by -10.3% year-on-year; 2) Steel production declined: The steel industry is still affected by the weak demand from real estate and infrastructure, with crude steel production from January to October 2024 down by -3.0% year-on-year to 0.851 billion tons, and molten iron production down by -4.0% year-on-year to 0.715 billion tons; 3) High growth in chemical coal consumption: Against the background of coal chemical industry capacity releases and the relatively high price difference between oil and coal, chemical coal consumption has maintained rapid growth this year, with CCTD data showing that the average coal consumption for chemical industry is approximately +9% year-on-year since the beginning of the year (up to 11-15).

The growth of coal demand is still promising, and we look forward to marginal improvement in non-power demand.

There is rigid growth in coal demand.

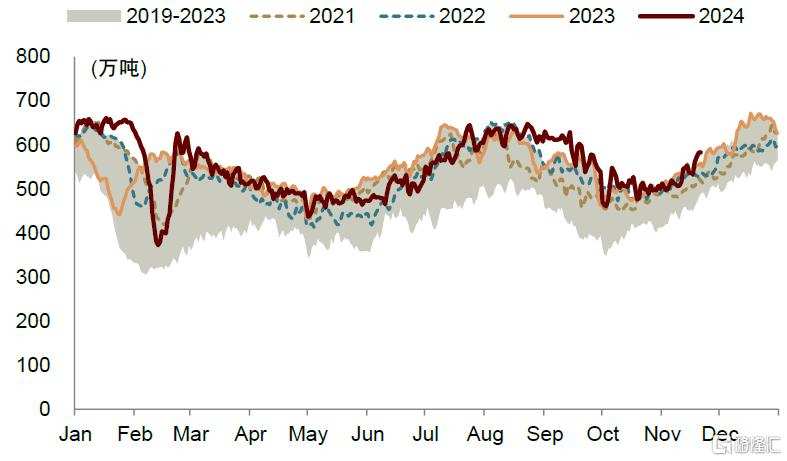

This winter and early spring will provide support for coal demand. Although in the second quarter of 2024 hydroelectric power is strong and coal is under pressure, due to high temperatures and droughts in some areas after July, hydroelectric power rapidly weakened, leading to strong support for coal demand. This resulted in coal consumption remaining exceptionally strong at a high level at the end of the "peak summer" period, downstream coal inventories have been partially cleared, creating some space for replenishment in the heating season. In the short term, we are optimistic about the seasonal increase in coal consumption, and coal demand is expected to remain strong this winter and early spring. However, the intensity of daily coal consumption growth may still need further monitoring of climate trends, as the China Meteorological Administration predicts above-average temperatures in most parts of the country from December to February of the following year.

Chart 17: Coal consumption per day for end users in twenty-five provinces is entering an upward trend.

Note: Data is up to November 21, 2024.

Source: CCTD, China International Capital Corporation Research Department

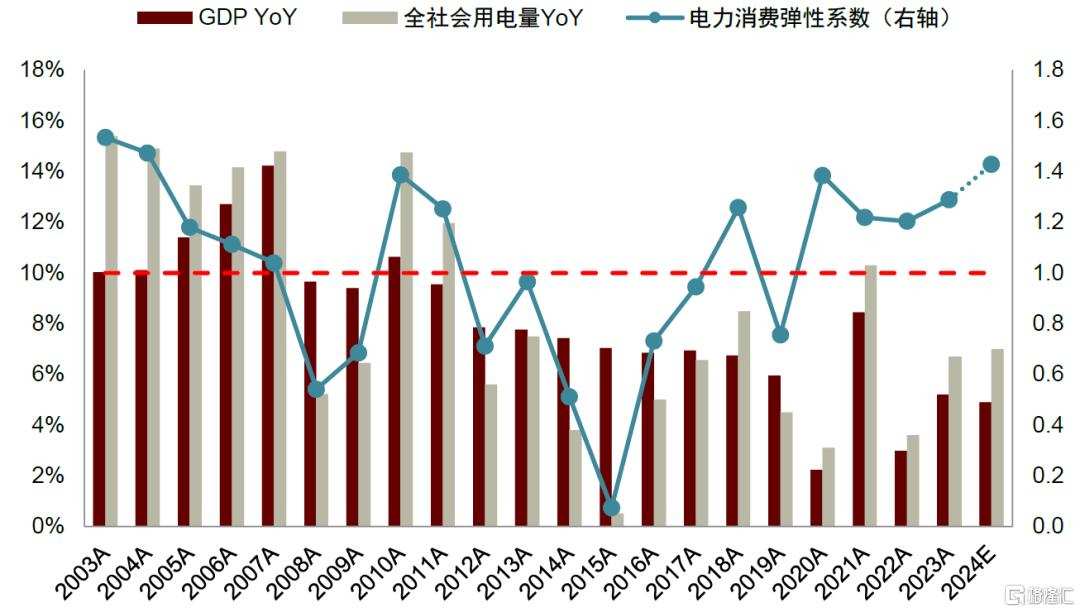

Electricity demand is expected to maintain rapid growth. Considering the demand for electricity growth exceeding expectations under the impact of high summer temperatures this year, the China Electricity Council raised its forecast for domestic power demand in 2024 by the end of October, with the year-on-year growth rate of total social electricity consumption revised from the previously expected +6.5% to +7.0%. This is 0.3 percentage points higher than the actual growth rate in 2023. If combined with China International Capital Corporation's forecast for domestic GDP growth (2024E +4.9% YoY vs. 2023A +5.2% YoY), the elasticity of electricity consumption in 2024 might even be higher than last year. Looking ahead, apart from the impact of extreme weather, we believe that the core reasons for this include the transition of old and new economic drivers and the improvement of electrification levels. Therefore, we expect domestic electricity demand to maintain rapid growth in the future.

Chart 18: Combining the judgments of CDEP and CICC Macro Research, domestic electricity demand elasticity may remain at a relatively high level.

