中海油2022年到2024年年中的一波主升浪,吸引了众多投资者的目光。随着股价的持续调整,市场对于中海油虽然评价依旧较高,但从股价的行动上看可能更像是,“这股票不错,我卖给你吧。”

中海油2022年到2024年年中的一波主升浪,吸引了众多投资者的目光。随着股价的持续调整,市场对于中海油虽然评价依旧较高,但从股价的行动上看可能更像是,“这股票不错,我卖给你吧。”

Source: Yaya Hong Kong Stock Circle Author: Kyle In the first half of this year, statistics show that at least 180 Hong Kong stock companies have implemented share buybacks, with a total amount of HKD 121 billion, setting a new high in the same period of history. Especially in the Internet companies, almost every shareholder return program has been significantly improved, which can be said to have opened a new era of Internet shareholder returns. Among these companies, Tencent, the "North Star" of Hong Kong stocks, is undoubtedly the most prominent. In the first half of this year, it contributed more than 40% of the repurchase volume of the Hong Kong stock market, firmly occupying the seat of the "repurchase king" of the Hong Kong stock market. In the second quarter, Tencent's single-quarter repurchase amount reached HKD 37.5 billion, which doubled from the first quarter's HKD 14.8 billion. The repurchase average price increased from HKD 290.6 to HKD 361.8, an increase of nearly 25%. It is worth mentioning that Tencent's repurchase amount this year will exceed HKD 100 billion, doubling from last year's HKD 49 billion. What is the concept of a one trillion repurchase plan? This amount is the sum of Tencent's total repurchase amount in the past ten years, which proves the management's confidence in future development and attaches importance to the demands of investors. Through various means such as repurchase cancellation, dividends, and physical distribution, Tencent has truly given back to shareholders in the capital market while achieving performance growth. One, the significance of a trillion repurchases is actively emerging. Looking back at the past two years, since Tencent's major shareholder Prosus began to reduce its holdings, the stock price has been somewhat suppressed. In particular, there have been regular trading behaviors in the market when Hong Kong stocks perform poorly. For example, Hong Kong-listed companies have a "silent period for repurchase" in the month before the financial report is released, during which repurchase is not allowed. This caused great upward pressure on the stock price whenever Tencent entered the repurchase silent period before last year. As can be seen from the following data, of the five silent periods before the end of 2023, only Tencent's stock price in October-November 2022 rose, and in other times it fell. However, since the end of last year, Tencent's stock price has risen during two consecutive silent periods. Especially after the launch of the trillion-dollar repurchase plan this year, the repurchase volume has far exceeded the number of shares sold by major shareholders. Therefore, whether it is on normal trading days that can be repurchased, or during silent periods, the impact brought by the sale of major shareholders can be ignored, and this point is being formed by market consensus. For example, during the repurchase silent period from January to March this year, which happened to be the worst half-year Hong Kong stock market, the Hang Seng Index fell to 14,800 points. Tencent's performance during this period was significantly better than before. Even though the short selling ratio once reached 20%, the stock price did not fall, and the final interval increase was 6%. After the release of the better-than-expected 2023 annual report and the restart of the repurchase at the end of March, Tencent's stock price performed even better in the second quarter, with an increase of nearly 25%. During the same period, the Hang Seng Index and the Shanghai and Shenzhen Composite Indexes fell significantly, with gains of only 8% and 4%, respectively, while Tencent significantly outperformed the Hong Kong stock market with a gain of 25%. Behind this phenomenon, there is no doubt that the trillion-dollar repurchase plan, which has doubled from last year's amount, has played an important role. More importantly, after the repurchased shares are cancelled, Tencent's share capital has been declining for three consecutive years. Since 2021, Tencent's total share capital has decreased from 9.608 billion shares to 9.355 billion shares. In the first quarter of this year, Tencent issued ordinary shares decreased by 1.1% compared to the previous quarter, and the repurchased shares have also been gradually cancelled since this year. This trend will continue to increase earnings per share and further enhance shareholder value. (Caption) Starting in 2022, Tencent has increased its repurchase efforts. With the repurchase cancellation, the company's total share capital has gradually decreased.

Author: Chongfeng

$CNOOC (00883.HK)$ The stock price has peaked and has been declining for nearly half a year.

Cnooc's main upward wave from 2022 to mid-2024 has attracted the attention of many investors. Although the market still holds a high evaluation of Cnooc with the continuous adjustment of the stock price, based on the stock price's movement, it seems more like, "This stock is good, I'll sell it to you."

