VerityData数据显示,美股上市公司内部人士出售股票交易率长二十年来单季最高纪录。这里所指的出售交易是指,在涵盖美国活跃交易美股的市值加权指数、美国上市公司覆盖面最广的指数之一Wilshire 5000中,成分股公司的高管出售股票,包括一次性获利回吐的交易,以及价格达到高管自动交易计划设定水平后所触发的定期出售交易。

VerityData数据显示,美股上市公司内部人士出售股票交易率长二十年来单季最高纪录。这里所指的出售交易是指,在涵盖美国活跃交易美股的市值加权指数、美国上市公司覆盖面最广的指数之一Wilshire 5000中,成分股公司的高管出售股票,包括一次性获利回吐的交易,以及价格达到高管自动交易计划设定水平后所触发的定期出售交易。Many reasons for insiders selling stocks have nothing to do with the prospects of the listed companies themselves. However, considering the recent returns, high valuations, increasing leverage, and the generally highly speculative environment, insider selling may suggest that the performance of the US stocks next year will be below expectations.

Recently, the trend of insiders selling company stocks from US-listed companies has been so strong that it has raised concerns in the media.

A recent report from the Financial Times stated that a record number of American corporate executives are selling their company's stocks. From Goldman Sachs to Tesla, and even Trump's own media group, a large number of corporate executives are taking advantage of the US stock market's rise after Trump’s election to profit.

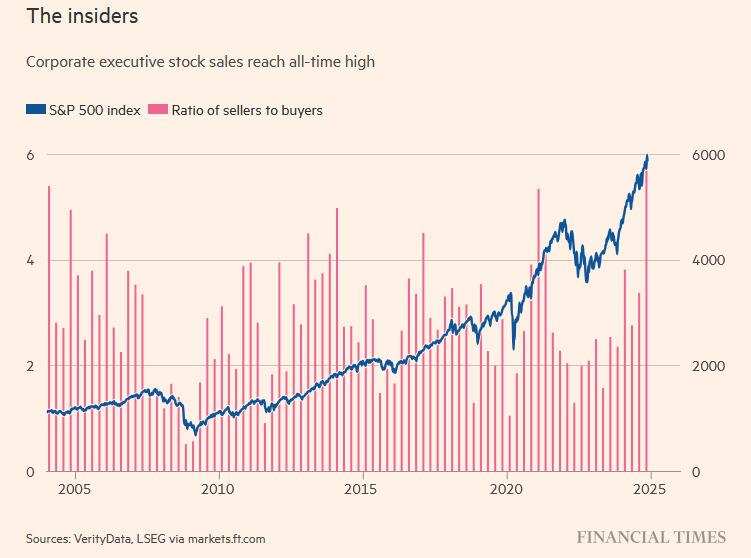

VerityData shows that the rate of stock sales by insiders of US-listed companies has reached a record high for a single quarter in twenty years. The sales transactions referred to here involve executives from constituent companies of the major US stock indices, including the market capitalization-weighted index that covers active trading stocks in the USA and one of the broadest indices of US-listed companies, the Wilshire 5000. This includes transactions for one-time profit-taking and regular sales triggered after prices reach levels set by executives’ automatic trading plans.

VerityData shows that the rate of stock sales by insiders of US-listed companies has reached a record high for a single quarter in twenty years. The sales transactions referred to here involve executives from constituent companies of the major US stock indices, including the market capitalization-weighted index that covers active trading stocks in the USA and one of the broadest indices of US-listed companies, the Wilshire 5000. This includes transactions for one-time profit-taking and regular sales triggered after prices reach levels set by executives’ automatic trading plans.

Moreover, in the fourth quarter of this year, the ratio of insider sellers to buyers among S&P 500 constituent companies was 23.7:1, which is the highest level since the US first mandated disclosure of insider trading data in 2004.

There are various reasons for insiders selling stocks, many of which are unrelated to the company's own prospects. Therefore, the record insiders’ sell-off does not necessarily signal a terrifying alarm. However, considering the recent returns, high valuations, increasing use of leverage, and an overall highly speculative environment, the insider sell-off sends another warning for the US stock market as a whole, suggesting that the market performance next year may not meet expectations.

Regarding the relationship between insider trading and market performance, Ben Silverman, the research director at VerityData, commented, "Generally speaking, insider sales tend to precede predictions by about two to three quarters. When they start to see bubbles forming in the market, insiders become more proactive in trying to generate liquidity."

However, Goldman Sachs' recent outlook for global investments in 2025 predicts a good return for US stocks next year.

Goldman Sachs calls next year the "Year of Alpha," suggesting investors focus on diversification to improve risk-adjusted returns, believing that high concentration and high valuations are reasons to reduce the weight of usa stocks in multi-asset portfolios, paying attention to assets such as stocks in japan and other asia, short-term government bonds, and the dollar, while gold remains the best hedging tool.

Goldman Sachs expects that global economic growth will remain stable next year, inflation will decline further, and monetary policy will continue to be accommodative. However, with the easing of inflationary tailwinds, the valuation of risk assets is at a high level, and the increase in policy uncertainty after the usa elections, along with geopolitical risks and the shift to "re-inflation," leads to increased tail risk.

Goldman Sachs suggests that investors maintain a moderate overweight in usa and asia, especially in the stock market of japan, while holding a neutral stance in the stock market of europe. Goldman Sachs believes that although valuations are high, strong earnings growth and healthy corporate balance sheets will continue to drive shareholder returns, especially in the usa market.

Goldman Sachs predicts that global equity will have a price return of 9% and a total return of 11% in the next year, primarily driven by earnings growth rather than valuation expansion. The roi for the s&p 500 index next year is projected at 11%. Due to weak economic activity, tariffs, constrained profit margins, and fluctuations in the range of csi commodity equity index prices, the roi for the europe STOXX 600 index is only forecasted to be 3% next year.

Editor/ping