Information Source: Wind, CDEP, CICC Research Department.

Chart 19: In terms of the proportion of electricity consumption, the electricity demand in the real estate and infrastructure sectors appears to be weak, while the emerging manufacturing and service industries show growth momentum in electricity demand.

Source: Wind, China International Capital Corporation Research Department.

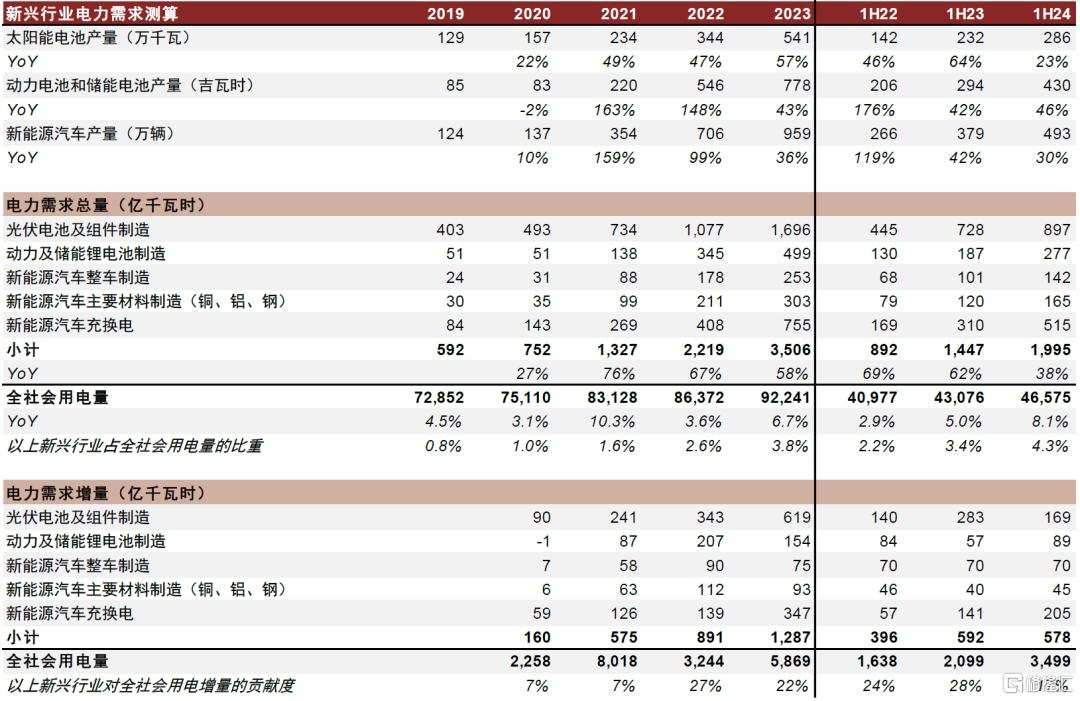

The growth of electricity demand in the new energy equipment and new energy vehicle related industry chains may account for over 20% of the total domestic electricity demand increment. In 2023, the total electricity consumption of the whole society increased by +586.9 billion kilowatt-hours year-on-year. We roughly estimate that over 20% of this increase may come from industries such as photovoltaic equipment, new energy vehicle manufacturing, and charging and swapping services. Considering that we only calculated the electricity consumption in key segments of these industries and did not include primary material smelting processing and charging and swapping equipment manufacturing, we believe that the total electricity consumption ratio of the entire industry chain upstream and downstream may be higher than the proportion we estimated. In terms of trends, the electricity consumption growth of these industries in the first half of this year has slowed to a certain extent, but it still maintains double-digit growth. Looking ahead, with the continuous increase in the penetration rate of new energy equipment and new energy vehicles, we expect these industries to continue to drive domestic electricity demand.

Artificial intelligence and other technological innovations are nurturing new growth points for electricity demand. Artificial intelligence, as an important part of new productivity, has broad long-term development space. We believe that the continuous expansion of computing power behind it is expected to drive electricity demand growth. In the baseline scenario, the International Energy Agency expects that by 2024, the electricity consumption of data centers, digital currencies, and artificial intelligence will increase from 460 billion kilowatt-hours in 2022 to 800 billion kilowatt-hours in 2026. The CICC Research Department predicted in the "ESG Industrial Chain Research Series (1): From computing power to green computing power - where is the transformation power, and what is the impact?" that by 2025, domestic data center electricity consumption will surpass 400 billion kilowatt-hours, a slight increase from 270 billion kilowatt-hours in 2022.

Chart 20: We calculate that the electricity demand growth of emerging industries such as photovoltaic, power and energy storage batteries, new energy vehicle manufacturing, and new energy vehicle charging and swapping is relatively fast.

Note: 1) The electricity consumption in the production process of power and energy lithium battery manufacturing does not include the electricity consumption in the upstream material production process, such as smelting and processing of nickel, cobalt, petroleum coke, needle coke, and other upstream raw materials manufacturing; 2) Only the electricity consumption of key processes is calculated.

Data sources: Wind, State Grid Corporation of China, government official websites, company announcements, International Copper Association, International Aluminium Association, China Photovoltaic Industry Association, Semiconductor Research Institute of Chinese Academy of Sciences, China International Capital Corporation research department.

Coal power demand still has room for growth. Combining economic growth and electricity demand forecasts, we estimate that the total electricity generation in 2025 may increase by around +6.5% year-on-year. Considering the possible fast growth of renewable energy in electricity generation, improvement in hydropower generation, we calculate that coal power still has growth potential, with an estimated year-on-year increase of around +3.5% for total coal power in 2025.

Chart 21: We expect coal power to still have room for growth in 2025.

Information Source: Wind, CDEP, CICC Research Department.

Chemical industry contributes to the growth of non-power coal.

Steel and cement demand may see marginal improvement. We believe that as policies gradually strengthen and special bond issuance accelerates, physical workload may increase, and the weak situation of steel and cement demand is expected to marginally improve. However, the extent of improvement still needs to observe the pace of policy implementation.