How should Cnooc be viewed currently?

How should Cnooc be viewed currently?

1. One of the largest oil companies with the lowest costs.

Cnooc is China's largest offshore crude oil and natural gas supplier, with assets spanning over 40 countries and regions worldwide. Its main business includes exploration, development, production, and sale of crude oil and natural gas. It holds 95% of the exploration and development rights of China's ocean resources and is the only enterprise authorized by the State Council to possess marine oil and gas extraction permits.

The company's main business is mainly divided into oil & gas sales, trading, and other businesses. Among them, oil & gas sales accounted for 78.7% of revenue in 2023, and the gross margin reached 97.23% of the company’s total, making it the main source of income and profit. Furthermore, within oil & gas, the revenue from petroleum sales typically accounts for over 80% of the total oil & gas sales revenue, reaching 86% in 2023. Therefore, petroleum is the core product affecting the company’s performance.

As a member of the three major oil companies, CNOOC inevitably has to be compared with the other two.

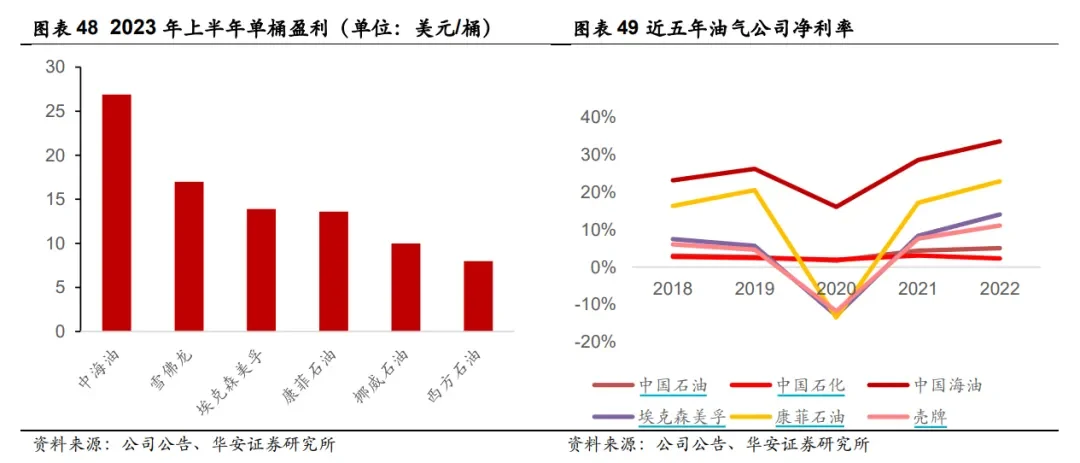

A comparison reveals that CNOOC's profitability is far higher than that of the two brothers.

CNOOC has a lower debt ratio, a higher profit margin, and a ROE level close to 20%.

Why is there such a large quality difference when all of them deal in petroleum?

1. Focus on upstream

Engaging in petroleum is definitely profitable; just look at those scarf-wearing rich folks in the Middle East, who are extraordinarily wealthy and freely procure in the A-share market.

However, there are different ways to engage in petroleum.

$PETROCHINA (00857.HK)$ and $SINOPEC CORP (00386.HK)$ Companies that are part of the entire industry chain layout, especially the investment in downstream gas station networks, generally cannot be managed by regular enterprises, so letting them manage can generate profits, but the profit level is lowered.

However $CNOOC (00883.HK)$ Mainly focused on offshore oil & gas exploration, development, production, and sales, it is the largest producer of offshore crude oil products and henry hub natural gas in the world. This focus on upstream business strategy enables cnooc to enjoy high gross margins in oil & gas exploration and extraction, avoiding the low margins in midstream and downstream sectors.

