这样就形成了市场可观的双边网络,还不用像外卖或者网约车那样,有大量实物和人员资产参与,全部在网络上运作,轻资产。今年以来,公司运用AI成功促进了业务发展,收入增速逐渐增快,整个华尔街都在期待AI应用侧出现大爆品,来证明Ai的大投入是有价值的,Applovin的成功,自然成为了当前大家想要的答案,在财报的刺激下,股价一年涨了七倍。

这样就形成了市场可观的双边网络,还不用像外卖或者网约车那样,有大量实物和人员资产参与,全部在网络上运作,轻资产。今年以来,公司运用AI成功促进了业务发展,收入增速逐渐增快,整个华尔街都在期待AI应用侧出现大爆品,来证明Ai的大投入是有价值的,Applovin的成功,自然成为了当前大家想要的答案,在财报的刺激下,股价一年涨了七倍。Essentially, it can be seen that the successful AI application stocks driven by AI are not really companies that use AI models with excellent external performance well, and something common to everyone does not constitute competitiveness. This also determines that the real AI application stocks are also very few.

Who is the hottest AI stock this year? Asking this question in the first quarter, the answer is still $Super Micro Computer (SMCI.US)$ , while asking this question two months ago, the answer is still $NVIDIA (NVDA.US)$ . And answering this question today, the most appropriate title for a stock falls on a new company. $Applovin (APP.US)$ 。

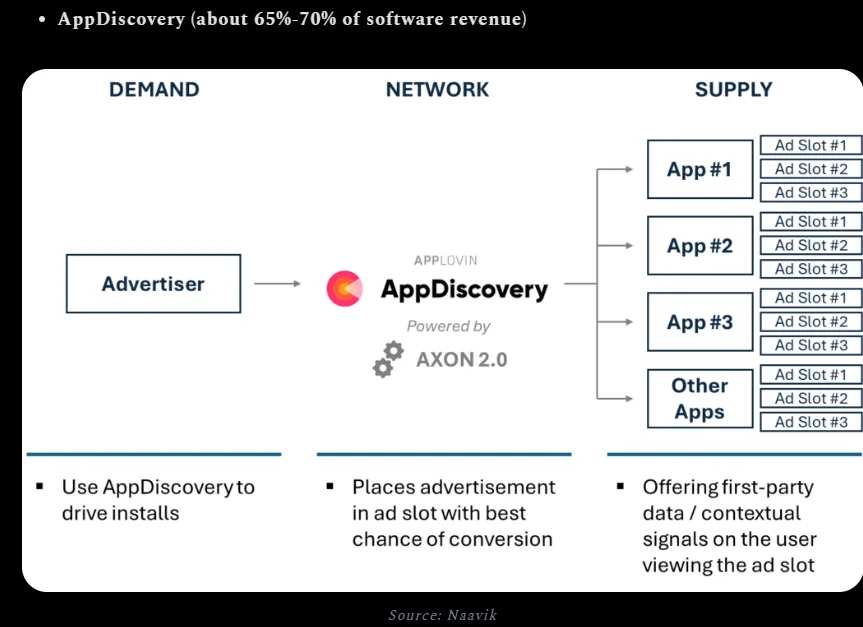

这家公司主要做的是一个广告中间商的角色,帮助大量的尾部互联网app,把用户流量时长变现,把广告位放到Applovin的平台上,而同时,Applovin将这些app背后的用户人群标签并分类,将这些广告位整理好提供给广告主。包括但不限于消费品公司、医药公司、其他互联网软件公司。

这样就形成了市场可观的双边网络,还不用像外卖或者网约车那样,有大量实物和人员资产参与,全部在网络上运作,轻资产。今年以来,公司运用AI成功促进了业务发展,收入增速逐渐增快,整个华尔街都在期待AI应用侧出现大爆品,来证明Ai的大投入是有价值的,Applovin的成功,自然成为了当前大家想要的答案,在财报的刺激下,股价一年涨了七倍。