Continuous increase in coal chemical capacity supports the demand for coal used in chemicals. Since the start of this year, the oil-coal price ratio has remained relatively high, benefiting the start of coal chemical projects. In addition, from a policy perspective, in the context of a complex geopolitical situation, the country is paying increasing attention to the supply security of key raw materials. Many large coal chemical projects have been approved in the past two years, to some extent reflecting the country's support for the development of coal chemicals to address potential supply chain risks in petrochemicals. With the expansion of coal chemical capacity, we believe that the impact of chemicals on non-power coal is expected to be further highlighted. However, we also caution that the policy proposals of the new US government may increase the risk of oil price declines, thereby affecting the oil-coal price ratio and causing disruptions to the start-up rate of coal chemical projects.

Chart 22: Low operating rate of petroleum asphalt, to some extent reflecting the slow progress of infrastructure physical work.

Note: Data as of November 22, 2024.

Data source: National Bureau of Statistics, General Administration of Customs, Longzhong Petrochemical, China International Capital Corporation Research Department.

Chart 23: The oil-coal price ratio is similar to the same period last year, still at a relatively high level.

Note: Data is up to November 22, 2024; uniformly calculated in standard coal caliber.

Source: Company announcements, China International Capital Corporation Research Department

Domestic supply is steadily releasing.

There are constraints in the medium and long term.

Although the production has marginally improved, stability remains the main focus for the whole year, with limited potential growth in the future.

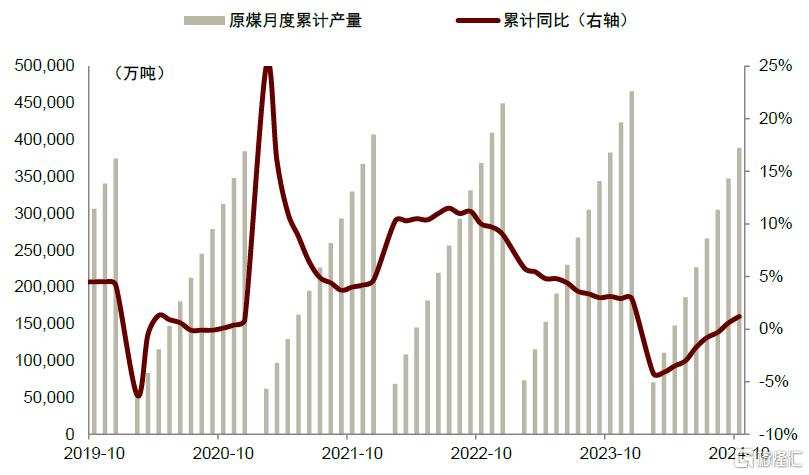

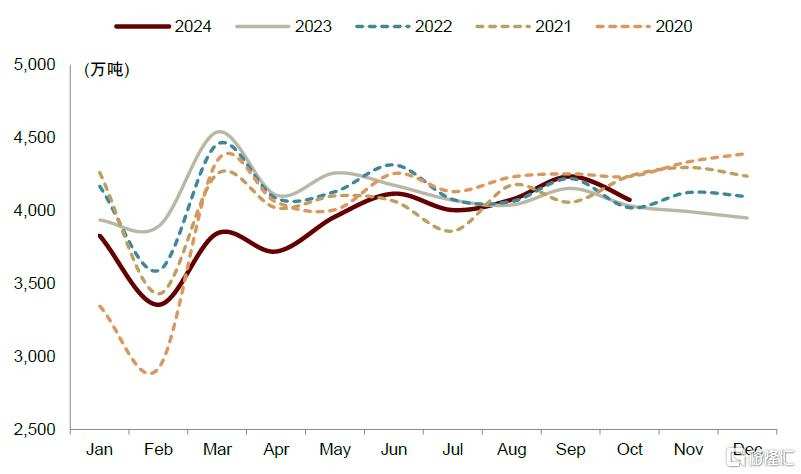

Coal production has marginally improved, but the production pace remains stable. National Bureau of Statistics data shows that the coal production in October was 411.8 million tons, +4.6% year-on-year. From January to October 2024, the cumulative coal production reached 3.89 billion tons, +1.2% year-on-year. Since May, when Shanxi proposed to improve the quality and efficiency of coal, domestic coal production has gradually recovered. Looking ahead, to balance economic growth and production safety, we believe that the pace of coal production will still be mainly stable, with a steady recovery as the main theme in the short term.

Chart 24: Cumulative coal production

Source: Wind, China International Capital Corporation Research Department.

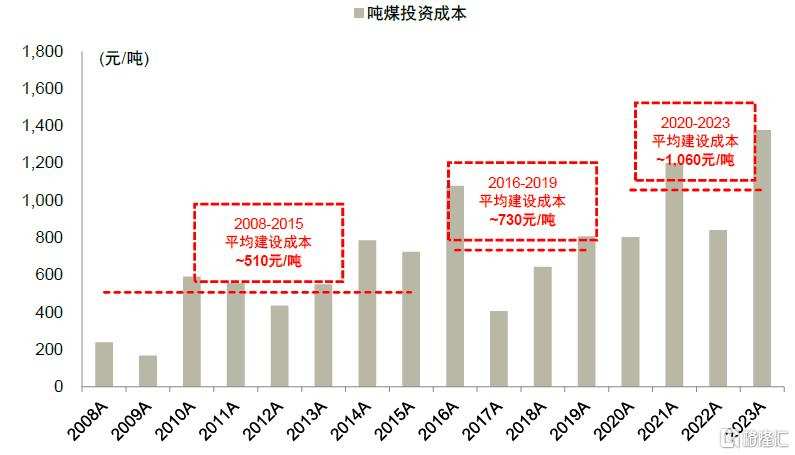

Potential supply increment is relatively limited. 1) High fixed asset investments are difficult to reflect the actual production capacity construction situation. From January to October 2024, the cumulative fixed asset investment in coal mining and washing industry increased by +8.6% year-on-year. In absolute terms, the capital expenditure of the coal industry is at a historical high, but considering that the investment includes enterprise maintenance expenses, mine intelligence, and investment in other business transformation and upgrading, and mine construction costs have increased significantly, we believe that the actual investment of coal enterprises in new mine construction may be relatively limited. More investments may be used for safety input, intelligent construction, and enterprise transformation and upgrading. For example, we have observed that the construction investment costs of coal approved projects since 2008 have increased. The construction cost per ton of coal for approved projects from 2020 to 2023 is about 1,060 yuan, which is 45% higher than the average cost of 730 yuan from 2016 to 2019.

