当“更大幅度的减重”策略式微,GLP-1巨头们如何打出差异化?“更健康的减重”成为了巨头们当下更核心的迭代策略选择,减脂增肌无疑是这个策略中的“种子选手”。肌肉流失是目前GLP-1药物最常见的副作用之一,临床研究表明:接受GLP-1药物治疗的患者,其肌肉流失速度远快于通过饮食或运动减肥的人群,这导致潜在的骨折风险、心血管风险增加等各种健康问题。

当“更大幅度的减重”策略式微,GLP-1巨头们如何打出差异化?“更健康的减重”成为了巨头们当下更核心的迭代策略选择,减脂增肌无疑是这个策略中的“种子选手”。肌肉流失是目前GLP-1药物最常见的副作用之一,临床研究表明:接受GLP-1药物治疗的患者,其肌肉流失速度远快于通过饮食或运动减肥的人群,这导致潜在的骨折风险、心血管风险增加等各种健康问题。The competition for GLP-1 weight loss drugs has become intense. The domestic biotech company, Lai Kai Pharmaceutical (02105), is expected to be the first to share the huge global market for fat loss and muscle gain.

The competition for GLP-1 weight loss drugs has become intense.

Now, in the past, giants competed by promoting greater weight loss, but this approach's marginal effect is diminishing. In November, Viking Therapeutics announced VK-2735 weight loss data showing 'best-in-class' potential, yet the stock price saw its largest single-day drop since March of this year.

As the strategy of 'greater weight loss' wanes, how will GLP-1 giants differentiate themselves? 'Healthier weight loss' has become the core iterative strategy choice for these giants, with fat loss and muscle gain undoubtedly being the 'seed players' in this strategy. Muscle loss is currently one of the most common side effects of GLP-1 drugs. Clinical studies have shown that patients receiving GLP-1 treatment lose muscle much faster than those losing weight through diet or exercise, leading to an increased risk of fractures, cardiovascular risks, and various health issues.

As the strategy of 'greater weight loss' wanes, how will GLP-1 giants differentiate themselves? 'Healthier weight loss' has become the core iterative strategy choice for these giants, with fat loss and muscle gain undoubtedly being the 'seed players' in this strategy. Muscle loss is currently one of the most common side effects of GLP-1 drugs. Clinical studies have shown that patients receiving GLP-1 treatment lose muscle much faster than those losing weight through diet or exercise, leading to an increased risk of fractures, cardiovascular risks, and various health issues.

As giants shift their focus and the fat loss and muscle gain route is preliminarily validated clinically, it has driven the elevation of fat loss and muscle gain target pipelines over the past two years, including scholar rock's stock price soaring 361.99% after announcing its MSTN antibody Apitegromab's Phase III data for spinal muscular atrophy, and Eli Lilly and Co acquiring the core pipeline for Bimagrumab (ActRIIA/ActRIIB antibody) from Versanis for $1.925 billion. However, the 'main wave' in this track has not yet arrived. Before the first half of 2025, there will be several significant catalysts in the global fat loss and muscle gain pipeline, including the completion of Phase II clinical trials of Eli Lilly and Co's Bimagrumab (hereinafter: Bima) in combination with semaglutide, as well as the reading of Phase II data for Regeneron's Trevogrumab (MSTN) and Garetosmab (Activin A antibody), while scholar rock's Apitegromab will also announce data for the combination with GLP-1 in treating obese patients in a Phase II trial. If the data exceeds expectations, the asset value of molecules in this sector will see a significant increase.

The domestic biotech company, Lai Kai Pharmaceutical (02105), is expected to be the first to share the huge global market for fat loss and muscle gain.

On November 20, Lai Kai Pharmaceutical signed a clinical cooperation agreement with Eli Lilly and Co, under which Eli Lilly and Co will be responsible for and bear the related costs of a Phase I study of LAE102 in the USA, with Lai Kai Pharmaceutical retaining global rights for LAE102. A savvy MNC would not have love without reason, and this clinical partnership between Eli Lilly and Co and Lai Kai Pharmaceutical is expected to lay a solid foundation for the first domestic fat loss and muscle gain drug to go abroad.

Why has LAE102 gained the favor of Eli Lilly and Co?