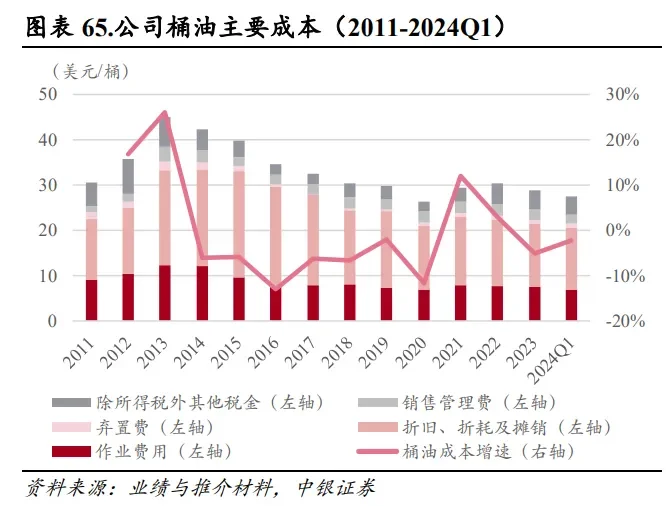

2. Low-cost strength

Low cost can be said to be the core competitive ability of oil companies, and it is key for the company to improve profitability and cope with the uncertainties of international oil price fluctuations.

CNOOC's oil production costs are generally on a downward trend and are at a leading level globally.

The main costs of CNOOC's oil barrel are composed of five parts: operating expenses, depreciation and amortization, abandonment costs, sales management expenses, and other taxes excluding income tax. In 2023, CNOOC's main costs for oil barrels were $28.83 per barrel, of which 49% were due to depreciation and amortization costs, and 26% came from operating expenses, accounting for 25.5% and 48.3% respectively.

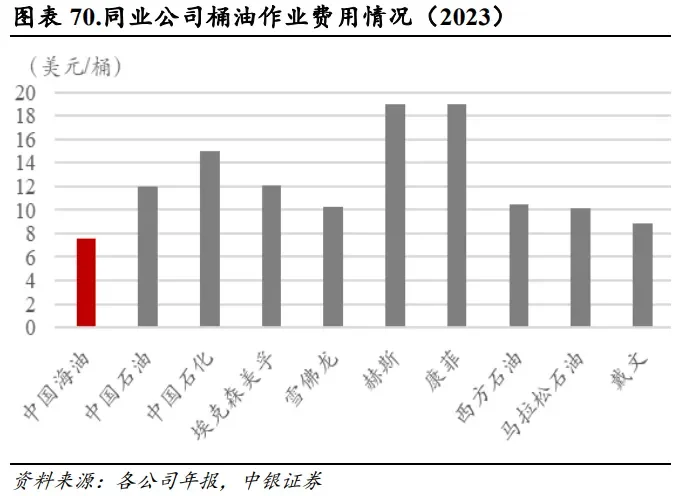

Among them, barrel oil operating expenses are globally leading, and the fluctuation with oil price changes is low. The depreciation and amortization costs of barrel oil are at the industry average level and are decreasing year by year, mainly because some high-cost assets from previous periods are being gradually absorbed.

At the same time, multiple technologies in the company's exploration, development, and production stages have achieved independent innovation, reaching globally leading levels or world advanced positions. Since 2023, the company has achieved several global firsts, including the world's first fully automatic production line for downhole electric machines, the world's first 100,000-ton deepwater semi-submersible oil storage platform, the world's first high-temperature, high-pressure multidimensional nuclear magnetic logging instrument, and the world's first high-temperature coring technology.

With a focus on upstream, low barrel oil production costs, internationally leading production technologies, and streamlined efficient personnel management, CNOOC's profitability is at a leading level in the industry.

In addition to its excellent qualifications, on the other hand, offshore oil and gas resource exploration is a major growth point for global oil and gas production. From a global perspective, due to the high exploration levels of onshore and shallow water oil, oil and gas production has nearly reached its peak. New oil and gas reserves worldwide have shifted from onshore and shallow waters to deep water, with nearly 50% of significant exploration discoveries in recent years coming from deep water, with proven reserves of about 100 billion tons of oil equivalent. The EIA predicts that the world's maximum recoverable oil is 300 billion tons, of which seabed oil reserves are 135 billion tons, accounting for 45%.

However, according to CNOOC's prospectus, as of 2020, the overall level of proven oil and gas resources in china is relatively low, with an average oil resource proven rate of 23%, far below the global average of 73% and the usa's 75% proven rate, while the average natural gas resource proven rate is 7%.

Cnooc is also actively acquiring resources globally, continuously engaging in overseas mergers and acquisitions, with assets spread across more than 20 countries and regions including the USA, Canada, Brazil, and Guyana, holding interests in several world-class oil & gas projects. As of the end of 2023, overseas oil & gas assets accounted for approximately 44.6% of the company's total oil & gas assets, with about 40.3% of its net proven reserves and approximately 31.2% of its net production coming from overseas.