2) The overall supply of new coal projects may be limited. Looking at the situation of coal projects approved by the National Development and Reform Commission and the Energy Bureau, since the proposal of 'dual carbon,' the approved production capacity of coal projects has decreased compared to the past. The average approved production capacity from 2020 to 2023 is around 40 million tons per year, which is half of the average level of over 80 million tons per year from 2008 to 2019. This reflects that under the green transformation, the country is not only guiding rational coal consumption from the demand side but also maintaining a relatively cautious attitude towards supply release.

Chart 25: Fixed asset investment in coal mining and washing industry.

Source: Wind, China International Capital Corporation Research Department.

Chart 26: Statistics of approved coal projects show an increase in coal construction expenditure per ton

Note: 1) Excluding mining rights fees; 2) From 2008 to 2023, a total of 242 projects approved by the National Development and Reform Commission and the Energy Bureau were used as statistical samples, with a total capacity of 1.19 billion tons.

Data source: Coal resources network, NDRC, Energy Bureau, CICC Research Department

Regional mismatch constrains supply, xinjiang coal cost supports coal prices

We expect that as coal supply in some traditional production areas gradually decreases, especially in the central and western regions, xinjiang's coal resources are expected to be further developed. With energy consumption still concentrated in the eastern region, we believe that factors such as capacity and transportation costs may provide support for the bottom of coal prices.

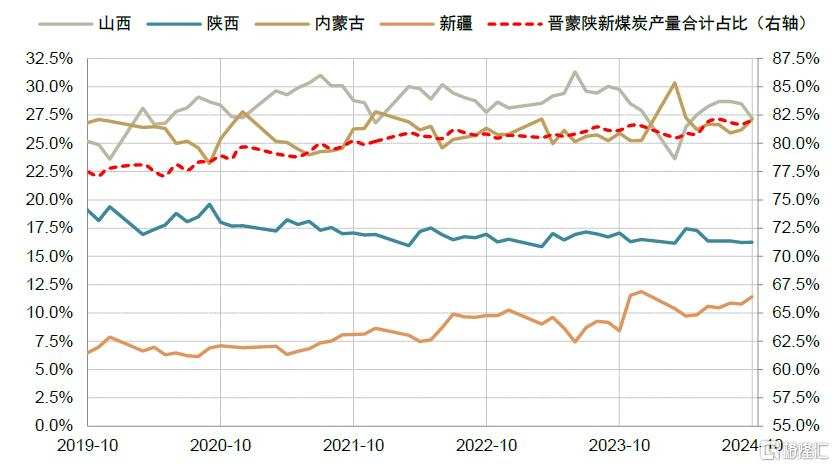

► Supply continues to concentrate in the central and western regions. During January to October 2024, the raw coal production in the four major producing areas of Inner Mongolia, Shanxi, Shaanxi, and Xinjiang was 10.61, 1.045, 0.641, and 0.425 billion tons respectively, with year-on-year changes of +6,231, -8,389, +988, and +75.65 million tons, respectively. The four areas together account for 81% of the total domestic raw coal production. Except for Shanxi being affected by production cuts, the other three major producing areas continue to release capacity. At the same time, due to factors such as coal mine safety accidents and natural depletion, the production in Anhui, Heilongjiang, Yunnan and other places declined. Considering the relatively limited and geologically complex potential developable resources in the eastern, northeastern, southwestern regions, we believe that the domestic coal supply may continue to show a trend of expansion in the west and decline in the east, and territorial supply-demand mismatch still exists. In the long term, we believe that the problem of territorial mismatch is expected to be gradually alleviated through transport capacity expansion, ultra-high pressure, resource local transformation, etc., but in the short term, transportation remains a hard constraint on coal supply.