As a multinational corporation that has already acquired Bima and entered the fat loss and muscle gain sector, achieving a global leading position, Eli Lilly and Co cannot stand by and allow LAE102, a potential best-in-class product from Lai Kai Pharmaceuticals, to fall into the hands of other major weight loss drug companies.

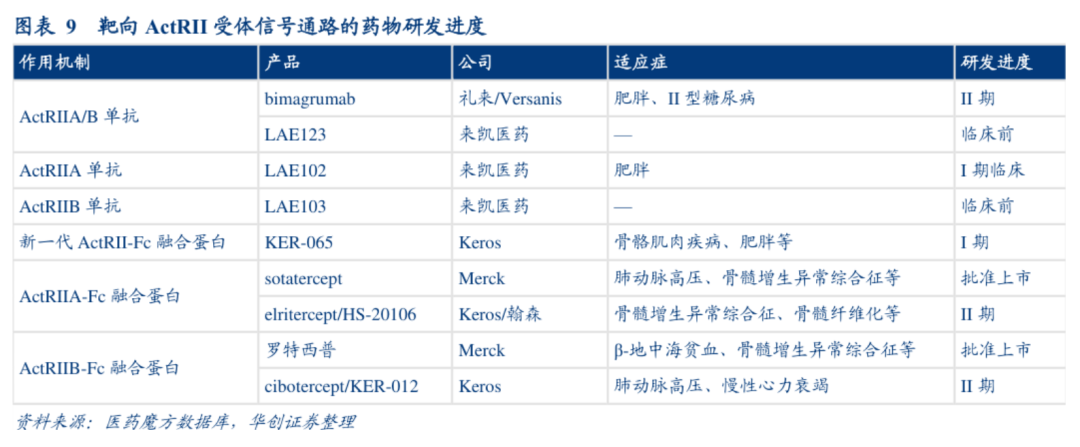

Currently, the only drugs that have entered clinical stages targeting the ActRII receptor globally are Eli Lilly's Bima and Lai Kai Pharmaceuticals' LAE102, while the remaining clinical pipelines under development target ActRII ligands. Research shows that blocking the ActRII pathway can inhibit muscle atrophy, and multiple ligands of ActRII have been proven to be negative regulatory factors for skeletal muscle, making the strategy of blocking the receptor more logically coherent and likely more effective than only blocking a single ligand.

In response to the strategy of blocking the ActRII receptor, Lai Kai Pharmaceuticals adopts a "multi-pronged approach." In addition to the highly anticipated clinical stage of LAE102 (ActRIIB antibody), the dual-target antibody LAE123 targeting ActRIIA/IIB has recently met the PCC requirements and officially entered the IND supportive research phase, along with the previously initiated IND supportive research for LAE103 (ActRIIB selective antibody). This allows the company to ensure a leading advantage while leaving space for trial and error, enabling comprehensive coverage of potential indications for the ActRII pathway.

Not only is the mechanistic logic coherent, but there are also no major issues regarding the druggability of ActRII receptor-targeted drugs. According to earlier published results from Eli Lilly's Bima 48-week Phase II clinical trial involving 75 overweight or obese patients with type 2 diabetes, the Bima treatment group experienced a weight reduction of only 6.5% compared to placebo, but it facilitated approximately 20.5% loss in fat content (comparable to the efficacy of Eli Lilly's Mounjaro) and increased lean body mass by 3.6%. More importantly, unlike typical GLP-1 drugs, no weight gain was observed within 12 weeks of stopping treatment in the Bima treatment group.

