城更加速,城改支持范围扩大到近300个地级市。通知明确地级城市资金能平衡、征收补偿方案成熟的项目,均可纳入政策支持范围。按照要求,城中村改造政策支持范围从最初的35个超大特大城市和城区常住人口300万以上的大城市,进一步扩大到近300个地级及以上城市。城市更新改造体量增加和改造范围扩大,更利于通过项目投资进一步拉动企业参与改造。

城更加速,城改支持范围扩大到近300个地级市。通知明确地级城市资金能平衡、征收补偿方案成熟的项目,均可纳入政策支持范围。按照要求,城中村改造政策支持范围从最初的35个超大特大城市和城区常住人口300万以上的大城市,进一步扩大到近300个地级及以上城市。城市更新改造体量增加和改造范围扩大,更利于通过项目投资进一步拉动企业参与改造。From January to October, the top 50 real estate companies added new land construction area of 40.7856 million square meters, a year-on-year decrease of 40.51%.

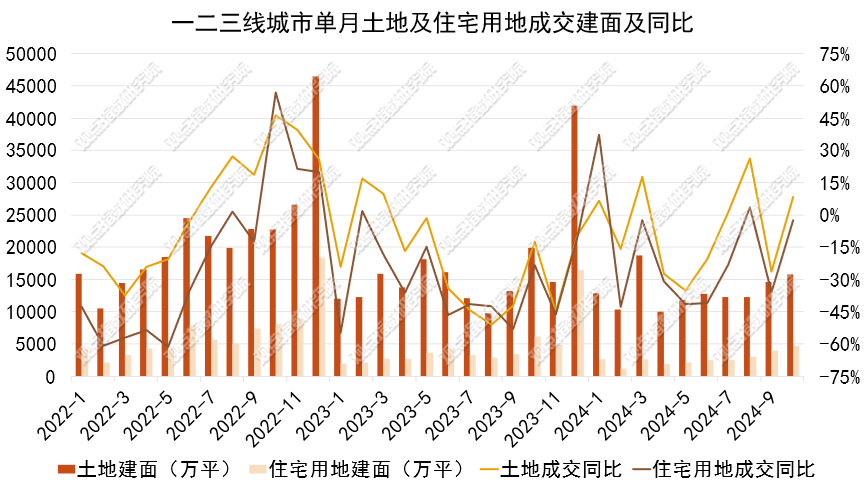

Intelligence Financial App learned that recently, the viewpoint index article stated that from January to October, the top 50 real estate companies added new land construction area of 40.7856 million square meters, a year-on-year decrease of 40.51%. Only seven enterprises acquired land with a value exceeding 20 billion, while only five enterprises acquired land valued between 10 billion and 20 billion. Urban land transactions are active, with an expected increase in land revenue. Residential land transactions in first, second, and third-tier cities totaled 723, with a planned construction area of 47.2031 million square meters, a 19.55% increase on a month-on-month basis, and a 24.24% year-on-year decrease. It is anticipated that many cities will continue to increase transactions by the end of the year, boosting land revenue.

Supply in first, second, and third-tier cities increased month-on-month, with relaxed price restrictions. Residential land supply in these cities comprised 3993.72 deals, with a planned construction area of 74.4466 million square meters, a 16.95% increase on a month-on-month basis, and a 13.65% year-on-year decrease. It is noteworthy that the Wangquansi Village shantytown in Fengtai District, Beijing, is the first land parcel in Beijing in over three years to not have an upper limit on land prices or guidance prices for selling commodity housing. This gives developers greater pricing flexibility when selling properties, enabling them to create products with different price systems to meet the varied demands of homebuyers.

Urban renewal accelerates, and urban renovation support expands to nearly 300 prefecture-level cities. The notice specifies that projects with balanced urban funds and mature expropriation compensation plans in prefecture-level cities can be included in the policy support scope. As required, the policy support for the renovation of urban villages has expanded from the initial 35 super-large and extra-large cities and major cities with a permanent population of over 3 million to nearly 300 prefecture-level and higher cities. The increased scale of urban renewal and expanded renovation scope are more conducive to further driving corporate participation in renovations through project investments.

