In recent years, the capital markets have become more cautious.

The market has raised higher demands for the profitability and long-term development of enterprises. Against this backdrop, whether enterprises can completely rely on their own strength to survive and even achieve profitability without external funding has become a key issue facing their development.

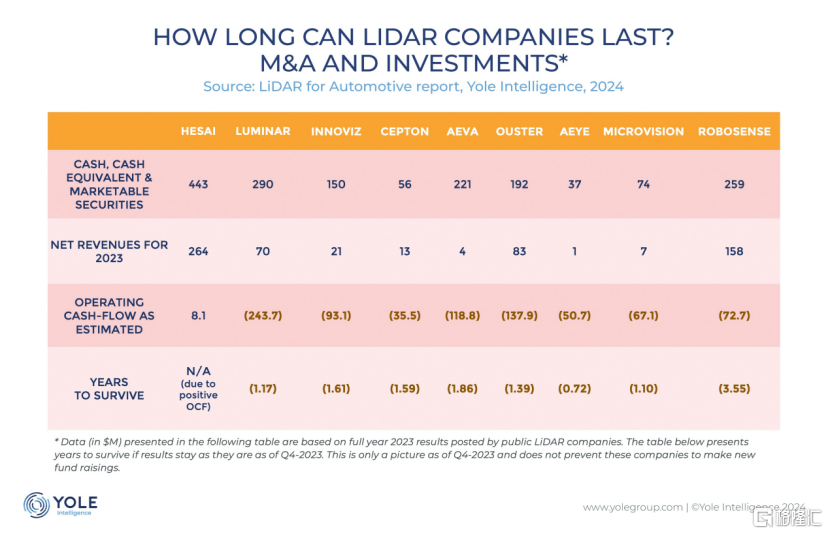

Taking the global smart automobile industry chain as an example, although many star companies have emerged, only a few have achieved profitability. Particularly in the field of onboard lidar, Yole Intelligence, in its "2024 Global Automotive Lidar Market Report," pointed out that many companies are facing rapid cash consumption and negative gross margins. Yole Intelligence further predicts that the cash flow of most overseas companies will be exhausted within two years.

But at the same time, there is still hope. The lidar industry may soon see its first profitable company.

But at the same time, there is still hope. The lidar industry may soon see its first profitable company.

On November 26, leading onboard lidar manufacturer Hesai (HSAI.US) announced its performance for the third quarter of 2024, significantly exceeding market expectations, and the company is on track for annual profitability. In the first trading day following the earnings report, Hesai's stock skyrocketed by 44%, indirectly confirming the capital market's high recognition of the financial report.

1. Approaching the Profitability Inflection Point

In the third quarter of 2024, Hesai achieved revenue of 0.54 billion yuan, a year-on-year increase of 21.1%. This growth was mainly due to a significant increase in lidar shipments, with total quarterly deliveries reaching 134,208 units, a substantial year-on-year growth of 182.9%; it is expected that in the fourth quarter, lidar shipments will reach nearly 0.2 million units, close to the company's total shipments for 2023.

In terms of profitability, Hesai continues to significantly turn losses into gains, with a Non-GAAP net loss narrowing by 56.8% year-on-year, and profitability indicators continuing to improve. It is also worth mentioning that the company’s ability to generate cash has been continuously improving. According to Yole Intelligence's "2024 Global Automotive Lidar Market Report," Hesai's cash flow situation stands out in the industry, being the only lidar company to achieve positive operating cash flow in 2023. As of the latest financial report, the company’s cash and cash equivalents, restricted cash, and short-term investments exceed 2.5 billion yuan, making it one of the few lidar leaders without cash flow anxiety.

With the current development momentum, hesai is expected to reach the milestone of being the "first in the world" in the fourth quarter — including becoming the world's first automotive lidar company to achieve quarterly profitability (GAAP) of over 20 million dollars, and the first company globally to achieve annual profitability (Non-GAAP).

Why has hesai been able to approach the profitability turning point ahead of its peers?

