具体来说,Michael Hartnett在报告中指出,由于美元和股市的大幅上涨,2025年第一季度将呈现长期的“美国繁荣”和短期的“全球萧条”。在这一背景下,美国小盘股(

具体来说,Michael Hartnett在报告中指出,由于美元和股市的大幅上涨,2025年第一季度将呈现长期的“美国繁荣”和短期的“全球萧条”。在这一背景下,美国小盘股(Bank of America analysts in the USA suggest that investors planning to engage in contrarian investments in 2025 should adopt an aggressive strategy, focusing on investing in bonds, international stocks, and gold.

Fintech APP learned that Bank of America analysts suggest that investors planning to engage in contrarian investments in 2025 should adopt an aggressive strategy, focusing on investing in bonds, international stocks, and gold. Bank of America Securities Chief Investment Officer Michael Hartnett's 2025 investment outlook report reveals that the global market will continue to be influenced by "major policies, major actions, and major tail risks," with a possible further differentiation in the global economy. The US economy is expected to exhibit "inflationary prosperity," while other regions face the risk of "deflationary recession."

Figure 1

Specifically, Michael Hartnett points out in the report that due to the significant rise in the US dollar and stock market, the first quarter of 2025 will see a prolonged phase of "US prosperity" and a short-term "global slump." Against this backdrop, US small-cap sE-mini Russell 2000 Index tocks, benefiting from the inflation combination policy of US tariffs, immigration control, deregulation, and tax cuts, are considered the best trades with excessive gains. However, Europe, Asia, and emerging markets show significant economic weakness at the beginning of 2025, especially in the manufacturing sector, with these regions facing greater risks of deflationary recession.

Specifically, Michael Hartnett points out in the report that due to the significant rise in the US dollar and stock market, the first quarter of 2025 will see a prolonged phase of "US prosperity" and a short-term "global slump." Against this backdrop, US small-cap sE-mini Russell 2000 Index tocks, benefiting from the inflation combination policy of US tariffs, immigration control, deregulation, and tax cuts, are considered the best trades with excessive gains. However, Europe, Asia, and emerging markets show significant economic weakness at the beginning of 2025, especially in the manufacturing sector, with these regions facing greater risks of deflationary recession.

Entering the second quarter, with European and Asian policy fear and a significant relaxation of the financial environment, international stocks will present a good buying opportunity. Bank of America predicts that the Federal Reserve will adopt a hawkish stance, while Europe and Asia will experience a peak of policy fear. At this point, "American exceptionalism" will peak, leading to significant adjustments in the US stock market, and asset allocation will shift towards cheaper international stocks and currencies. Attracted by China's fiscal easing, new European fiscal easing, and the European Central Bank's aggressive interest rate cuts, funds will flow towards European cyclical stocks and emerging market currencies.

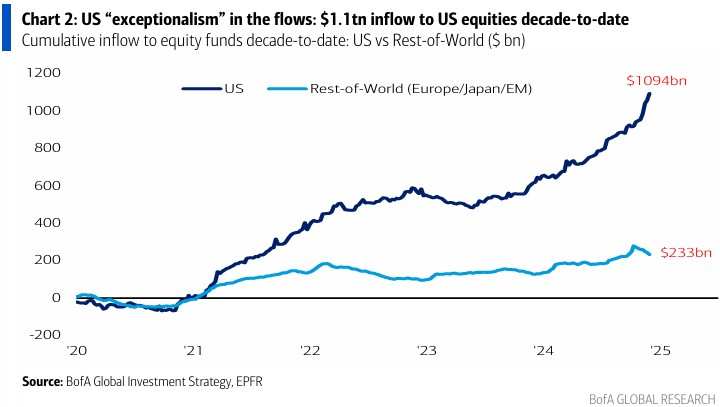

Figure 2

In addition, Bank of America also pointed out that when the US bond yield reaches 5%, investors should seize the opportunity to buy 10-year US Treasury bonds. This level may not only trigger market volatility and risk asset losses, but also mark the peak of "inflation prosperity," and may bring innovative solutions to reduce the US budget deficit. However, Bank of America also reminds investors that by the end of 2025, the US bond yield is more likely to be lower than 4% rather than higher than 5%, which will drive global stock markets to achieve a 5-10% increase by the end of the year, after the volatility in the first half of the year.