Urban renewal accelerates, and urban renovation support expands to nearly 300 prefecture-level cities. The notice specifies that projects with balanced urban funds and mature expropriation compensation plans in prefecture-level cities can be included in the policy support scope. As required, the policy support for the renovation of urban villages has expanded from the initial 35 super-large and extra-large cities and major cities with a permanent population of over 3 million to nearly 300 prefecture-level and higher cities. The increased scale of urban renewal and expanded renovation scope are more conducive to further driving corporate participation in renovations through project investments.

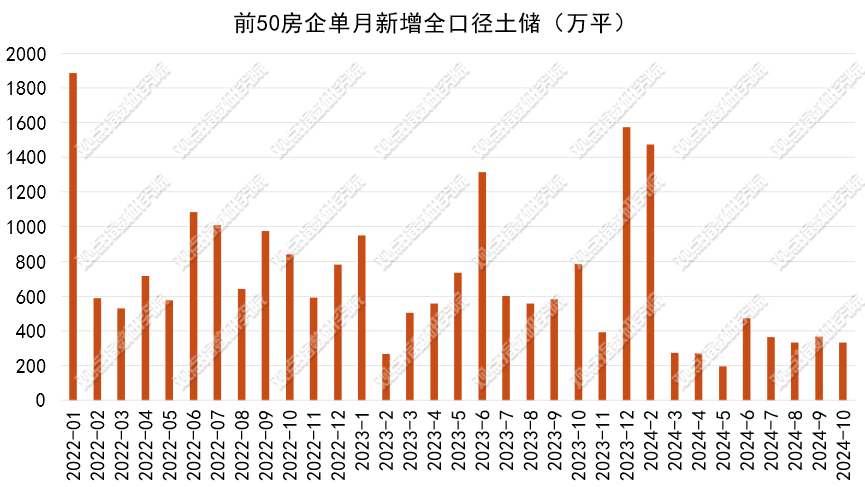

From January to October, the top 50 real estate companies added new land construction area of 40.7856 million square meters, a year-on-year decrease of 40.51%.

The real estate companies' report on new land reserves released by the Point of View Index shows that the top 50 real estate companies added a monthly new land construction area of 3.3169 million square meters, a 9.32% month-on-month decrease, and a 57.68% year-on-year decrease.

Data source: Point of View Index compilation

From January to October, the top 50 real estate enterprises added a total construction area of 40.7856 million square meters, a year-on-year decrease of 40.51%. Among them, Poly Developments, China Resources Land, and Shijiazhuang Guokong added new land reserves of 2.3318 million square meters, 2.1249 million square meters, and 1.7938 million square meters, respectively, leading the industry.