The considerable space in the industry has also motivated Cnooc to continuously strive for progress, driving growth in reserves and production through sustained high capital expenditures. Since 2016, the company's capital expenditure has rapidly increased from 48.733 billion yuan to 127.913 billion yuan in 2023, with a compound annual growth rate of 14.8%. In 2024, the company adjusted its capital expenditure budget to 1250-135 billion yuan. Driven by measures to increase reserves and production, the company's oil & gas production has achieved continuous breakthroughs. In 2023, net oil & gas production reached approximately 678 million barrels of oil equivalent, exceeding the initially set annual target of 650-660 million barrels of oil equivalent, with a year-on-year growth of 8.7%.

At the same time as maintaining high capital expenditures, the company is also offering decent dividends to ensure shareholder returns, and it has committed that from 2022 to 2024, the annual dividend payout ratio is expected to be no less than 40%; the absolute annual dividend is expected to be no less than 0.70 HKD per share (before tax).

2. Positive correlation with oil prices.

Cnooc has maintained good quality; why is the market not interested?

The biggest factor is the decline in oil prices.

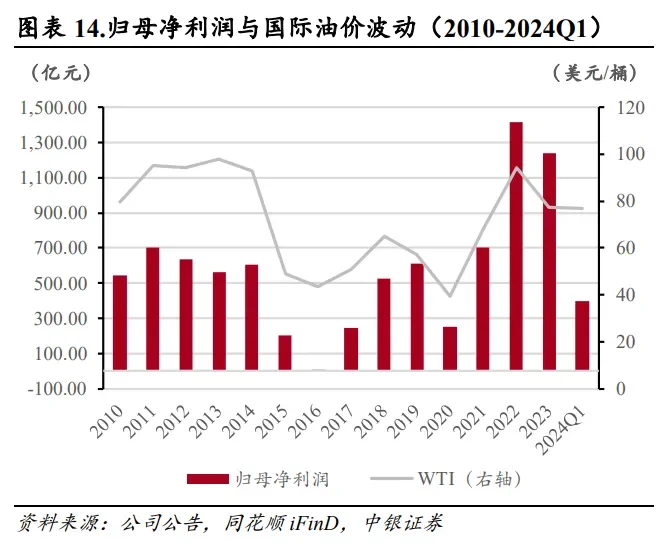

The company's profitability is greatly affected by oil prices; it can be seen that its net income has a correlation with the fluctuations in international oil prices.

At the same time, Cnooc's stock price has a long-term positive correlation with oil prices, only recently breaking out into an independent trend, with the market giving it a revaluation.

The main reason is that in 2022, under a high oil price market environment, the net income attributable to the parent company reached 141.7 billion yuan, a year-on-year increase of 101.51%. The huge profits combined with a good dividend rate and extremely low valuation led to its dividend yield exceeding 15% at one point. The defensive dividend rate pricing in the last two years provided cnooc with an opportunity for value reassessment. At the same time, despite the high fluctuations in oil prices, cnooc can still maintain decent profits to sustain its dividend level.

However, in the second half of this year, oil prices began to decline continuously, moving away from the high fluctuation range. The stock price of cnooc also started to fluctuate downwards.

When the market believes that cnooc is showing an independent trend, it is actually still heavily tied to oil prices after reassessment.

How should future oil prices be viewed?

Oil currently accounts for about 33% of the total energy consumption in the world. Its price is mainly influenced by supply and demand, crude oil inventory, and geopolitical risks.

