预计由于非OPEC供应增长,

预计由于非OPEC供应增长,

Bank of America Merrill Lynch expects that due to a significant increase in production from non-OPEC countries, coupled with the possibility of OPEC+ releasing more supply, the crude oil market may enter a surplus cycle, with the average annual price of Brent crude oil expected to be $65 per barrel. Basic metals are experiencing price fluctuations amid differentiated supply and demand. Driven by macroeconomic uncertainty and risk aversion sentiment, gold remains one of the most attractive precious metals in 2025.

What challenges will commodities face next year under the potential risks of weak global economic growth and US tariff policies?

The Bank of America Merrill Lynch analysis team pointed out in the "2025 Commodity Outlook" report released on November 24 that the trade war and a strong dollar may lead to a decline in commodity prices, but the differentiated performance will provide investors with more opportunities and challenges.

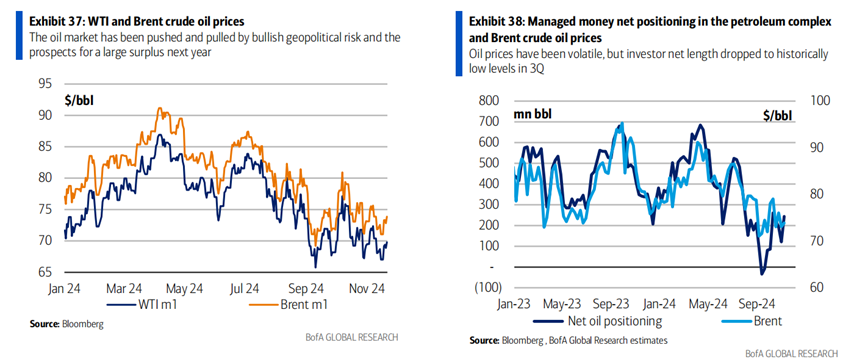

It is expected that due to the increase in non-OPEC supply, the global oil market will experience oversupply in 2025, with Brent crude oil prices possibly hovering around $65 per barrel. The growth in US natural gas supply and demand will further tighten inventories.

It is expected that due to the increase in non-OPEC supply, the global oil market will experience oversupply in 2025, with Brent crude oil prices possibly hovering around $65 per barrel. The growth in US natural gas supply and demand will further tighten inventories.

Base metals may see price fluctuations in supply and demand differentiation, while gold continues to strengthen due to macro uncertainty, with a target price set at $3,000 per ounce. Copper and aluminum prices may decline in the short term, then rise in the second half of the year.

Oil market: Non-OPEC supply growth dominates the market, overall demand growth is weak.

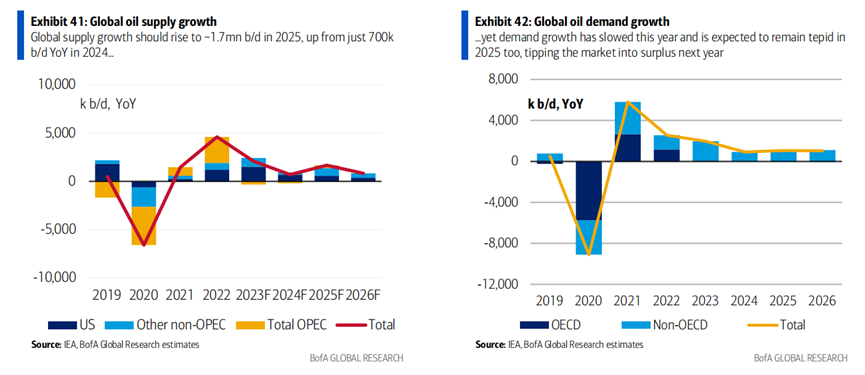

Bank of America Merrill Lynch predicts that global GDP will grow by 3.3% in 2025 and 2026. The global trade tensions may weaken economic activities in the first half of 2025 and harm the demand for most cyclical commodities such as oil and industrial metals. Overall, the main tone of the global energy market in 2025 is oversupply and slowing demand growth.

Due to a significant increase in production from non-OPEC countries, alongside OPEC+ potentially releasing more supply, the crude oil market may enter an oversupply cycle, with the average annual Brent crude oil price expected to be $65 per barrel and WTI at $61 per barrel.