In terms of inflation, Bank of America expects inflation to unexpectedly rise, making gold and csi commodity equity index viable sources of income. Especially in the context of higher-than-expected inflation, copper, raw materials, and other csi commodity equity index are attracting attention. Fiscal overexpansion, economic isolationist trends, and the development of artificial intelligence are expected to continue to suppress any deflationary factors in 2025. If the Trump administration allows a second round of inflation to occur, it will be seen as a political dereliction of duty, as economic prosperity often comes with rising inflation, and the US was already at full employment status in early 2025.

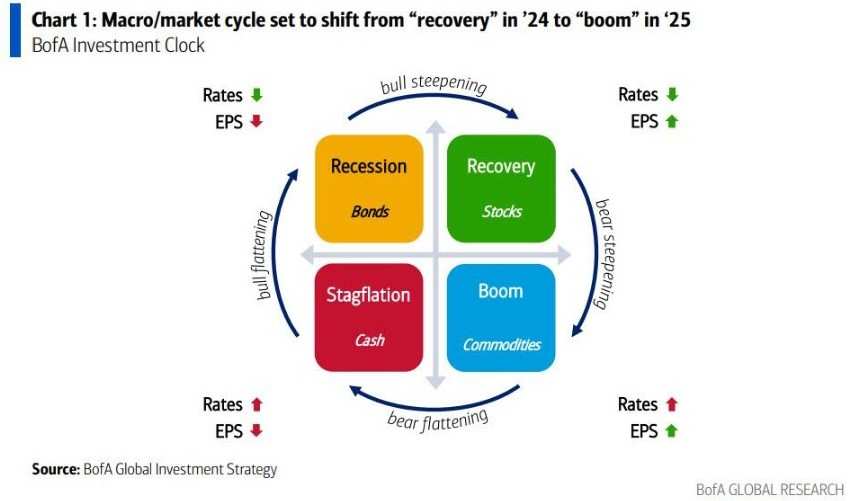

Bank of America's CNI Investment Clock Index model shows that the "recovery" phase of the stock market in 2024 (characterized by falling interest rates and rising earnings per share) is expected to be replaced by the "prosperity" phase of commodities (characterized by rising earnings per share and interest rates) in 2025. The prelude to this shift will be the "steepening of the bear market" in the first quarter of the yield curve, at which point bonds will begin to reflect expectations of "inflation prosperity" rather than "interest rate cuts."

Furthermore, Bank of America believes that higher-than-expected inflation will drive strong performances in gold (recommended to buy below $2500 per ounce), cryptos, and some underrated categories of csi commodity equity index assets in 2025. Especially when "policy panic" in Asia and Europe emerges, investors should prioritize layouts through copper, raw materials, Latin American assets, and commodities.

At the same time, Bank of America also advises investors to hedge against unexpected "tail risks." These tail risks include the end of the Hong Kong linked exchange rate system, the possible disintegration of the euro or a shift in EU strategy triggered by the "America First" policy, a sharp economic downturn in the US caused by Trump's tariff policy, a second round of inflation forcing the Federal Reserve to urgently raise interest rates, a depreciation of the US dollar caused by the incoming new Fed Chair in 2026 adopting a pro-inflation policy, and a potential Wall Street bubble in the field of artificial intelligence, among others.

Bank of America specifically points out that the AI/Seven Giant Bubble is currently the most significant "tail risk," because many investors anticipate that up to $7 trillion in money market funds will eventually flow into the US stock market (if the tighter financial conditions in the first quarter fail to curb investors' speculative enthusiasm, the market may re-enact the frenzy of 1999). In this bubble of the seven major tech giants, Bank of America believes that going long on cryptos and undervalued, tech-driven Chinese stocks is a wise choice to address this risk.

See Figure 3