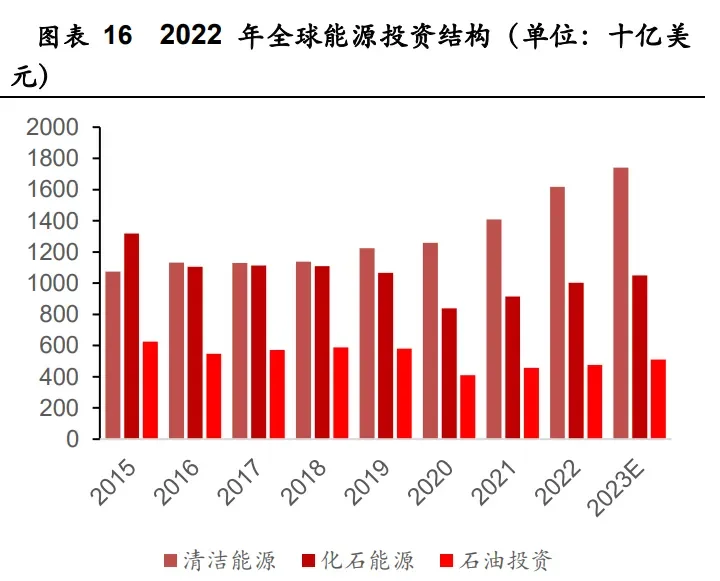

From a long-term perspective, the global green energy transition goals are still ongoing. Carbon peak is expected to be achieved by 2030, and carbon neutrality is targeted before 2060. The investment proportion related to oil continues to decline, while the proportion of investment in clean energy continues to rise. The long-term supply side is limited.

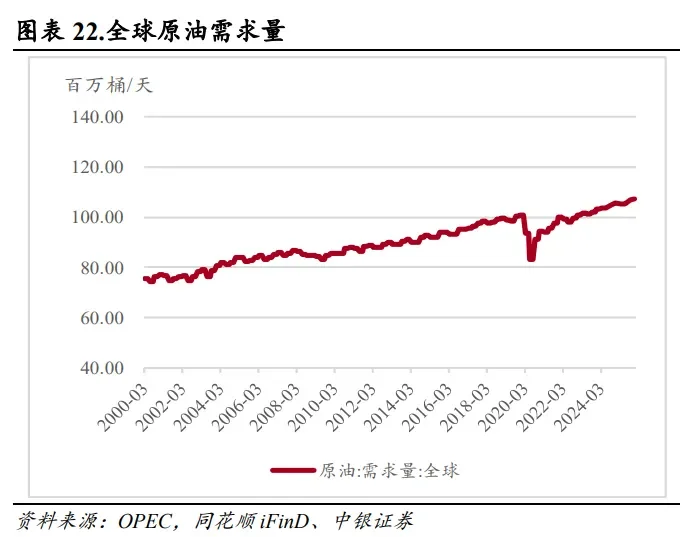

The global demand for crude oil has been slowly increasing in the long term. According to EIA statistics, the world’s oil consumption in 2023 is 101 million barrels per day, with the Asia-Pacific, North America, and Europe accounting for 36.85%, 24.27%, and 14.12% of global oil consumption, respectively. The Asia-Pacific is the largest region for oil consumption. China and india are the second and third largest oil consumers in the world, accounting for 15.78% and 5.26% of the world's total consumption, respectively.

According to the IEA’s report "Oil 2023: Analysis and Forecast to 2028" released in June 2023, it is expected that global oil demand will reach 0.106 billion barrels per day by 2028, an increase of 5.9 million barrels per day compared to the level in 2022. OPEC raised its forecast for oil demand in the "2023 World Oil Outlook" released on October 9, 2023, estimating that global oil demand will peak at about 0.116 billion barrels per day by 2045.

This means that long-term, the supply and demand situation for crude oil will gradually tighten.

But in the short to medium term, the situation is more complicated.

Currently, the combined oil production from the americas, OPEC, and Russia approaches 80% of the global oil supply.

To respond to weak global demand and the potential for economic recession impacting oil prices, OPEC+ will announce an extension of production cuts for another three months until April 2025, with Russia likely to follow suit.

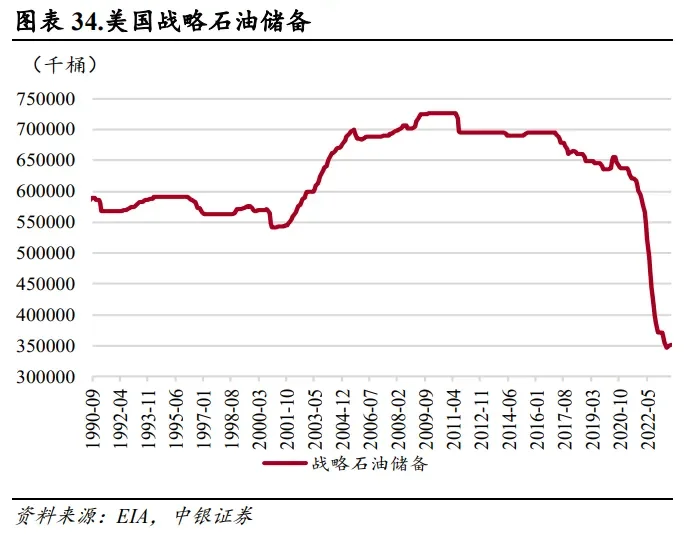

Meanwhile, the usa has been increasing production and selling oil reserves for two years to reduce inflation, which has brought prices down. In June 2023, the strategic petroleum reserve in the usa fell to its lowest level since 1990, with only 0.347 billion barrels remaining. After prices dropped, there was active replenishment in July 2023, likely nearing the end of 2025, but the trend in oil prices does not show significant support due to a slight slowdown in the global economy.