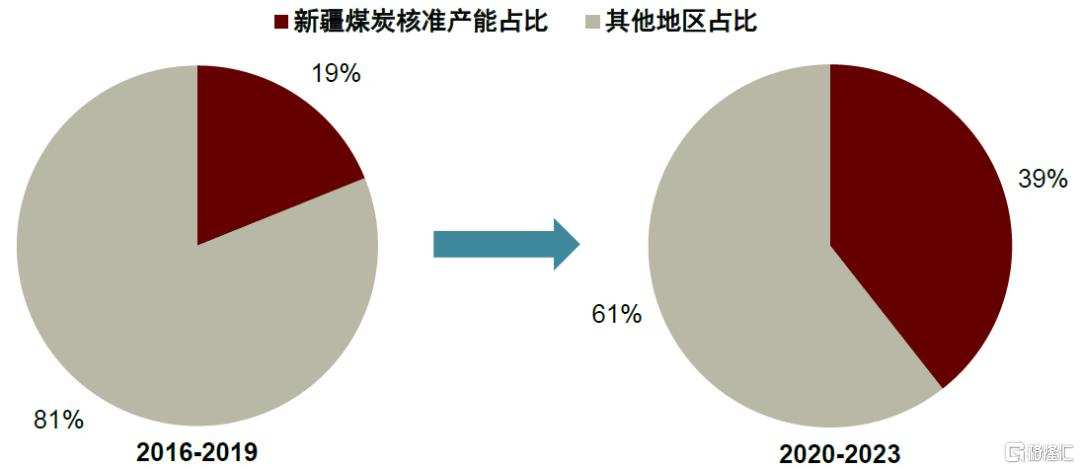

► Xinjiang coal's supply guarantee capability increases, and rigid transportation costs support coal prices. From January to October 2024, Xinjiang's cumulative production accounted for 10.9% of the national total, an increase of 1.1 percentage points from 9.8% in 2023, and 4.6 percentage points from 6.3% in 2019. Looking ahead, we expect Xinjiang's coal production and external shipping volume to steadily increase, further enhancing the importance of supply. Changes in coal project approvals also reflect the long-term trend of increased supply of xinjiang coal. During 2020-2023, the total capacity of coal projects approved in the Xinjiang region accounted for nearly 40% of the total capacity involved in projects approved nationwide during the same period, compared to less than 20% in 2016-2019. With the increase in xinjiang coal, we expect its rigid transportation costs to provide support for the bottom of coal prices. We roughly estimate that the transportation cost of xinjiang coal to northern ports is around 650 yuan/ton (xinjiang coal mainly radiates nearby areas, but the price at the port and the pit has a linked relationship, so estimating the cost to the port can also provide some reference value), considering the pit cost of xinjiang coal, we estimate that the spot price at the port may need to be around 750 yuan/ton to fully ensure the enthusiasm for xinjiang coal shipping.

Figure 27: The proportion of coal production in Shanxi, Shaanxi, Inner Mongolia, and Xinjiang regions is steadily increasing

Source: Wind, China International Capital Corporation Research Department.

Chart 28: From the perspective of coal approved projects, we expect more supply increment in the medium to long term to come from Xinjiang.

Data source: National Development and Reform Commission, Energy Bureau, Coal Resource Network, China International Capital Corporation Research Department.

Chart 29: Calculation of coal transportation costs in Xinjiang.

Data source: Wind, China Railway 95306 website, company announcements, China International Capital Corporation Research Department.

Import structure growth, cost support overseas coal prices.

The growth rate of coal imports narrowed, with high-calorific value thermal coal and primary coking coal imports expected to continue to be limited.

Imports maintain double-digit growth, with incremental contributions from Australia and Mongolia. From January to October 2024, China's cumulative coal imports increased by +13.5% year-on-year to 0.435 billion tons, maintaining double-digit growth since early 2023. Structurally, Indonesia, Australia, Mongolia, and Russia are the main sources of coal imports for China, accounting for 92% of China's total coal imports from January to October. The import increase mainly comes from Australia and Mongolia. Due to cost, transportation, and other reasons, imports of Russian coal have decreased. By category, from January to October, the import volume of non-coking coal (i.e., thermal coal) increased by +32.94 million tons or +11% year-on-year, with most of the increase coming from Australia; coking coal imports increased by +18.12 million tons or +22% year-on-year, with 60% of the increase from Mongolia and Australia.

There is still growth potential in total imports, but the increase in high-calorific value thermal coal and premium primary coking coal may be limited. Considering that overseas natural gas prices remain relatively high, and marginal costs also provide some support for overseas coal prices, we believe that high-calorific value imported thermal coal may maintain a price inversion state with domestic coal, constraining the improvement of the coal import structure. Due to the relatively slow recovery in Australian coking coal supply, we expect that in the short term, the increase in domestic high-quality primary coking coal imports may also be relatively limited.

Chart 30: Division of coal import sources

Data Source: Coal Resource Network, China International Capital Corporation Research Department

Chart 31: Major sources of coal imports by type

Data Source: Coal Resource Network, China International Capital Corporation Research Department

Global coal demand growth, with supply disruptions

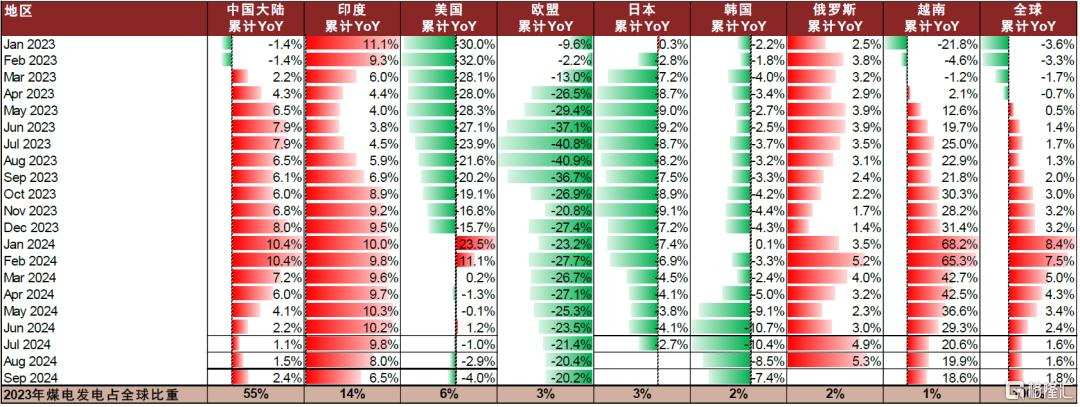

Global coal-fired power demand continues to grow, with transportation constraints and geopolitical conflicts disrupting supply. From a demand perspective, global thermal coal consumption still shows resilience, mainly contributed by emerging markets such as China, India, and Vietnam. Ember data shows that the global coal-fired power generation in the first three quarters of 2024 increased by +1.8% year-on-year. In China, coal-fired power demand is steadily growing; driven by demand, India's coal-fired power maintains rapid growth, while Vietnam's coal-fired power demand also recorded significant growth due to industrial expansion and extreme weather conditions. From a supply perspective, Indonesia's coal exports continued to grow in the first three quarters of 2024, but at a slower pace than last year; Australia's coal exports saw a slight increase; with the gradual resumption of navigation at the Port of Baltimore in late May, the United States' coal exports accelerated; Mongolia's coal exports maintained rapid growth; however, geopolitical conflicts and transportation capacity issues constrained Russia's coal exports; disruptions in railroad transportation also affected coal exports from South Africa, Canada, and other regions.