这样就形成了市场可观的双边网络,还不用像外卖或者网约车那样,有大量实物和人员资产参与,全部在网络上运作,轻资产。今年以来,公司运用AI成功促进了业务发展,收入增速逐渐增快,整个华尔街都在期待AI应用侧出现大爆品,来证明Ai的大投入是有价值的,Applovin的成功,自然成为了当前大家想要的答案,在财报的刺激下,股价一年涨了七倍。

随着硬件股票整体业绩预期已高,难再有大惊喜,这些应用股也被视作是下一回合的Ai投资核心标的,会延续英伟达的爆发行情。Applovin跟$Palantir (PLTR.US)$并驾齐驱,已经成为了最火热的Ai股,而在中国市场,映射的标的也从硬件算力,切换到了AI应用股票上。当下,还是要理解一下,Applovin会不会像英伟达一样行情持续两年,且后续还有哪些预期的空间。

一、流量化的商业模式

首先网络广告这门生意本身是互联网最大的生意。一直是巨头们的自留地,腾讯微信、Meta、Google、字节跳动,它们的商业模式之所以能赚大钱,就是在于,它们有丰富的产品使用基数,很长的日均使用时长,流量即资产,在它们拥有的流量基础上,放入广告位,能够准确投放到全球的用户上,精准投放程度,传播广泛度,肯定比线下的广告更优。

As of today, any advertiser, regardless of the industry—energy, consumer goods, industrial products, software, finance—cannot avoid advertising on these internet plus-related giants when promoting something new.

But obviously, the entire internet is huge, and even though the giants are powerful, they cannot cover all the traffic. Many people still spend a lot of time on a large number of niche applications, including but not limited to: segmented media, social, and leisure games. These application developers are small independent companies, and it is difficult for them to find a wide range of advertisers to cooperate with, which will consume a lot of energy. Therefore, the monetization of traffic is low. However, this is also where their products have a relative advantage - with few ads and good user experience.

Advertisers will not target individual small applications one by one. But as the dominance of the giants strengthens, the barriers for advertising on Tencent, ByteDance, Meta, and Google continue to rise, with increasing investment returns. On the contrary, by combining several appropriate small segmented applications and advertising on them, you can achieve the goal of precise targeting of the audience while spending less.

These demands naturally give rise to traffic monetization matchmaking platforms, and this is the business model of Applovin.

However, this model is not easy to implement. Small applications need to be able to receive advertising fees from Applovin and make money before they will cooperate with you. Advertisers must also be willing to advertise here and see good returns after the ads.

Most advertisers still prefer internet giants as they have the most precise control over the entire internet traffic and audience coverage. Additionally, these internet giants can also provide monetization services for small apps because they have extensive advertiser resources.

For example, in China, a large number of low-monetizing small applications, including many mini-game apps, ad-watching game apps, reading apps, and segmented social media platform apps. They do not directly accept ads. Instead, their ad monetization functions need to interface with WeChat or ByteDance to distribute advertisers' demands and share revenue.

However, this approach has inevitably led to contradictions. Giants already have huge traffic and advertising spaces, and they prioritize earning money by showcasing good-quality ads on their own apps. This has resulted in small applications receiving low-quality ad revenue after joining internet giant ad alliances, creating opportunities for platforms like Applovin.

The development of Applovin is also related to its strategic orientation. It can be seen that the company itself is a software company with a large number of app applications. However, in recent years, both in-app purchases and ad revenue of the self-operated app business have been declining. Meanwhile, platform revenue is increasing. It can be said that the company's role as a software company is diminishing.

The self-operated app should be in the initial stage, prepared to have enough advertising space to attract advertisers, otherwise there will only be a small number of third-party app advertising spaces at the beginning, and advertisers will not consider it, thus the business cycle cannot move. As a large number of small apps integrate into the company's system, the commercial model has been established, the company starts earning intermediary fees, shifting the focus, and begins to use third-party apps at the tail end as core advertising spaces, gradually replacing its own product traffic, which is reasonable and sensible.