Since Trump took office, the strength of the dollar has also negatively impacted oil prices. Trump has clearly supported traditional oil companies in energy policy, potentially easing restrictions on them, while during his administration, the effect of new energy alternatives has slowed, providing better investment prospects for oil companies.

Thus, in the short to medium term, the return of strong oil prices is not very clear.

If oil prices can stabilize at a certain level, the profit expectations for cnooc will also stabilize. However, with current oil prices around 70 dollars, this is the breakeven point for many shale oil producers in the usa. Many institutions predict that oil prices will range approximately between 70-85 dollars.

If the global economy does not meet expectations, then oil prices may decline further, with the bottom possibly at the extraction cost of leading shale oil companies.

Additionally, the change in market style is also part of the factors.

On one hand, the arrival of the USA's interest rate cut cycle is happening, although inflation data is still fluctuating. On the other hand, domestic policies are also waiting for the right time to be released.

In this phase, the market is likely to shift from defensive strategies to offensive strategies such as growth stocks and technology stocks.

The selection of cnooc stocks mainly leans towards stable and sustainable competitiveness with high dividends. However, in reality, most funds are reluctant to wait a year for an 8% dividend when they can earn double in a month. For them, dividends are a reluctant defensive choice. As long as there is a tendency for market changes, they are unwilling to stay even for a second. A large number of dividend stocks, including cnooc, have experienced a pullback together.

Conclusion

If using dividend yield for valuation, the current 8% dividend yield of cnooc H shares and 5% of A shares still have attractiveness in their respective markets.

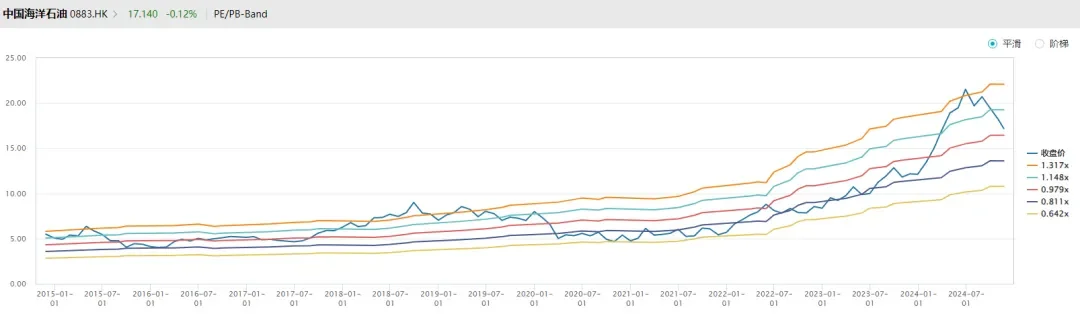

If viewed from the perspective of PB, it is quickly returning to the central position of the past 10 years.

If we look at the commonly used market cap/reserve ratio and market cap/output ratio in the oil & gas field. The netizen "和尚桥挑水" calculated that from 2014 to 2023, the average market cap per barrel of reserves was 89.86 Hong Kong dollars, and the market cap per barrel of output was 885.24 Hong Kong dollars.

By the end of 2023, reserves stood at 6.784 billion barrels, and output at 0.678 billion barrels. The corresponding average market cap was 609.6 billion Hong Kong dollars and 600.2 billion Hong Kong dollars. In the first three quarters of 2024, the output increased by 8.5%, leading to a market cap increase of 8.5% to 651.2 billion Hong Kong dollars. Currently, with a market cap of 810 billion Hong Kong dollars, there is still some distance from the past average of these indicators.

Overall, due to changes in oil prices and the macro environment, cnooc's stock price has been under pressure. The stock price is not considered expensive, but investors looking to buy for the first time should either accept the current dividend yield or consider leaving a certain margin of safety at this more volatile macro stage.

Editor/Rocky

Comment(2)

Reason For Report