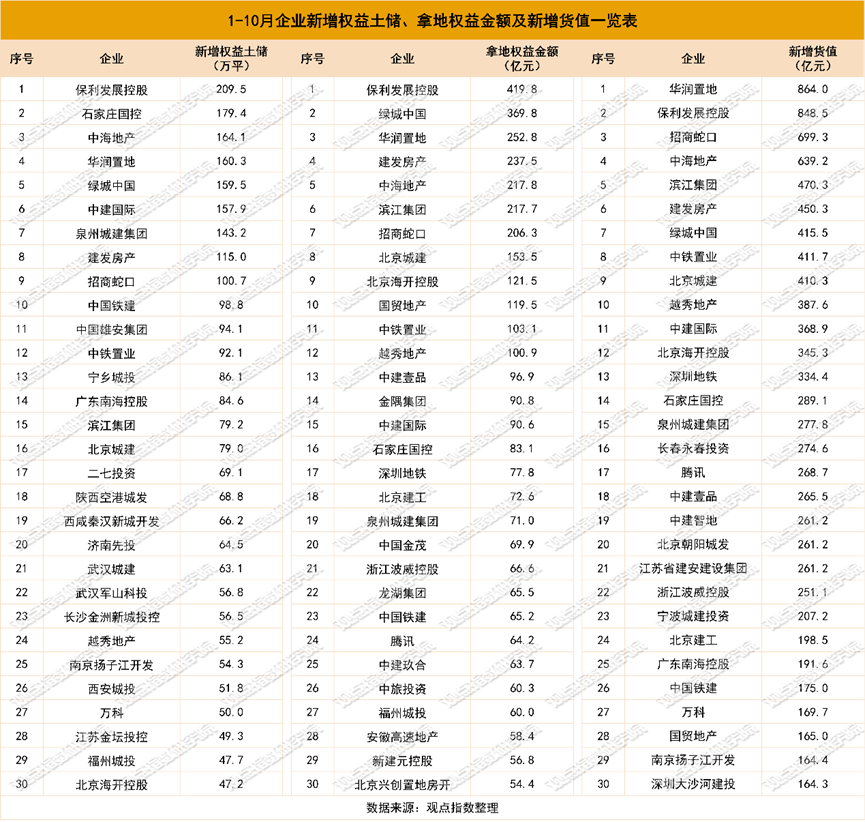

In terms of equity land acquisition amount, the enterprises with the largest investment in land from January to October are Poly Developments, Greentown China, Jiande Property, Hangzhou Binjiang Real Estate Group, and China Resources Land, with equity acquisition amounts of 41.984, 36.978, 25.279, 23.754, and 21.781 billion yuan respectively. In addition, Hangzhou Binjiang Real Estate Group and China Merchants Shekou Industrial Zone Holdings closely follow with land acquisition amounts of 21.77 billion yuan and 20.626 billion yuan respectively. There are only seven enterprises with land acquisition amounts exceeding 20 billion yuan, and only five between 10 billion and 20 billion yuan.

In terms of added value, the enterprises with the highest increase in land value from January to October are China Resources Land, Poly Developments, China Merchants Shekou Industrial Zone Holdings, Greenland Holdings, and Hangzhou Binjiang Real Estate Group, with added values of 86.399, 84.846, 69.927, 63.921, and 47.029 billion yuan respectively.

Urban land transaction is active, with expected increase in land revenue.

According to the Index of Viewpoint Monitoring, the number of land transactions in first, second, and third-tier cities during the reporting period was 3191; the planned construction area of land transactions was 157.9427 million square meters, up 8% MoM and down 21.45% YoY; the total transaction price was 285.397 billion yuan, up 16.96% MoM and down 31.42% YoY; the average transaction price per square meter was 1806.97 yuan, up 8.3% MoM and down 12.69% YoY.

Data Source: Wind, compiled by the Viewpoint Index.

In terms of residential land, there were 723 transactions of residential land in first, second, and third-tier cities, with a total planned construction area of 47.2031 million square meters, up 19.55% month-on-month and down 24.24% year-on-year; the total transaction price was 210.692 billion yuan, up 19.94% month-on-month and down 36.9% year-on-year; the average transaction price per square meter was 4478.01 yuan, up 6.46% month-on-month and down 16.44% year-on-year; with an average premium rate of 2.46%.

In the first-tier cities, from October 18 to November 18, Beijing completed 7 land transactions, with a total area of 0.4008 million square meters, a transaction price of 22.992 billion yuan, and 2 land parcels were transacted at a premium. The winning bidders included Beijing BBMG Corporation, Chi Mer Land, Greentown China, among others, with BBMG Corporation acquiring 2 land parcels within a week.

The sixth batch of land auctions in Shanghai included 4 land parcels, with a total area of approximately 0.1968 million square meters, and a total auction price of about 14.844 billion yuan. Only the Yangpu Dinghai land parcel won by Greenland Holding generated a premium, with a premium rate of 2.32%. Companies acquiring land in this batch include China Resources Land, Greenland Holding, Xiangyu Real Estate, and Shanghai Urban Investment. It can be seen that private real estate companies have not entered the market, and investments remain cautious.

From October 18 to November 18, Guangzhou completed transactions for 6 land parcels, with a total construction area of 0.3029 million square meters and a total price of 8.932 billion yuan, won by Poly Developments, Cinda Real Estate, Zhushi Real Estate, and other companies.

Among them, Poly Developments took all 3 residential plots in Pazhou South at the base price of 5.901 billion yuan, with a total floor area of approximately 0.138 million square meters. The plot ratio for the 3 parcels is 2.5, and the transaction floor price is around 43,000 yuan/square meter (excluding ancillary construction).

During the period, only 1 land parcel was transacted in Shenzhen. The parcel is located in Qianhai Merchants Street K104-0049, with a total area of 13,657.28 square meters and a planned construction area of 38,155 square meters. The land auction attracted the participation of four real estate companies including Tianjian Real Estate, Greentown China, China Railway Construction Real Estate, and China Merchants Shekou.

