贝莱德表示,此轮上涨的背后,是市场对美国经济增长更加强劲、以及对监管环境(尤其是金融监管)更加宽松的预期。如今,美国大选结果已揭晓,市场反应也已初步平息。

贝莱德表示,此轮上涨的背后,是市场对美国经济增长更加强劲、以及对监管环境(尤其是金融监管)更加宽松的预期。如今,美国大选结果已揭晓,市场反应也已初步平息。Source: Zhitong Finance and Economics.

Blackrock stated that in terms of stocks, it is recommended to moderately overweight US stocks before the end of the year, focusing on finance, consumer discretionary, and specific technology sectors. At the same time, Blackrock will reduce holdings in 'defensive' sectors (especially essential consumer goods) to provide funds for moderately overweighting stock assets. Regarding bonds, opportunities still exist in corporate bonds, securitization, and other forms of credit products, but investors should remain cautious about long-term US bonds. Due to the bond market's difficulty in digesting a large supply of bonds, long-term US bonds may face greater challenges in the coming months or even years.

With the US election dust settled, investors have shed their wait-and-see attitude and are now rushing to embrace US stocks and other risky assets. Last week, the S&P 500 index rose by 4.7%, achieving its best weekly performance since October 2022. This week, the Federal Reserve released the minutes of its November monetary policy meeting, driving the market's optimistic sentiment and leading to another increase in the S&P 500 index by the day's closing.

Blackrock stated that behind this round of gains is the market's stronger expectations for US economic growth and a more lenient regulatory environment (especially financial regulation). Now that the results of the US election have been announced, market reactions have also begun to calm down.

Blackrock stated that behind this round of gains is the market's stronger expectations for US economic growth and a more lenient regulatory environment (especially financial regulation). Now that the results of the US election have been announced, market reactions have also begun to calm down.

As the end of the year approaches, how should investors view the trends in the US stock market before the year-end? Blackrock believes that the following three points are worth noting: the continued strength of US stocks, cyclical stocks leading the way, and a further steepening of the yield curve.

Despite the cumulative 25% rise in US stocks since the beginning of the year (as of November 20), which shows a significant premium compared to other markets and historical levels, Blackrock believes that this upward trend may still continue in the short term. In addition to growth in the consumer market and loose monetary policy, US stocks may also benefit from seasonal strength, as well as optimistic expectations from the market for more fiscal stimulus policies and relaxed regulatory measures.

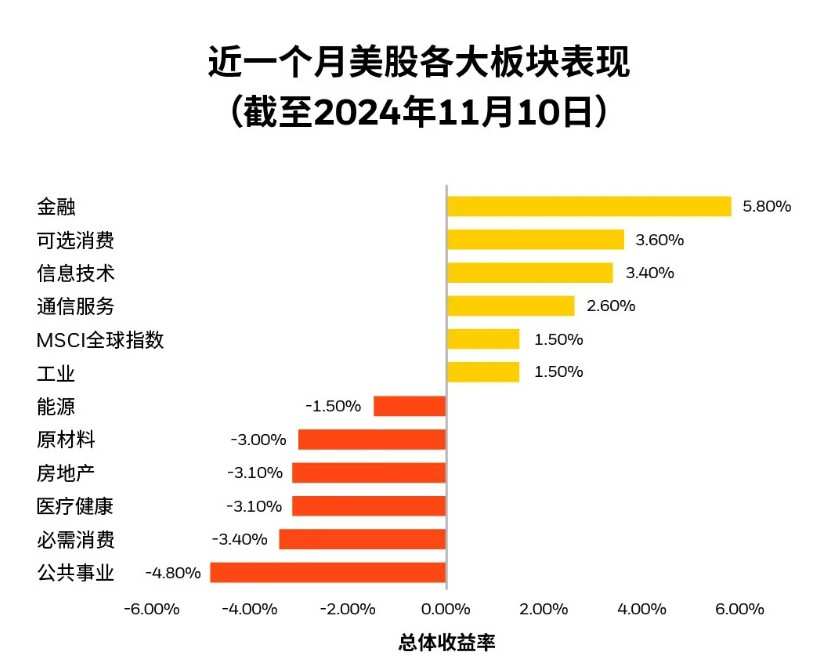

In terms of individual stocks, Blackrock predicts that cyclical stocks are likely to continue to maintain their lead, consistent with trends seen over the past few months. Blackrock believes that the pace of US economic growth may not be too significant, currently maintaining a healthy level between 2.5% and 3%. However, investors may continue to favor companies or sub-sectors with operational leverage (the ability to increase revenue by increasing income), including the consumer discretionary and financial sectors (as shown in the figure) that have led the way since the election. The financial sector is not only benefiting from robust US economic growth and a steep yield curve, but may also see a more lenient regulatory environment under a Republican administration, further boosting its performance.

BlackRock mentioned that, in addition to the stock market, the market environment for bonds and interest rates may also be affected, especially long-term US Treasury bonds. The main reasons are that, against the backdrop of a strong US economy, further stimulus measures may alter the pace and extent of future interest rate cuts by the Federal Reserve; secondly, in addition to monetary policy, tax cuts and/or stimulus measures funded through debt financing may further exacerbate the already historically high fiscal deficits in the USA, thereby increasing the issuance of US Treasury bonds.

It is worth noting that although the yields on US Treasuries have rebounded from the lows in September, the additional yield compensation received by investors for bearing long-term risks (i.e., term premiums) is still at a moderate level compared to historical levels. If bond investors begin to anticipate larger multi-year fiscal deficits, the yields on long-term bonds may further accelerate, surpassing short-term bonds, thereby forming a steeper yield curve.

Editor / jayden