Chart 32: Global regions' coal-fired power generation growth rate in the first three quarters of 2024

Note: Blank spaces indicate incomplete data

Source of information: Ember, China International Capital Corporation Research Department

Chart 33: Coal export growth rates in major global regions for the first three quarters of 2024.

Note: The statistical scope for the coal export volume and year-on-year growth rate of Russia in the chart is sea coal exports, with Russia's total coal export volume in 2023 at around 0.21 billion tons.

Data sources: IHS McCloskey, Kpler, China Coal Economic Network, Research Department of China International Capital Corporation.

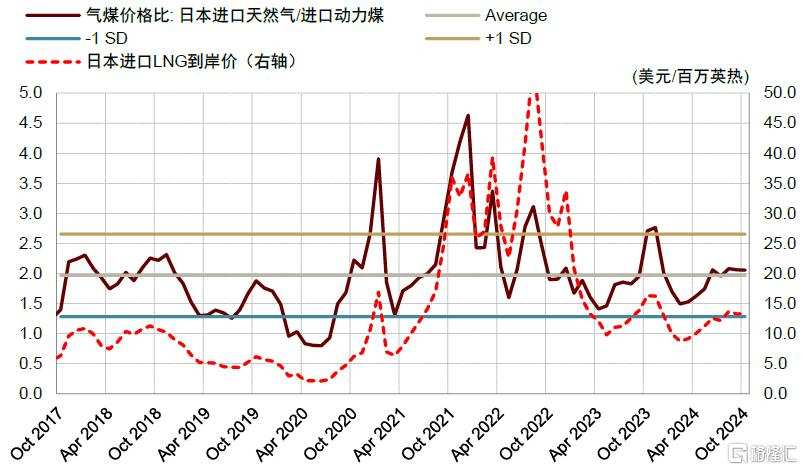

Overseas natural gas prices have fallen from historical highs but are still relatively high.

Natural gas has maintained a relatively high level in the short term, supporting the price of thermal coal. Overseas thermal coal prices are closely related to overseas natural gas prices. Although the current natural gas prices have fallen from the extreme high in 2022, they are still relatively high in historical terms. With relatively frequent supply disruptions and marginal demand improvement, natural gas prices in Europe and Japan have risen this year. Looking ahead, we believe that overseas natural gas supply is still subject to geopolitical uncertainties and may continue to fluctuate at a relatively high level in the short term, which is expected to provide some support to the price of overseas thermal coal.

Chart 34: European gas prices rebound, providing support for local coal prices.

Sources: IHS McCloskey, Investing.com, China International Capital Corporation Research Department

Chart 35: Asia-Pacific gas prices rebound, providing some support for regional thermal coal prices

Sources: IHS McCloskey, Wind, China International Capital Corporation Research Department

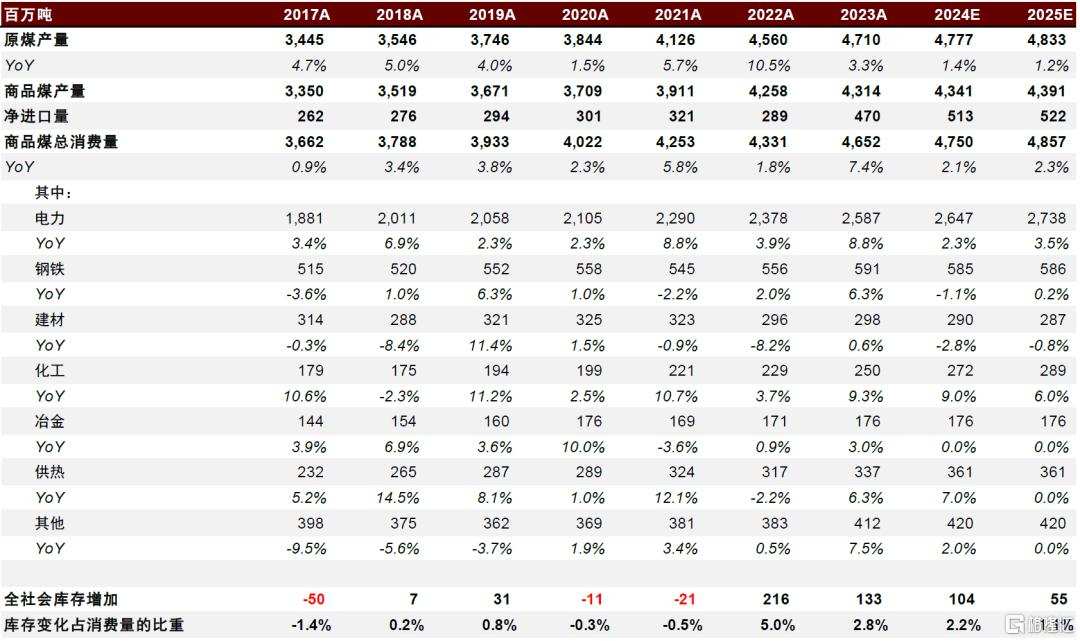

Healthy supply and demand support keep coal prices at historically relatively high levels

By 2025, coal supply and demand are expected to remain balanced, with coal prices staying at historically relatively high levels. Looking ahead to 2025, we believe coal demand is expected to grow steadily. Specifically, assuming: 1) Under high elasticity in electricity demand, and with marginal recovery in hydropower, next year's demand for thermal coal may increase by 3.5%; 2) For non-power coal, countercyclical adjustments boost efforts, with coal demand for steel, construction materials expected to gradually stabilize, and chemical coal demand maintaining rapid growth due to capacity additions.