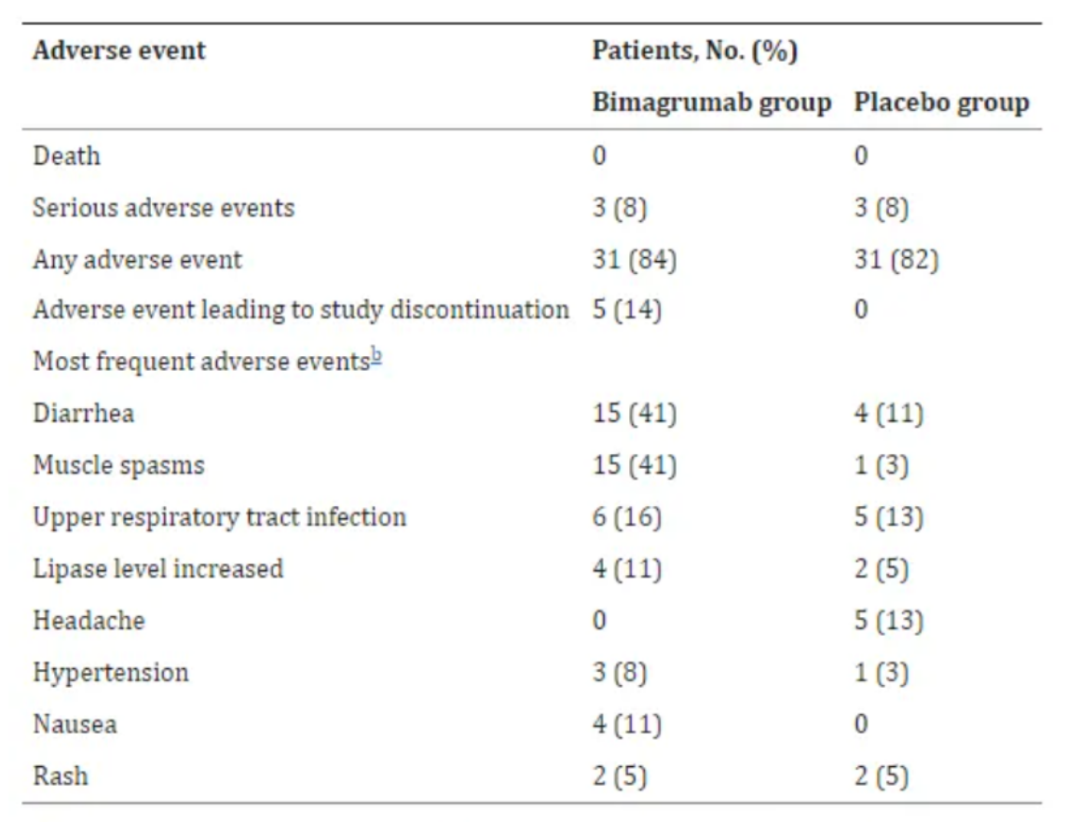

Despite its powerful weight loss and muscle gain effects, Bima is not without its drawbacks, which also presents more opportunities for optimization or iteration for later entrants. Novartis's clinical data on Bima published in JAMA in 2021 indicated that its core adverse events were mild diarrhea (41% vs 11%) and muscle cramps (41% vs 3%), with the highest frequency of diarrhea occurring after the first dose and gradually decreasing thereafter. Additionally, in the aforementioned Phase II clinical trial involving obese patients with type 2 diabetes, five patients experienced adverse reaction events that led to study termination, which adds more uncertainty for subsequent large sample clinical trials of Bima.

Why is LAE102 from laike pharmaceutical a potential best-in-class molecule?

1) Preclinical and early clinical indicators support: LAE102 has already shown potential for increasing muscle and reducing fat in preclinical studies, and its combination with GLP-1 receptor agonists can further reduce fat and significantly decrease muscle loss associated with GLP-1 receptor agonists. Laike Pharmaceuticals previously announced that early signs of target binding and expected PD biomarker changes can be observed at low clinical doses of LAE102, greatly increasing the likelihood of LAE102 producing excellent early clinical data.

2) The competition between ActRIIA and ActRIIB pathways is unclear (strong A or strong B): It is well known that Bima targets both ActRIIA and ActRIIB, but its binding activity with the ActRIIB receptor is far higher than with ActRIIA. Although previous studies have shown that myostatin is highly expressed in young muscle and is considered key in muscle growth regulation, myostatin has a higher affinity for ActRIIB than for ActRIIA. However, there is no conclusion on whether blocking receptor A or receptor B is more effective in reducing fat and increasing muscle.

Laike Pharmaceuticals' preclinical DIO model (diet-induced obesity model) data show that LAE102 has a significant effect on increasing lean mass, while another ActRIIB selective antibody LAE103 also shows efficacy in increasing lean mass, with LAE102 demonstrating even stronger effects. In the DIO model combined with semaglutide, LAE102 showed robust effects. These data strongly support LAE102's leap to becoming a potential best-in-class molecule in the field.

