投机者开始重建日元空仓

投机者开始重建日元空仓The bet on shorting the Japanese yen increased to $13.5 billion in November, once again reviving the yen carry trade that once shook the global market.

Yen arbitrage trading - an investment strategy that has been very popular this year, is making a comeback.

According to Bloomberg's analysis of data from the Japan Financial Futures Association, Tokyo Financial Exchange, and the U.S. Commodity Futures Trading Commission, Japanese retail investors as well as foreign leveraged funds and asset management companies are estimated to have increased their put bets on the yen from $9.74 billion in October to $13.5 billion in November.

Speculators are starting to rebuild their short positions on the yen.

Speculators are starting to rebuild their short positions on the yen.

Due to significant interest rate differentials, increased borrowing by the U.S. government, and relatively low currency market volatility, these bets are expected to increase next year. Under these conditions, the practice of borrowing in Japan and then investing funds in the global high-yield markets becomes more appealing.

Alvin Tan, Head of Asia Foreign Exchange Strategy at Royal Bank of Canada in Singapore, said: "The absolute interest rate differential of other currencies relative to the yen is very large, which means it will always be seen as a funding currency. The main reason it is not used as the funding currency for arbitrage trading is volatility."

Strategists at Mizuho Securities and Saxo Markets stated that arbitrage trading may return to levels seen earlier in the year, with investors abruptly exiting this trade after the Bank of Japan raised rates in July. One thing to note is that Trump's return to power may lead to turmoil in the currency markets.

The widespread adoption of this investment strategy could impact global markets. The yen arbitrage trading liquidation in the summer wiped out approximately $6.4 trillion from global stock markets in just three weeks, and the Nikkei 225 index experienced its largest decline since 1987. Last week's sudden surge in the yen highlighted the sustained risks faced by investors engaging in re-buying arbitrage trades.

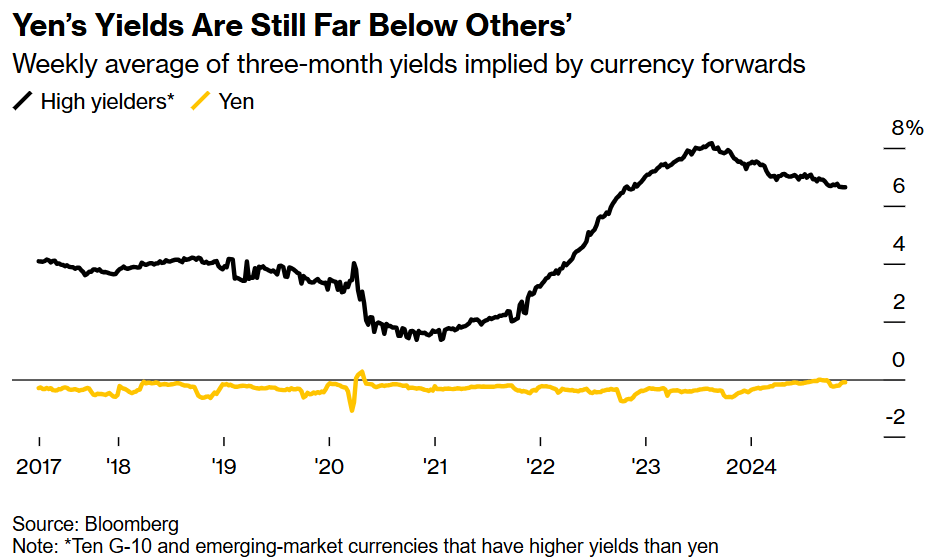

Interest rates are the driver of such trades. The average yield of the top ten G7 and emerging market high-yield currencies exceeds 6%. In contrast, the Bank of Japan's benchmark interest rate is only 0.25%, with the yield on the yen nearly zero.

The yield on the yen lags far behind other currencies.

Although the Bank of Japan is gradually raising interest rates, its yield gap with major economies like the USA remains significant. The Federal Reserve cut rates by 25 basis points in November to a range of 4.5%-4.75%. Felix Ryan, a forex analyst at the Bank of Australia and New Zealand in Sydney, believes that even if Japan raises rates to around 1%, the logic for arbitrage trades remains valid.

This strategy has been very profitable. Since the end of 2021, the yen arbitrage trading targeting the top 10 major currencies and emerging market currencies has yielded 45%, compared to the S&P 500 index return of only 32% considering dividend reinvestment.

This has attracted more and more arbitrage investors, with yen short positions reaching $21.6 billion by the end of July (i.e., before a massive liquidation).

Charu Chanana, Chief Investment Strategist at Shengbao Market, said, "The Bank of Japan’s rate hikes are unlikely to be enough to narrow the yield gap between Japan and the USA. With US debt and fiscal conditions clearly a key concern for the incoming Trump administration, yen arbitrage trading may still have an attractive space to maintain."

In recent months, the US dollar and US Treasury yields have surged, as people speculate that Trump's tariffs and tax policies will boost the economy and inflation, possibly slowing the pace of Fed rate cuts.

Market concerns eased somewhat after Trump nominated Scott Bessent as Treasury Secretary. However, Shoki Omori, Chief Strategist at Tokyo Mizuho Securities Japan, believes that Trump will ultimately decide US fiscal policy.

"Fundamentally, everything is related to Trump," Omori said, he believes arbitrage trading could make a comeback as early as January next year. "People have forgotten the power risk Bezenet poses to Trump. If Bezenet wants to continue in office, I don't think he will be so rigid on budget issues."

The threat of a trade war led by Trump could also drag down global assets, especially after last week's vow to impose additional tariffs on China, Canada, and Mexico.

While the Mexican peso has long been the preferred currency for yen arbitrage trading due to the country's double-digit interest rates, Trump's remarks could create enough volatility to make this trade less attractive.

This is important because yen-financed arbitrage trading benefits from lower exchange rate volatility. A Morgan Chase indicator measuring foreign exchange volatility has fallen from its post-epidemic peak. Despite the increased uncertainty of the new Trump administration, the conflict in Ukraine has escalated.

Global foreign exchange market volatility remains low.

However, some believe that the narrowing interest rate differential will keep the momentum of arbitrage trading low next year, especially after BOJ Governor Haruhiko Kuroda opened the door for a rate hike in December. Japanese officials are also cautious about the yen, with the Finance Minister stating last month that the yen has experienced sharp one-way volatility since late September.

Due to continued structural issues such as substantial outflows of capital putting pressure on the yen, the yen has been the worst performer among G10 currencies this year. Despite reaching 140 levels against the dollar a few months ago in the context of interest rate differential trade closing out, it has now returned to around 150.

Jane Foley, Foreign Exchange Strategy Director at Rabobank, said: "The Japanese Ministry of Finance has reconnected with speculators through verbal interventions, and BOJ Governor Haruhiko Kuroda's remarks have kept market concerns about a rate hike in December. Although arbitrage trading has received further support, this should ensure that arbitrage trading lacks clear confidence and momentum in the spring of next year.

Before the meetings of the Bank of Japan and the Federal Reserve in December, investors may have a further understanding of arbitrage trading. Utada's dovish tone or Fed Chairman Powell's hawkish tone, as well as any hints of key data points, may attract arbitrage traders back into the market.

Omori said, "The Bank of Japan's interest rate hike speed will be slow, and if Powell does not intend to reduce interest rates quickly, then the interest rate differential will be very attractive for arbitrage trading."

The Japanese Ministry of Finance is not so aggressive, if they "remain silent, investors will feel there is no reason not to engage in such trading."