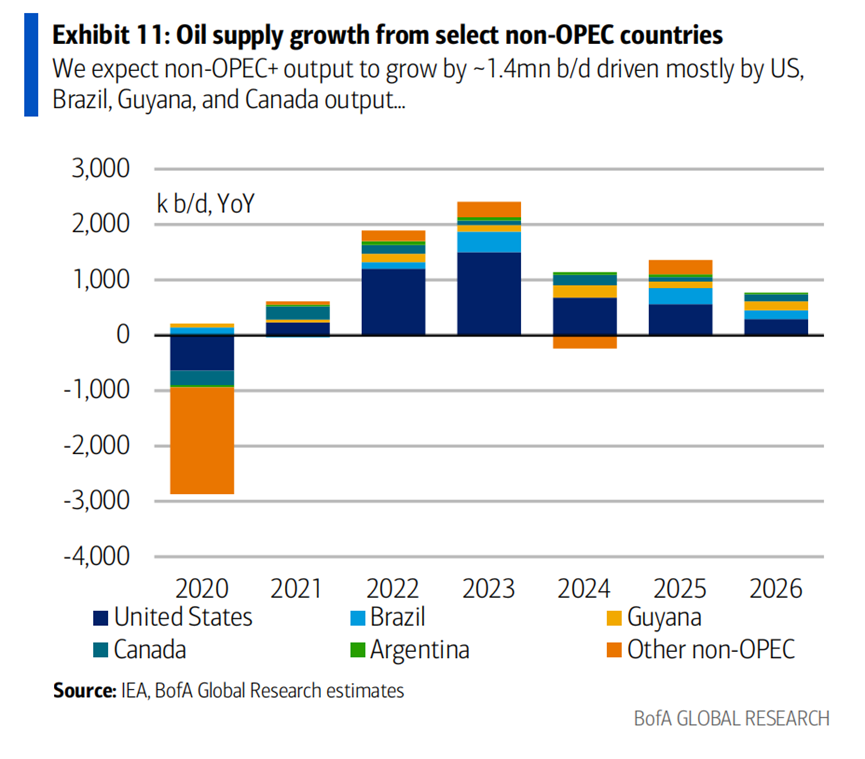

Specifically, the main sources of crude oil supply growth in 2025 will be the USA, Brazil, Canada, and Guyana. The recovery of shale oil production in the USA and the new capacity in the Gulf of Mexico will drive a year-round production increase of 0.35 million barrels per day in the USA.

In addition, Brazil's subsalt oil field projects will concentrate on production from 2024 to 2026, including several large FPSOs (floating production storage and offloading units) such as Mero 3 and Buzios 7, expected to contribute approximately 0.3 million barrels per day of new supply for Brazil. The Yellowtail project in Guyana is expected to start production in the second half of 2025, adding 0.12 million barrels per day of new capacity for the country.

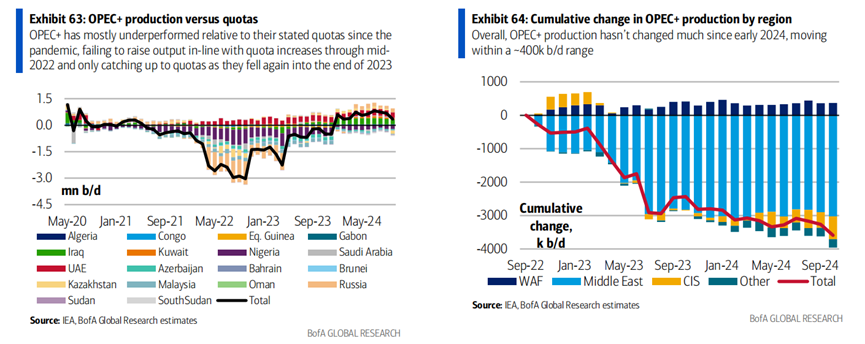

This will put pressure on OPEC+ from the production increase trends of non-OPEC countries. Although these countries may maintain market balance by adjusting production, their influence is gradually being weakened. The report forecasts that OPEC+ supply will only increase by 0.29 million barrels per day in 2025, far lower than the 1.4 million barrels per day increase from non-OPEC.

On the demand side, the slowdown in global economic growth, weak recovery in emerging markets, and a strong dollar have all suppressed oil demand. Bank of America Merrill Lynch estimates that global oil demand will grow by only 1.1 million barrels per day in 2025, which is significantly lower than the non-OPEC supply increase. Although geopolitical tensions in the Middle East may support oil prices in the short term, this impact is insufficient to offset the pressure from the supply-demand fundamentals.