3) The convenience of subcutaneous injection: Currently, the best-selling GLP-1 products are pre-filled pen subcutaneous injections, and subcutaneous injection formulations are more convenient for weight loss patients to use in conjunction with GLP-1. LAE102 has initiated a subcutaneous registration cohort in Phase I clinical trials and is also the first-in-class in global clinical progress.

Additionally, the potential of LAE102 can also be validated and initially explored from other aspects. On one hand, laike pharmaceuticals' founder Dr. Lü Xiangyang is a co-inventor of Bima and has over 20 years of experience in ActRII research, with a greater probability of creating a better version of Bima. On the other hand, laike pharmaceuticals’ active promotion of LAE102's progress and quick clinical execution indicate that the company team has full confidence in and grasp of LAE102.

02 Eli Lilly and Co, the creator of big deals.

For laika pharmaceuticals, eli lilly and co is one of the only two best-fitting partners globally.

Looking at eli lilly and co's acquisition strategy for 2023-2024, it is characterized by acquiring 'early,' 'new,' and high premium acquisitions. Especially in the metabolic field, in July 2023, eli lilly and co acquired VersanisBio for 1.9 billion USD, while its core pipeline Bima was in the completed phase 2a clinical trials/ phase 2 enrollment; in June 2023, eli lilly and co acquired the diabetes cell therapy company Sigilon for a total consideration of 0.3096 billion USD, with a premium of over 400%, and at the time of acquisition, Sigilon's core pipeline had just entered clinical trials; and eli lilly and co recently reached an expanded cooperation worth 1.4 billion USD with KeyBioscience, where the core pipeline, a dual amylin calcitonin receptor agonist (DACRA) for treating obesity and osteoarthritis, had just completed phase 1 clinical trials. Now, laika pharmaceuticals' LAE102 is at an early clinical stage, which falls within the range of eli lilly and co's acquisition strategy.

The overseas clinical collaboration between eli lilly and co and laika pharmaceuticals regarding LAE102 inevitably leads investors to reasonably speculate: the clinical cooperation is just a 'start,' to lay the foundation, with both parties potentially having further cooperation or even reaching M&A.

Such speculation is not unfounded and is not uncommon in the cooperation between global MNCs, biopharma, and biotech. Taking eli lilly and co as an example, it reached a collaboration with Sigilon for the encapsulated cell therapy SIG-002 for type 1 diabetes treatment in 2018 (63 million USD initial payment + 0.41 billion USD milestone payments), and five years later acquired it for about 0.3 billion USD; similarly, regarding biontech's collaboration with domestic biotech PumiSi, in November 2023, they reached a global rights cooperation concerning the PD-L1/VEGF dual antibody PM8002, and a year later, PumiSi was wholly acquired by biontech.

It is not ruled out that laika pharmaceuticals and eli lilly and co may follow the aforementioned development path; perhaps everything needs to wait for the clinical data of LAE102 to materialize.

Secondly, many investors feel confused about eli lilly and co acquiring Versanis while also cooperating with laika pharmaceuticals on LAE102. In fact, the two transactions are not conflicting for eli lilly and co, as MNCs do not 'put all their eggs in one basket.' A very clear trend currently is that both eli lilly and co and novo-nordisk a/s are iterating and combining around GLP-1, aiming to strengthen their competitive advantage. The iterative direction of 'reducing fat and increasing muscle' and the feasibility of drug candidates in the ActRII pathway have been validated, so eli lilly and co's dual positioning strategy is a 'occupying' mindset and ensures not to miss out on major research paths in this domain, making sure that drug candidates or FIC candidates 'must be within my system.'

Similarly, this strategy is also observable in merck's aggressive investment in the 'IO+ADC' layout, as it collaborates simultaneously with Chugai Pharmaceutical and Kolon Life Science on ADC pipelines, striving to encompass various target ADCs available in the market.