Ultimately, Tianjian Real Estate won the parcel at a price of 1.435 billion yuan, with a transaction floor price of 37,610 yuan per square meter, and a premium rate of 16.48%. It is worth noting that there is no set price limit for commodity housing sales on this plot, and it is not subject to the '70/90' unit type policy restrictions.

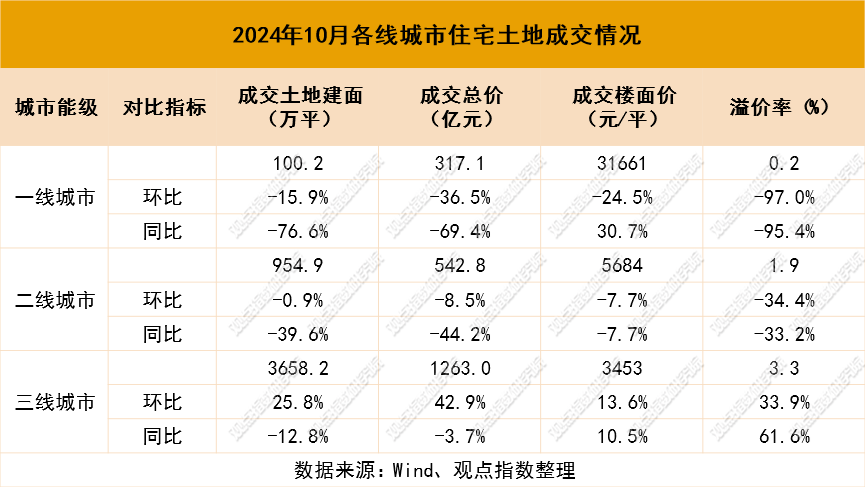

The planned construction area of residential land transactions in second-tier cities was 9.5488 million square meters, a decrease of 0.86% compared to the previous month and a decrease of 39.55% year-on-year; the total transaction price was 54.28 billion yuan, a decrease of 8.49% compared to the previous month and a decrease of 44.18% year-on-year; the transaction floor price was 5684.48 yuan/square meter, a decrease of 7.7% compared to the previous month and a decrease of 7.66% year-on-year.

The main cities for land transactions during the period include Fuzhou, Xiamen, Hangzhou, and Nanjing. On November 15, Fuzhou auctioned off 30 plots of land totaling 911.38 mu, with a starting price as high as 13.24 billion yuan. Among the 30 plots, 16 were residential plots, including 8 in Jin'an District, 1 in Cangshan District, and 4 each in Gulou and Taijiang districts. This broke the historical record of Fuzhou's four urban districts for the highest single supply of 30 plots. In the end, 14 residential plots were transacted, with a total transaction amount of 10.61 billion yuan.

The planned construction area of residential land transactions in third-tier cities was 36.5816 million square meters, an increase of 25.78% compared to the previous month and a decrease of 12.85% year-on-year; the total transaction price was 126.304 billion yuan, an increase of 42.94% compared to the previous month and a decrease of 3.71% year-on-year; the transaction floor price was 3452.66 yuan/square meter, an increase of 13.65% compared to the previous month and an increase of 10.49% year-on-year.

During the observation period, in the three-tier cities, the residential land auctions in third-tier cities increased month-on-month, with the increase expanding. It is expected that many cities will continue to increase transactions before the end of the year, increasing land revenue.

