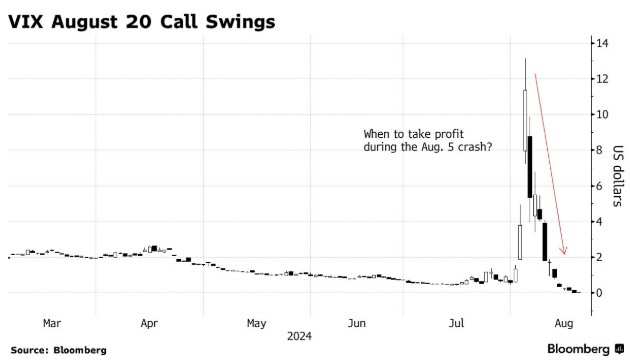

更为戏剧性的是,在 8 月 5 日的波动性冲击期间,预期股市波动率指标创下历史新高,但在一周内几乎回吐了所有涨幅。当天近月期货的涨幅远低于预期。

更为戏剧性的是,在 8 月 5 日的波动性冲击期间,预期股市波动率指标创下历史新高,但在一周内几乎回吐了所有涨幅。当天近月期货的涨幅远低于预期。Should investors choose VIX call options or S&P 500 index put options? As the peaks of the CBOE Global Markets volatility index become shorter, this question has become central.

In terms of hedging, should investors choose VIX call options or S&P 500 index put options? As the peaks of the CBOE Global Markets volatility index become shorter, this question has become central.

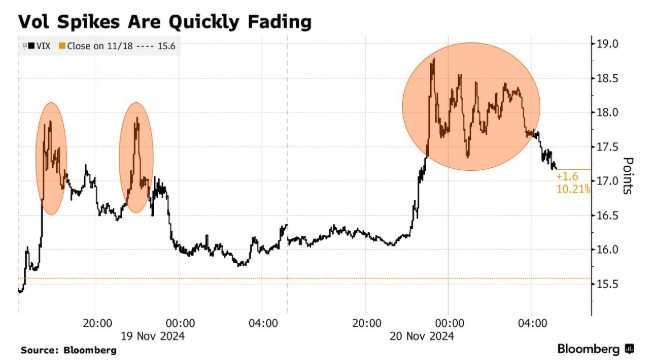

According to the Zhitong Financial APP, last week, due to escalating concerns over the ongoing conflict between Russia and Ukraine, the VIX index rose more than 2.3 points twice during the session. By the close, the VIX index had risen less than 1 point.

More dramatically, during the volatility shock on August 5th, the expected stock market volatility index hit an all-time high, but almost retraced all gains within a week. The increase in near-term futures that day was far below expectations.

More dramatically, during the volatility shock on August 5th, the expected stock market volatility index hit an all-time high, but almost retraced all gains within a week. The increase in near-term futures that day was far below expectations.

As the market increasingly views bad news as tail risks, investors are beginning to doubt the true effectiveness of volatility hedging — or their actual value, as any monetization of volatility now requires very quick profit-taking. The so-called volatility is usually very high under market pressure, which means that a surge in volatility may quickly turn into a crash - as recently proven, it's very difficult to profit from.

Moo Point Capital Management Stock Index Volatility Fund Managing Partner Jeremy Wien said: "The monetization of VIX call options is extremely difficult. That being said, the increase in VIX may be faster and more severe than the stock market decline, so in some cases, VIX call options can be a very useful hedging tool."

Wien added that VIX call options may be more suitable for guarding against geopolitical events, while S&P 500 put options may be more appropriate for hedge against weak economic data, disappointing earnings, or stock declines related to artificial intelligence.

In a recent research report, including Bank of America strategist Matthew Welty, hedge funders looking to choose between VIX call options or S&P 500 put options need to consider the reaction of volatility indicators, as a stock market crash does not necessarily cause a surge in volatility. Bank of America points out that the VIX options market accumulated significant imbalances in 2023 and 2024, which may not have been fully eliminated. Traders may find it difficult to hedge during market stress events, resulting in an increase in VIX futures.

On August 5th, given the rapid pace of market crashes and subsequent volatility selling, VIX call option holders may find it difficult to cash out their hedges. A report from the Bank for International Settlements shortly after emphasized that the bid-ask spread for S&P 500 put options widened significantly before normal trading hours, leading to an increase in the VIX spot price. Since the VIX spot price is calculated based on the midpoint of the bid-ask price, even without S&P 500 index options trading, this price level may rise.

Anne Van Kuijk, head of the S&P 500 index and VIX options department at Optiver Amsterdam, pointed out that in panic situations, the convexity of VIX call options is significantly higher than that of S&P 500 put options. The inflow of funds into leveraged short positions in VIX exchange-traded funds has reduced the cost of VIX call options.

French Industrial Bank derivatives strategist Jitesh Kumar stated that VIX and S&P 500 products serve different purposes. When investors buy S&P 500 put options, they are betting on index level options, while buying VIX call options allows them to remain sensitive regardless of the index level - as long as the volatility does not decrease. He added that many market participants also hold VIX tail risk hedging products for regulatory purposes, which is "very beneficial" to them.

Kumar concluded: "Investors need to choose hedge based on spot/volatility views."