From another perspective, for laika pharmaceuticals, eli lilly and co is one of the best global partners for LAE102, based on three levels: 1) As an MNC with various GLP-1 drugs on the market and in research, eli lilly and co possesses rich experience and resources in clinical design and clinical resources for overseas weight loss metabolic drugs. More importantly, in the future, LAE102 might accelerate overseas clinical development through the combination with eli lilly and co's marketed GLP-1, facilitating faster market entry; 2) Eli lilly and co's commercialization capabilities in the weight loss field are unquestionable. LAE102, positioned as a 'weight-loss companion,' has a synergistic relationship with the GLP-1 pipeline within eli lilly and co's ecosystem rather than a competitive relationship, thus it is expected to leverage the GLP-1 surge for rapid volume growth; 3) As a powerful MNC, future significant introduction of LAE102 or even a full acquisition of laika pharmaceuticals by eli lilly and co remains a possibility.

As investors and observers, we may just need to wait for the upcoming domestic clinical data of LAE102 and for further cooperation between lakai pharmaceuticals and eli lilly and co.

The initiative is in lakai's hands.

It is worth noting that despite collaborating with the giant eli lilly and co, lakai pharmaceuticals firmly holds the 'decision-making power' in its own hands.

Retaining global rights combined with a 0.23 billion HKD placement for refinancing highlights lakai pharmaceuticals' determination to 'grow larger and stronger' in this business development.

According to the statistics from guosheng pharmaceuticals, after 2018, the proportion of innovative drugs going overseas in china shows that preclinical projects account for 34-43%, phase I clinical projects account for 19-26%, post-market projects make up 22%-23%, while phase 2/3 clinical and application for listing stages both account for less than 10%. Generally, as clinical projects advance to later stages, the upfront payment amounts and total transaction values are larger.

Currently, lakai pharmaceuticals' LAE102 is in phase I clinical trials in china (data has not yet been read out), and is also in the early stages of clinical trials in the usa.

Choosing to collaborate clinically is equivalent to 'borrowing a ship to accelerate development'; on one hand, lakai pharmaceuticals utilizes resources from eli lilly and co to speed up LAE102's overseas clinical trials, while allowing the multinational corporation to handle core quality for the clinical verification pipeline; on the other hand, lakai pharmaceuticals can use this clinical collaboration to 'trade time for space', to maximize the balancing of licensing value risks, striving to sell the pipeline at the best price.

Many investors have questioned the timing of this placement, but in fact it is one of the best time windows for refinancing. Although lakai pharmaceuticals has at least 2 years of cash flow pipelines before refinancing, continuing to increase cash reserves allows the company greater strategic choices for clinical options (licensing out or continuing to push domestic clinical trials); more importantly, insufficient cash reserves will no longer be the main reason for potential overseas buyers to bargain down the company's asking price, adding more negotiation leverage for lakai pharmaceuticals in future large transactions.

At the same time, the potential trade partners for investors to consider for LAE102 should not be limited to eli lilly and co, novo-nordisk a/s, roche, and astrazeneca, as these MNCs all have GLP-1 product pipelines, and these giants are also quite interested in innovative molecules for weight loss and muscle gain.

There were reports from foreign media revealing that the buyer who initially engaged in in-depth negotiations with versanis (bima) last year was not eli lilly and co, but someone else, who was subsequently outbid at a high stock price by eli lilly and co.

Therefore, the decision on what price LAE102 will be BD at and which MNC to grant authorization to still firmly rests in the hands of laikae pharmaceuticals, which adds many different possibilities for the company's long-term development in the future.

From the analysis of potential trade type possibilities, besides the BD pipeline, it is not impossible for laikae pharmaceuticals to be acquired outright as versanis was, as MNCs are fond of acquiring platform-type biotechs. Laikae pharmaceuticals has laid out a series of "pipeline lines" including LAE102, LAE103, and LAE123 around the strategy of blocking the ActRII receptor. As the early data for LAE102 and the preclinical data for LAE123 are released in the future, laikae pharmaceuticals' platform attributes in the Activin signaling pathway may be strongly validated, which undoubtedly highlights the company's "platform性" and significant acquisition value.

Conclusion: With the widespread use of GLP-1 drugs, it is almost certain that the long-term growth trend of patients' demand for fat loss and muscle gain is established. The clinical cooperation between laikae pharmaceuticals and eli lilly and co is only a typical collaboration reflective of China's biotech sharing in the global weight loss market cake, but its long-term potential may also transform into a future huge BD transaction case or even a milestone event marking the acquisition of the first Hong Kong stock 18A biotech.

This article is reprinted from the "Gengling Society" WeChat official account, edited by Zhitong Finance: Jiang Yuanhua.