Data source: Point of View Index compilation

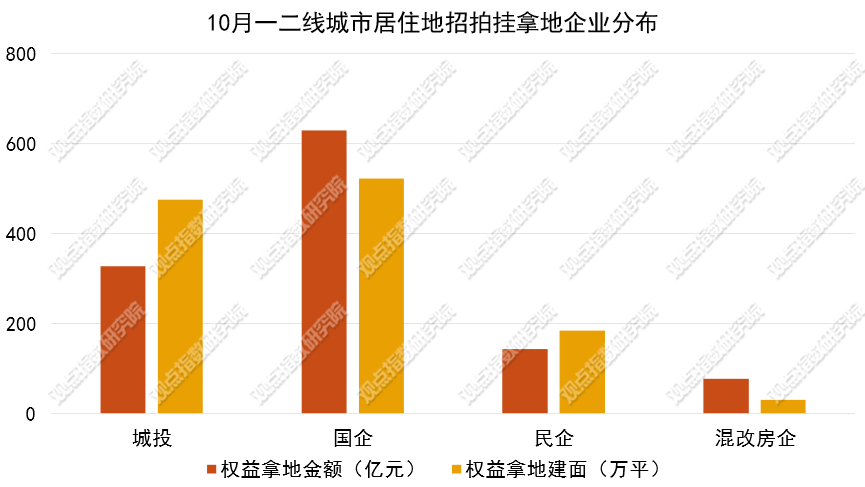

Viewpoint Index statistics show that in October, the types of enterprises that won bids for residential land in first and second-tier cities were mainly state-owned enterprises. In terms of equity land acquisition amount, the proportion of state-owned enterprises, urban investment entities, private enterprises, and mixed-ownership real estate enterprises during the reporting period were 53.43%, 27.83%, 12.14%, and 6.6% respectively.

Supply in first, second, and third-tier cities increased month-on-month, with relaxed price limit conditions.

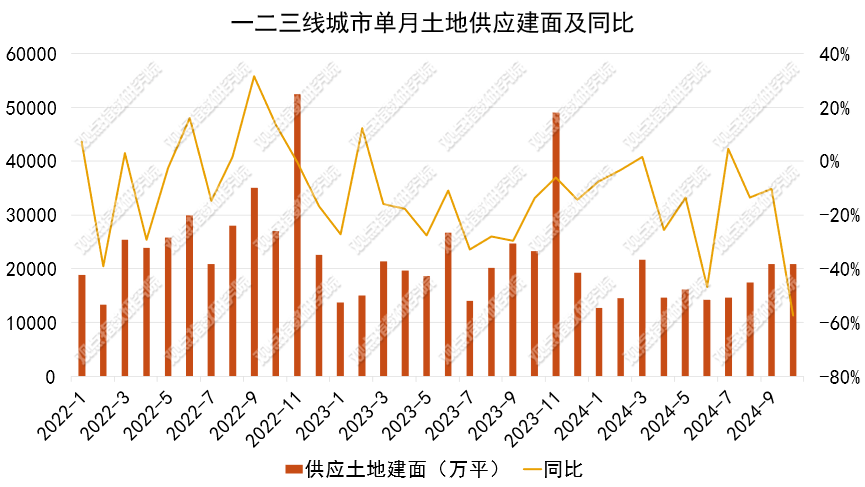

The data from the first, second, and third-tier cities monitored by the opinion index shows that during the reporting period, the number of land supplies was 3999 parcels, with a planned construction area of 208.4721 million square meters, a 0.4% decrease compared to the previous period, and an 11.96% year-on-year decrease; the starting price of land supply was 2132 yuan per square meter, a 23.17% increase compared to the previous period.

Data Source: Wind, compiled by the Viewpoint Index.