At this point, Applovin has completed the transition of its business model. Currently, the revenue growth from the intermediary advertising business exceeds the decline in software business, the former model is better, with higher profit margins. Therefore, we finally see Applovin achieving a significant increase in revenue and profit margins.

Of course, this model is not perfect. The revenue comes from advertisers' investment. From a macro perspective, the growth rate of internet advertising is not very fast, it just has a relative price competitive advantage against giants, being able to temporarily gain market share.

How much advertising revenue can be earned depends heavily on the ad placement. It is related to the size of internet tail traffic and the proportion of these tail apps integrating with Applovin. There is a ceiling, no matter how many more integrations happen, it won't be more than what meta can achieve in terms of ad placements. Expecting it to grow into an internet giant is unrealistic.

As an intermediary, the commission is limited. Advertisers' fees go to Applovin and then need to be distributed to various tail app developers. If it were META, most of the ad fees would be earned by themselves because the ad placements in their own apps belong to them. Therefore, Applovin's model is actually more challenging.

However, giants have their own issues, with bloated staff, high costs, and soaring research and development expenses. Currently, with Applovin's new model achieving a higher advertising return on investment, running costs for the model are higher, yet Applovin has also achieved profit margins comparable to giants in the short term.

But this model has a small possibility of a loophole. One day, some of the tail apps, the providers of ad spaces, may grow into internet giants and start running ads themselves. At that point, there will be a considerable loss of ad space resources, and a significant shift in advertiser demand, which could cause a significant impact on Applovin.

This loophole has a real example: TikTok, during its development, invested a lot in advertising promotion through meta and Google. These two platforms joyfully collected advertising fees, only to realize later that they were the ones who fueled TikTok's growth.

In the customer case studies of Applovin, not only consumer goods or financial companies that want to market are advertisers, but also many internet companies are using Applovin for advertising. Their goal, of course, is to monetize traffic, either through paid in-app purchases or selling advertising space for monetization. Some companies advertise in order to help others advertise in the future.

Second, uninterrupted growth.

And Applovin's success is not due to this industry model having an advantage.

Essentially, it is still the advertising industry, and other competitors have not benefited from it. For example $Unity Software (U.US)$ , the company is a game development engine, also providing software monetization services. Many tail-end game apps are developed using the Unity engine. After the game development is completed with Unity, it is packaged to provide advertising space for monetization, naturally aligning with the flow. There is a strong synergistic advantage.

But Unity, on the other hand, did not excel. In the middleman business, Applovin left Unity far behind. Unity always thought about how to make money from tail-end app developers, rather than looking at the bigger picture, building a system together, connecting with advertisers, and doing business like Meta and Google.

In 2022, Applovin proposed an acquisition to Unity, which had a larger market cap at the time. Unity thought Applovin's market cap was too small. Now, it's clear that Applovin has significantly outperformed Unity in both performance and market cap, and no longer sees Unity as a suitable partner. Having a gold mine at home, there are still people who need to go begging.

The key to victory is strategic focus, as mentioned above, the middleman's job is to optimize efficiency and deliver successful advertisements to advertisers in order to sustain.

Applovin also has 200 tail-end apps, whether to focus more on self-promotion or follow the generous third-party, the former is more cost-effective. However, the company should be clear that having so many apps does not make it a software giant, so one cannot rely on this. By pooling together all tail-end app traffic, efficient advertisements can be produced to truly establish the model.

Another point is the optimization in cost and automation, which also involves the core theme: AI.