On the supply side, we believe major producing regions will continue to balance economic growth and safety production. Assuming Shanxi's supply continues to recover but may still not reach 2023 levels throughout the year, next year's national raw coal output may increase by 1.2% under this background. In terms of imports, we expect total imports to continue to grow, but imports of high calorific value thermal coal, high-quality coking coal may still be limited. Overall, we expect the coal supply and demand to be generally balanced, with the possibility of a slight downward shift in the center of coal prices, but still at historically relatively high levels.

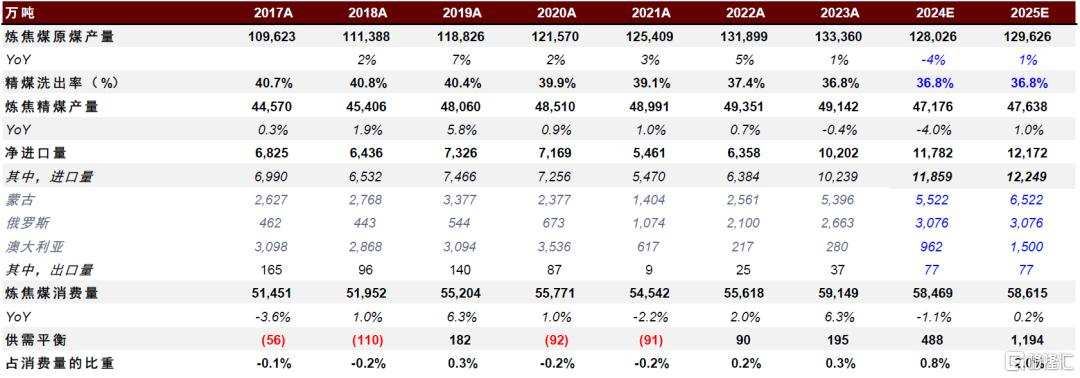

Chart 36: Coal supply and demand balance sheet

Sources: coal resources network, Wind, China International Capital Corporation research department.

Coking coal: reality is weak, expected to lead.

In the short term, we believe that demand is the core determining factor of coking coal prices. Stimulated by favorable policies, coking coal demand is expected to recover first in 3Q24, driving coal prices to rebound. However, weak reality remains, with insufficient dynamic for coking coal prices due to slow recovery in pig iron production + Shanxi's recovery-induced increased production, prices have fallen back to levels before the COVID-19 pandemic. Looking ahead, if demand recovery is further implemented, we believe the tight supply and demand balance and scarcity of resources characteristic will help coking coal prices rebound.

In the long term, we believe that tight supply of high-quality coking coal will support coal prices. On one hand, with the depletion of existing mine resources and declining coal quality, we judge domestic coking coal supply has basically peaked, with weak supply elasticity and further downside risks, especially in high-quality prime coking coal, which is facing obvious structural and regional scarcity issues. On the other hand, with the extension of mining depth, the difficulty of mining and potential safety hazards increasing, we believe that the coal industry's "impossible triangle" may be more pronounced in the coking coal sector. Against the backdrop of stricter safety supervision, coal enterprises may struggle to balance production volume and costs, potentially leading to a scenario of either "maintaining costs -> reducing production volume" or "maintaining production volume -> increasing costs", both of which directly or indirectly support coking coal prices.

Steel's high-quality development demands higher standards for dual coke quality, and high-quality coking coal is scarce. In the coking process, the general proportion is 35% prime coking coal, 15% fat coal, and the rest is blended coal; according to "Characteristic Distribution of Scarce Coking Coal Resources in China" (Deng Xiaoli, 2018), in 2018, the proportion of reserves of prime coking coal and fat coal in China was 18% and 8%, respectively, and the proportion of coking raw coal output in 2023 is 23% and 7%. From the perspective of reserves and output, China's prime coking coal exhibits structural scarcity issues. Looking ahead, the higher demands placed on dual coke quality by steel's high-quality development: on the one hand, with the trend of domestic blast furnace largescaleization, the coke CSR index (i.e. hot strength) is becoming increasingly important, with a positive correlation between the proportion of prime coking coal and CSR generally, furnace capacity enhancements driving demand for prime coking coal; on the other hand, for high-strength steel such as special steel products, there are higher thresholds for sulfur content standards, and low sulfur, high volatile matter coal helps reduce sulfur content in coke.

Demand: reality is weak, waiting for demand to recover.

Demand continues its weak trend. Against a backdrop of pessimistic demand expectations, black series prices have faced significant pressure overall since the beginning of this year, with coking coal prices being resilient. The spread between coke and steel profits has shrunk, further lowering operating rates, causing the industry chain to be dragged into sustained negative feedback, thus hampering coking coal demand. We believe that further easing of real estate policies, accelerated issuance of special bonds may drive demand to gradually recover, but the pace of recovery needs further observation.

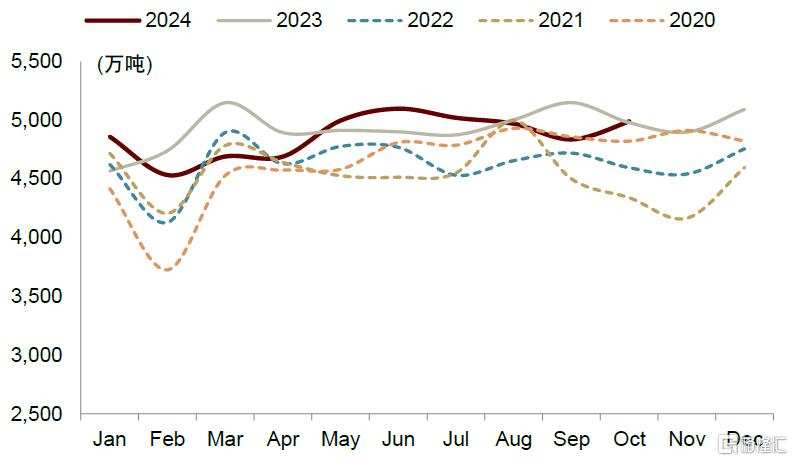

Chart 37: Monthly consumption of refined coke nationwide

Data Source: Coal Resource Network, China International Capital Corporation Research Department