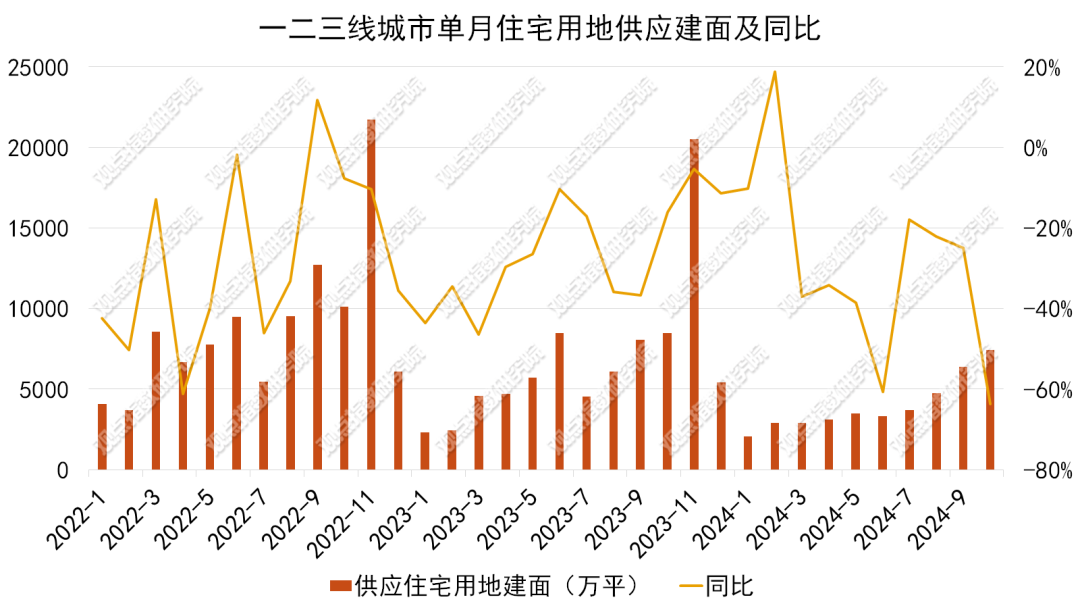

In terms of residential land, during the reporting period, the supply of residential land in first, second, and third-tier cities was 3993.72 parcels, with a planned construction area of 74.4466 million square meters, a 16.95% increase compared to the previous period, and a 13.65% year-on-year decrease; the starting price of land supply was 4637 yuan per square meter, a 10.09% increase compared to the previous period, and a 37.07% year-on-year increase.

Data Source: Wind, compiled by the Viewpoint Index.

During the period, the fifth round of planned commodity residential land supply list in Peking involved a total of 7 plots of land, with an area of approximately 0.32 million square meters and a planned construction scale of approximately 0.78 million square meters, scheduled to be supplied by November 30, 2024.

All projects in this round of supply are located within a 1000-meter radius of rail transit stations, including 5 projects in the central urban area, 3 in Chaoyang District, and 1 each in Fengtai District and Shijingshan District; and 2 projects in multiple locations, located in Changping District and Economic and Technological Development Zone respectively.

It is worth noting that the trading starting price of plot FT00-0613-0024 in the shantytown renovation and land development project in Wanquan Temple Village, Fengtai District, Beijing, is 11.054 billion yuan. The project site is located in Taipingqiao Street, Fengtai District, Beijing, with a land area of 0.0637 million square meters and a planned construction area of ≤0.1783 million square meters. In addition to the high starting price, this plot is also the first in Beijing in over 3 years without a set upper limit on land prices and guidance prices for commodity residential sales.

By canceling the maximum price requirement, developers will have greater freedom to set prices when selling properties in the future, making it more advantageous for developers to create products with different price systems, meeting the needs of buyers at multiple levels at once.

During the same period, a mixed residential and commercial land in Nanshan District's Houhai area was listed in Shenzhen with a starting price of 12.65 billion yuan. It is scheduled to be auctioned off at 3 pm on December 2nd, with the winning bidder determined by the principle of 'highest bid wins.' The announcement shows that the plot number of this land is T107-0107, the land area for sale is 0.034654 million square meters, with a plot ratio of 7.59, a construction area of 0.263 million square meters, and a starting floor price of 48,106 yuan per square meter.

On October 29, Shanghai issued the seventh batch of concentrated land supply auction announcement, involving Baoshan District, Pudong New Area, Hongkou District, Yangpu District, Putuo District, Minhang District, and Qingpu District, with a total starting price of 25.65 billion yuan.

On November 10, Guangzhou listed 8 plots for sale at a total starting price of approximately 4.85 billion yuan. Among them, 5 plots involve residential land located in Huangpu, Baiyun, and Huadu Districts.

Among the listed plots this time, the most attention is on Shuanggang Parking Lot (Phase I) in Huangpu District, with a land area of 50,415 square meters and a planned construction area of 109,436 square meters. The starting total price is 1860.42 million yuan, and the starting floor price is 17,000 yuan per square meter. The plot is located above Shuangsha Metro Station and is expected to be developed with integrated platform above the metro, connecting the residential part to the metro.

It is understood that near Shuangsha Metro Station, there is the Yueshan Project of Zhongjian Maritime Silk Road City, which plans to create an international dynamic waterside area of 2.37 million square meters, with a total investment of about 28.9 billion yuan and a total construction area of about 3.3 million square meters. Therefore, the pressure on the old Huangpu area due to Shuanggang Parking Lot (Phase I) in Huangpu District is not small.

During the reporting period, there were 233 residential land supply cases in second-tier cities, with a planned construction area of 14.6186 million square meters, an increase of 17.07% compared to the previous period and a decrease of 29.84% year-on-year; the starting floor price for the land supply was 6,965 yuan per square meter, an increase of 33.4% compared to the previous period and an increase of 31.26% year-on-year.

