特朗普的胜利给制药商带来了损失。自大选前一天以来,诺和诺德、罗氏、

特朗普的胜利给制药商带来了损失。自大选前一天以来,诺和诺德、罗氏、Source: Zhitong Finance

"Since 1950, the S&P 500 index has risen more than 10% 21 times as of the end of May. In about 90% of these cases, the S&P 500 index rose for the rest of the year. There were only two instances of declines for the rest of the year, in 1987 (-13%) and 1986 (-0.1%)."

With the rebound of the stock market, the old adage "Sell in May and Go Away" seems to have been a bad advice once again. Last month, the S&P 500 index rose 4.8%, the best May performance since 2009. The NASDAQ 100 index rose nearly 6.2%, and the NASDAQ Composite Index rose 6.9%. Goldman Sachs FICC & Equities Trading Division said: "History doesn't really support this saying. Don't sell, leave the market (go on vacation), and enjoy the good times."

The rising trend is still to be continued?

If history is any guide, it may indicate that the rise of the stock market is not over yet.

Looking ahead to the rest of 2024, Scott Rubner, Managing Director of the Goldman Sachs Global Markets Division and tactical expert, pointed out the following historical background for investors.

Rubner stated that the S&P 500 index has risen 10.7% year-to-date, and since 1950, the S&P 500 index has risen more than 10% 21 times as of the end of May. In about 90% of these cases, the S&P 500 index rose for the rest of the year. There were only two instances of declines for the rest of the year, in 1987 (-13%) and 1986 (-0.1%).

"Since 1950, the median return of the last 7 months of each year (June 1 to December 31) is 5.4%. In the aforementioned 21 cases, the average performance of the last 7 months increased to 8.1%." Rubner added.

Rubner also pointed out that the NASDAQ index has risen for 16 consecutive Julys, with an average return of about 4.64%.

Author: Wei Haoming

The growth prescription for pharmaceutical companies in Europe: shift to the USA.

Currently, the biggest threat faced by European pharmaceutical groups comes from the USA. The elected president Donald Trump and his nominated health secretary, Robert F. Kennedy Jr (RFK), are a "toxic combination" of "America First" nationalism and anti-pharmaceutical sentiment, which is even worse considering companies valued at $480 billion.$Novo-Nordisk A/S (NVO.US)$and $230 billion. $ROCHE HOLDING AG (RHHBY.US)$ From the perspective of companies like this.

Trump's victory casts a shadow over the prospects of European pharmaceutical companies.

Trump's victory has caused losses for drug manufacturers. Since the day before the election, novo-nordisk a/s, Roche,$Novartis AG (NVS.US)$、$AstraZeneca (AZN.US)$、$GlaxoSmithKline (GSK.US)$and $Sanofi (SNY.US)$ The total market cap loss of these six major europe companies reached 86 billion USD, equivalent to 6% of their equity value, while the total decline of major usa pharmaceutical groups was only 2%. The industry's common fear is related to Kennedy, who distrusts pharmaceutical companies, especially vaccines. Informants from european drug manufacturers told the media that they are concerned about his lack of public health awareness and general anti-science stance. Usa drug manufacturers should feel the same way.

However, investors in sanofi, Roche, and their regional peers are troubled by the fact that RFK and Trump's agenda may have an anti-Europe tendency. In September of this year, the cabinet nominee stated that legislators should restrict drug prices, so that pharmaceutical groups would not charge American patients more than those across the Atlantic. He wrote in a commentary that this difference relates to the fact that health authorities in European countries tend to negotiate with manufacturers on behalf of the entire nation, which allows them to maintain low prices. This will not happen in the USA. RFK cited novo-nordisk's diabetes and weight-loss drug Ozempic as an example, pointing out that its price in Germany is one-tenth of the current level in the USA. This is a sensitive area for Europeans, as the high drug prices across the Atlantic often subsidize drug research and support cheap sales to other regions of the world.

However, investors in sanofi, Roche, and their regional peers are troubled by the fact that RFK and Trump's agenda may have an anti-Europe tendency. In September of this year, the cabinet nominee stated that legislators should restrict drug prices, so that pharmaceutical groups would not charge American patients more than those across the Atlantic. He wrote in a commentary that this difference relates to the fact that health authorities in European countries tend to negotiate with manufacturers on behalf of the entire nation, which allows them to maintain low prices. This will not happen in the USA. RFK cited novo-nordisk's diabetes and weight-loss drug Ozempic as an example, pointing out that its price in Germany is one-tenth of the current level in the USA. This is a sensitive area for Europeans, as the high drug prices across the Atlantic often subsidize drug research and support cheap sales to other regions of the world.