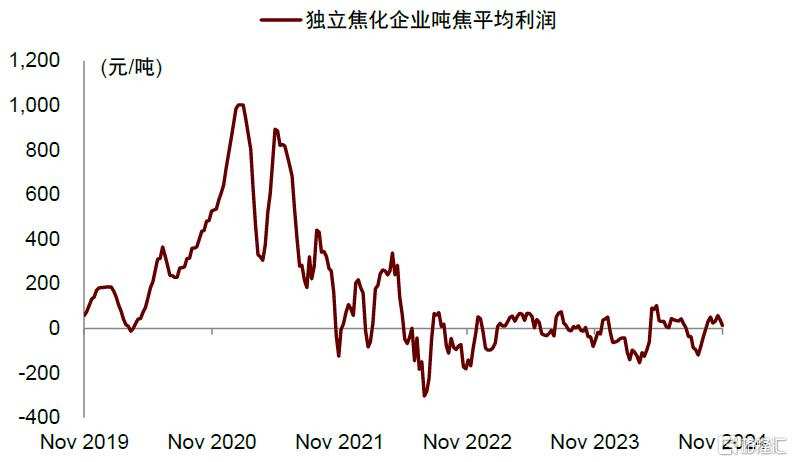

Chart 38: Profits per ton of coke are at the edge of loss

Source: Wind, China International Capital Corporation Research Department.

Chart 39: Profit per ton of steel declines, to a certain extent reflecting the continued weakness in architecture engineering demand, while manufacturing demand remains relatively robust

Source of Information: Mysteel, China International Capital Corporation Research Department

Supply: The inadequate elasticity of high-quality primary coking coal supply highlights its scarcity

The situation of insufficient supply elasticity is difficult to change. In 2023, Shanxi contributed around 25% of the national thermal coal supply and ~47% of the coking coal supply. In 2023, Shanxi produced 1.378 billion tons of coal, with the 'Notice on the Work Plan for Stabilizing Coal Production and Supply in Shanxi Province in 2024' proposing a provincial coal production target of around 1.3 billion tons in 2024, a target that is -78 million tons lower than the actual production in 2023. In May 2024, to consolidate economic growth and achieve the annual production target, Shanxi encouraged some mines to speed up production under the premise of ensuring safety. From January to October, Shanxi's raw coal production decreased by 7% year-on-year (or -83.9 million tons), with Shanxi's coking coal production decreasing by 7% year-on-year (or -14.4 million tons, accounting for 73% of the national decrease). In terms of production recovery progress, since August, Shanxi's coking coal production has returned to a level close to the same period in 2023. Looking ahead to 2025, considering stricter safety supervision, we believe that stabilizing production and supply will be the main theme, and the possibility of a significant release of supply from Shanxi compared to the current level is relatively limited. The situation of insufficient elasticity in coking coal supply may still be difficult to change.

Most newly approved projects are for thermal coal, with limited increase in coking coal production capacity. From the perspective of new projects, in the past three years, most of the coal projects approved by the country are for thermal coal; from the perspective of listed companies, the increase in supply of coking coal enterprises relies more on the injection of group assets, with fewer coking coal mines under construction. Therefore, we expect that within the visible range in the next 3-5 years, the market is unlikely to see a significant release of new supply.

High-quality coking coal is becoming increasingly scarce, and the increased cost of resource acquisition raises the threshold for increasing supply. According to the 'Long-term Supply and Demand Forecast Research on Coking Coal in China' (Li Liying, 2019), by 2017, the average recoverable life of coking coal in China was 26 years. Coal mines in production are facing exhaustion issues, especially the difficult issue of obtaining high-quality primary coking coal. In addition, the yield of coking coal has declined, mainly due to the deepening of coal mine mining, leading to higher ash content and sulfur content, increasing the difficulty of washing. Against this background, the scarcity of domestic coking coal resources continues to be highlighted, with a significant increase in mining rights acquisition costs and a corresponding increase in the threshold for capital entry.

Chart 40: Monthly supply of coking coal in the country

Data Source: Coal Resource Network, China International Capital Corporation Research Department

The main increase in imports comes from Mongolia, but the thermal intensity of the coal quality is limited, and the price advantage has also been somewhat weakened. The main increase in China's coking coal imports is still from Mongolia. In the report 'Approaching Mongolia's Coal: The Rhythm of the 'Black Gold' on the Northern Plateau', we predict that under the improvement of production and transportation conditions, Mongolia's coal supply will still have growth space in the next three years, with the annual increment expected to exceed 10 million tons. Australia and Russia have limited expansion space domestically, so the incremental supply is expected to be relatively stable. However, structurally, although the quality of Mongolian coal is at a medium to high level, with indicators such as ash content and sulfur content being good, the thermal strength (CSR) indicator is slightly insufficient, restricting its operation in large blast furnaces and making it difficult to be a direct replacement for high-quality domestic prime coking coal. Therefore, we predict that there may still be a structural shortage of high-quality coking coal domestically. In addition, considering that the price of high-quality Mongolian coking coal has basically become comparable to domestic prime coking coal prices, the price advantage has diminished. We expect that the increase in Mongolian coal may be more affected by fluctuations in domestic coal prices.

Chart 41: Coke Supply-Demand Balance Sheet

Data Source: General Administration of Customs, Coal Resources Network, Research Department of China International Capital Corporation

This article is excerpted from 'Coal 2025 Outlook: Ready to Attack and Defend, Timing is Key' published by China International Capital Corporation on November 30, 2024. Analysts:

Chen Yan CFA Analyst SAC Certificate Number: S0080515060002 SFC CE Ref: ALZ159

Xu Yunyan Analyst SAC Certificate Number: S0080524070009