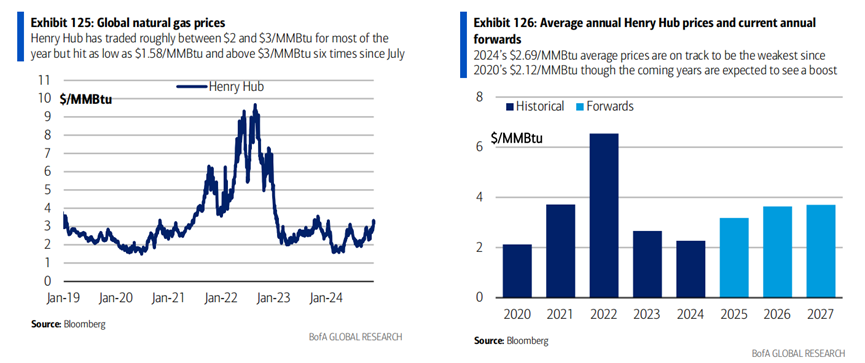

Henry hub natural gas: Tightening supply and demand drives price increases.

In contrast to the weakness in the crude oil market, the natural gas market may become a highlight in 2025. Bank of America stated that Trump's potential future policies may include the restoration of natural gas export licensing rounds, and the Federal Energy Regulatory Commission has already approved numerous liquefied natural gas export facilities.

Driven by increased winter demand and infrastructure development, the average price of US Henry Hub natural gas is expected to reach $3.33/MMBtu for the whole year, higher than the levels of 2024.

The LNG (liquefied natural gas) market is tightening further due to increased European import demand, especially in cases of cold weather or geopolitical escalation, which may trigger short-term price increases.

In addition, the transition to new energy also supports the natural gas market. As demand for LNG trucks and gas-fired power generation grows, the market position of natural gas becomes increasingly important in the energy structure adjustment.

Metal market: Energy transition and supply shortages shape price fluctuations.

The metal market faces a differentiating trend in 2025: the long-term demand growth from the energy transition counterbalances the supply chain tension, causing some metal prices to seek support amidst fluctuations.

Trade and tariffs have created a bearish backdrop for industrial metals, while China's stimulus measures may partially offset this impact.

Driven by macro uncertainties and a risk-averse sentiment, gold remains one of the most attractive precious metals in 2025. Bank of America Merrill Lynch expects that although a strong dollar and rising interest rates will suppress gold prices in the short term, the price of gold will break through $3000/ounce in the second half of the year due to rising global debt levels and increasing macro risks.

Bank of America pointed out four key policy aspects that will directly affect gold through interest rates and the dollar:

- Deregulation (bearish for gold): A broad deregulation that includes energy and financial services could provide a tailwind for economic growth, reflected in rising interest rates.

- Fiscal policy (bearish for gold): Personal tax cuts in the Tax Cuts and Jobs Act may be extended, and additional tax cuts may now be implemented, which would moderately boost short-term growth and create upward pressure on interest rates.

- Tariffs (bearish for gold): After Trump's inauguration, tariffs on his country may rise significantly in the short term. Concerns arise that if the domestic currency is pressured by tariffs, central banks in emerging markets will lack interest in continuing to increase their gold shareholding.

- Federal Reserve interest rate cuts (bearish for gold): Assuming the economic fundamentals remain solid, if significant tariff increases are announced, the Federal Reserve may pause interest rate cuts. Stricter immigration flows may bring additional upward risks to inflation.

The performance of silver prices is also worth looking forward to. Driven by industrial demand such as photovoltaic panels, silver prices are expected to rise from $30 per ounce to $40 per ounce.

Bank of America pointed out that copper and aluminum are the core beneficiaries of the new energy transition. Especially under the demand driven by electric vehicles, cecep solar energy, and grid upgrades, these two metals may see a price rebound by 2025. Although copper may face pressure in the first half of the year due to weak demand, prices are expected to recover from $8,500 per ton to $10,500 per ton as the global economy warms in the second half of the year. By 2025, the aluminum market is expected to enter a supply deficit phase, and prices may exceed $3,000 per ton.

Agricultural products market: A mix of weather and policy risks.

The agriculture market may be one of the most unstable areas in the csi commodity equity index. The report indicates that corn, chicago srw wheat, and soybean prices face downward pressure in the short term due to weather factors and weak demand. In addition, if the usa resumes the trade war with china, it could have a significant negative impact on the price of us soybeans. In contrast, sugar may have some room for price increases due to potential supply shortages.