Meanwhile, the universal import tariffs that Trump may impose could hurt pharmaceutical groups and severely undermine their competitiveness and profitability in the USA. In 2023, the EU exported 33% of its pharmaceuticals to the USA, which is usually one of the highest profit markets in the world. Unless drug manufacturers can pass on the costs of the proposed 10% to 20% tariffs, their profits will be hit.

Solution: "Localization in the USA."

Ironically, the antidote to all these problems in usa lies in the root: european drug manufacturers need to be more americanized. One option is to promote manufacturing in usa to avoid tariffs. This is difficult to accomplish in a short time, but making substantial commitments and starting operations at a new site may win the support of the Trump administration. Mergers and acquisitions trade would also help. Novo-nordisk a/s's parent company announced in February this year that it will spend 16.5 billion USD to acquire a contract drug manufacturers. $Catalent (CTLT.US)$ The target company's website lists more sites in North America than in other regions, which means this Danish giant is buying itself a convenient tariff hedging tool. The only problem with this strategy is that mergers and acquisitions in usa are not cheap, just like the usa labor force. At that time, the media estimated that the roi of Novo-nordisk a/s's parent company would be less than 3%.

Another strategy might be for european pharmaceutical groups to fundamentally change their revenue structure through mergers and acquisitions, rather than merely expanding their production scale. For instance, acquiring a fast-growing biotechnology group focused on the usa from among many would be beneficial. This may sound strange because RFK's plan could undermine growth in that market. However, this idea would initiate a transformation from european pharmaceutical manufacturers to usa pharmaceutical manufacturers—relocating top executives to new york and eventually listing there would be the logical next step. If the world's largest and most profitable drug market becomes increasingly nationalistic, it makes sense for european giants to enter the local market.

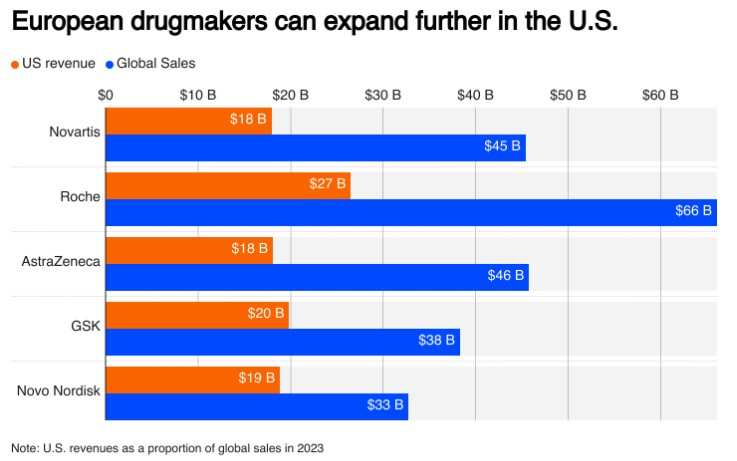

Many companies facing risks also have their own special reasons for leaning towards the usa market. For instance, novartis ag is at the top of the european market, making further growth in its home region challenging.

Despite concerns about RFK's policies, the stock prices of USA drug manufacturers often remain higher than those of their most direct competitors in europe, indicating that investors believe growth in the USA market will continue. For example, in the hot obesity market, according to Visible Alpha, $Eli Lilly and Co (LLY.US)$ the PE ratio is 34 times, while the PE ratio of Denmark's novo-nordisk a/s is 27 times. Similarly, the expected PE ratios for the european drug manufacturers astrazeneca and novartis ag are 14 times and 13 times, respectively, while the expected PE ratio for Illinois-based abbvie (ABBV.US) is 15 times.

It remains unclear what measures trump will take regarding tariffs or drug prices, and the implications for the rest of the world are even more uncertain. However, investors seem convinced that the performance of european pharmaceutical groups will be the worst, making it all the more reason for them to turn towards the usa market.

Editor/Jeffy