Wuxi and Wuhan are the main cities for land supply during the reporting period. The total area of residential land under auction in Wuxi is approximately 1.4586 million square meters, with a total starting price of 22.076 billion yuan. The total area of residential land under auction in Wuhan is approximately 1.0014 million square meters, with a total starting price of 9.068 billion yuan.

During the reporting period, there were 932 parcels of residential land supplied in third-tier cities, with a planned construction area of 58.2397 million square meters. This marks a 17.42% increase on a month-on-month basis and a 10.31% decrease on a year-on-year basis. The starting floor price for these parcels was 3486 yuan per square meter, showing a 12.2% increase month-on-month and a 30.03% increase year-on-year.

During the period, the supply of land increased in second and third-tier cities. It is worth noting that two billion-dollar land parcels were introduced in first-tier cities during this period. The introduction of high-quality land parcels is ultimately to stimulate the investment enthusiasm of real estate enterprises. However, the investment amount for these large land parcels is substantial and not all companies can afford it. The starting prices alone pose a threshold for companies with limited financial strength.

On November 11th, the Ministry of Natural Resources issued a notice regarding the use of special local government bond funds to acquire idle land. The notice emphasizes the control of incremental land, optimization of existing land, and improvement of quality, to support the activation of idle land. It is expected that the future increase in land supply will correspondingly decrease, while the efficiency of utilizing existing resources will be greatly enhanced.

Urbanization is accelerating, and the scope of urban transformation support has expanded to nearly 300 prefecture-level cities.

The Ministry of Housing and Urban-Rural Development revealed that in 2024, the national plan aims to start the renovation of 0.054 million old residential areas in urban towns. According to statistics reported by various regions from January to September, a total of 0.048 million old urban residential areas started renovation nationwide. In terms of regions, Jiangsu, Shanghai, Jilin, Qinghai, and four other regions have all started the renovation.

According to CCTV News, the Ministry of Housing and Urban-Rural Development and the Ministry of Finance recently jointly issued a notice, specifying that projects with mature funding balance and compensation solutions in prefecture-level cities can be included in the policy support scope. As required, the policy support scope for urban village transformation has expanded from the initial 35 super large and mega-cities and cities with a permanent population of over 3 million, to nearly 300 prefecture-level and above cities.

The Opinion Index believes that the increase in the scale of urban renewal projects and the expansion of the renovation scope are more conducive to further stimulating business participation in the renovation through project investments.

In terms of cities, the first phase of the Miao Ling Village renovation project in the Xiannexin City Center area of Wuhan formally started in Huarong District, Ezhou City, marking the official start of Wuhan's largest-scale old city renovation project. The total area of this renovation is 134 hectares (2123 acres), involving approximately 1681 households that have not been demolished, totaling 5044 people. The total construction area of the demolition and renovation is approximately 504,416 square meters, including 424,857 square meters of residential area, 72,059 square meters of commercial area, and 7,500 square meters of office area.

The Guangzhou Planning and Natural Resources Bureau disclosed the detailed control plan for the Xin'an Tan Village area in the Guangzhou Bay Area, marking a new progress for the renovation of the Tan Village in Baiyun District.

According to the plan, Tan Village will be transformed into a purely residential community, with the addition of 20 residential land parcels, 10 commercial land parcels, and 2 primary and secondary school land parcels. This plan will transform the original village and undeveloped land into residential and commercial land. The total planned land area of the Tan Village area is approximately 234 hectares, with a total construction volume of about 3.74 million square meters, a scale close to the transformation volume of four Liede villages.

During the period, Shui On Land signed a cooperation framework agreement with Nanqiao Town, Fengxian District, Shanghai for the 'Beigang Village' renovation project. The 'Beigang Village' renovation project is located in the core area of Nanqiao Town in Fengxian New City, Shanghai, with an overall renovation area of about 779.08 acres and a planned total construction area of about 0.497 million square meters.

The Longgang Nanwan Xiali Lang Urban Renewal Project in Shenzhen has been approved, with China Resources Land participating in the development. The project is located in the Xialang Street, Longgang District. The land area for the project renewal unit is 416,056.3 square meters, the demolition area is 281,185.1 square meters, the development construction area is 166,209.9 square meters, and the planned volume is 966,833 square meters. This renewal project will include various functions such as residential, commercial, office, and hotel buildings, with a residential area of 834,778 square meters, including 88,839 square meters of affordable housing.