By breaking down the profit statement model, we can find the answer — hesai maintained a high gross margin and achieved continuous growth in gross profit, while controlling the expense ratio (including R&D and SG&A). Generally, gross margin usually reflects a company's product or service market competitiveness, as well as its control over the supply chain. In the first half of 2024, hesai's gross margin reached 45%, a figure that significantly exceeds that of its industry competitors — during the same period, valeo and suptech's gross margins were only 18.5% and 13.6%, respectively. Even looking at the entire automotive industry chain, hesai technology's gross margin is particularly notable. For a long time, the average sales gross margin of the new energy vehicle industry sector has been below 20%. For example, the leading company in the power battery industry, contemporary amperex technology, had a gross margin of only 26.5% for the same period; and ningbo joyson electronic corp., a leading enterprise in the automotive safety components field, had a gross margin of 15.6%. In the traditional automotive industry chain, even the leading automotive glass manufacturer fuyao glass, which is considered to have a high gross margin level, still could not break through 40% in gross margin for the first half of 2024, still showing a noticeable gap compared to hesai technology. These data fully demonstrate hesai technology's competitive advantage and profitability in the industry.

In the third quarter, thanks to the positive cycle of cost and scale, along with the boost from service revenue, hesai's gross margin further increased to 47.7%.

In addition, hesai has found a balance between controlling short-term costs and achieving long-term growth. Technology can only succeed with a firm long-term investment approach. Reducing R&D investment to gain profit margins is undoubtedly a short-sighted move. The company did not choose to reduce R&D investment for short-term profits but insisted on long-term investment to enhance product competitiveness and innovation capabilities. In the third quarter, the company's R&D expenses grew by 14.3% year-on-year, reaching 0.22 billion yuan. At the same time, through technological commercialization and rapid revenue growth, the company successfully reduced the expense ratio without sacrificing R&D and long-term growth. The gross margin and expense ratio will gradually form a scissor effect, creating conditions for the company’s net income rate to turn positive.

It can be said that this is a long-term positively growing financial model.

Second, it is the "hitting point" for investors and the "growth acceleration point" for enterprises.

The profit inflection point is a key turning point in the development of a company.

The development trajectory of technology companies often follows an S-curve model, which describes the complete life cycle of a product from market introduction to eventual decline. During the introduction phase, new technologies or products experience slow growth due to low market awareness and limited consumer acceptance. In the growth phase, as market awareness of the new technology or product increases, along with improvements and maturation of the product itself, market demand rapidly increases, and the growth rate accelerates.

Within the S-curve, there is a critical point known as the profit inflection point, which is an important sign of a company entering a rapid growth stage. Once this point is crossed, the company's profitability and revenue growth will exhibit exponential growth, rather than just nonlinear growth. This becomes the 'hitting point' that investors are most concerned about—this also explains why Hesai's stock price surged over 40% after its earnings report. Furthermore, the profit inflection point also signifies a growth inflection point, usually accompanied by a rapid increase in market penetration rates, as well as a swift expansion in sales and market share, representing a critical juncture for the validation of the business model.

In publicly available information, we can find empirical support for this point:

First, Hesai's leadership position in the global vehicle lidar market continues to strengthen. The company has ranked first for three consecutive years in terms of global market share for vehicle lidar, passenger vehicle lidar market share, and installations. According to data from NE Times, in September 2024, Hesai maintained its position as the highest company in China in terms of lidar assembly volume with a market share of 31.9%.

Second, Hesai's product market penetration rate is also rapidly increasing. As of the third quarter of 2024, the company has established production partnerships with 75 models from 20 domestic and international auto manufacturers, including well-known companies such as Li Auto, Xiaomi, Leapmotor, Great Wall Motor, Chongqing Changan Automobile, and SAIC Volkswagen. Six out of the ten highest-revenue international auto manufacturers in the Fortune Global 500 list have already reached mass production partnerships with Hesai.

Data source: 2024 Global Vehicle Lidar Market Report published by Yole Intelligence, a subsidiary of the international authoritative research institution Yole Group.

Hesai co-founder and CEO Li Yifan stated that in the third quarter, the company's business maintained a strong growth momentum, gaining multiple new customers and projects. This quarter, Hesai established partnerships with a top three automobile company in japan, SAIC Volkswagen, leapmotor, and a high-end electric vehicle brand under a leading automobile group in china. In addition, a cooperative project with a global mass-production model of an international top automobile brand has successfully entered a new stage, marking a key milestone in Hesai's international expansion.

After years of deep cultivation, the company's future growth path is becoming increasingly clear, and it is about to enter a harvest season.

It has been proven that there are no windfalls in the technology industry, only perseverance.

Technology investments should look to the long term.