Last year, after various models were introduced, the company quickly put them into use, one of which is the labeling algorithm. This algorithm uses limited usage information from tail-end apps to infer user attributes, classify tags, and determine suitable advertisements. This is actually consistent with the recommendation algorithms of most short video apps; the higher the accuracy of recommendations, the better. However, there is a significant difference in difficulty between recommendations based on gaming data and browsing data from users watching Youtube or analyzing hobbies from Instagram posts. This recommendation model is naturally the expertise of Applovin, a type of small AI model that sets the company apart from others. Of course, the more top-tier the advertising middleman, the more data analysis they can have, enabling them to make more precise tags. It can be said that this is a model with extremely strong economies of scale, where the first to expand will gain an advantage.

In addition, the company is most efficient in automated advertising investment. By using the AIGC model, the company automatically generates ad materials, significantly reducing the traditional design labor and time costs, thereby enhancing the efficiency of completing advertising tasks.

Therefore, it is not a problem that the company's business is AI-driven; the key lies in the rational application of its internal algorithm small models and the external AIGC large models.

The company has experienced huge declines since 2021, followed by significant increases, indicating an excessive reaction of the U.S. stocks to short-term performance.

From 2019 to the present, the company's performance has been steadily growing with no significant stagnation. In 2022, due to rate hikes and the overall decline of the internet industry, the revenue did not increase. The profit suffered during the years 2020-2022 due to a shift in business model, leading to poor performance.

But it was a bit excessive to drop to 1x PS at the worst time.

In 2023, the company's profit margin and revenue have reached new highs, and profits have also surged significantly. However, the stock price tripled last year and has not yet returned to the high level of 2021. This indicates that the company's valuation last year was still restrained. At 30 times P/E, it is an internet advertising company with good growth.

Since 2024, the company's revenue has accelerated to 40%, while the profit margin has increased from 10% to 30%, essentially completing a business model replacement.

As the market recognizes that the company's transformation to an AI-driven nature has led to a valuation increase surpassing performance, doubling, with ad tech valuations possibly at 30x PE and AI application valuations at 90x. Last year's performance was not attributed to AI+, thus there was no premium on valuation. Things look different now.

AI+ indeed provides growth benefits, but unlike NVIDIA, the software company's current rise is still driven by valuation appreciation. NVIDIA, on the other hand, has not had excessive forward-looking profit estimates in the last two years. Of course, the market's understanding may be that selling hardware is ultimately cyclical, but software has consistent earnings potential, hence the more optimistic valuation growth. Regardless, Applovin is an example of how to effectively use AI. Assuming future performance remains in an accelerated state, where revenue growth exceeds 50%, then Applovin's valuation can still rise, leaving room for further expansion.

The advantages of AI often benefit companies that are adept at utilizing AI, especially those transforming traditional business models within industries. However, the key point is targeting profits, a realm for true giants. Without aiming for markets like meta and Google, it would be difficult for Applovin to achieve such significant performance leaps. For many AI applications, without clear commercial monetization paths or taking advantage of current profit spaces, achieving such results is challenging.

Applying the same model in China would unlikely yield a space like Applovin's. Primarily, more tail-end applications in China run through WeChat mini programs rather than standalone apps. Tencent has strengthened its moat, making it harder for intermediaries in advertising to emerge. In the business model, driving distribution with a vast amount of small games.$XD INC (02400.HK)$The state may be the closest. But whether it can be done well, this is the same doubt as Unity, using AI is an ability, not just using the same ingredients to make the same dish.

Conclusion

Applovin's success is Ai's success, but not entirely, without the explosion of AI large models, the company is also actively transforming models, in fact, it is a suitable strategic focus. AI only accelerates this arrival, but in the long run, for example, using external AIGC models to produce advertising materials, reducing costs, can't other competitive companies imitate it, certainly they can. If everyone uses it, it means AI is useless. The decisive key is still its own label algorithm model, of course, this also counts as a small AI model.

So fundamentally, it can be seen that the AI application stock that succeeds because of AI is not really a company that uses externally well-performing AI models, what everyone has does not constitute competitiveness, Palantir is also driven by exclusive models. This also determines that true AI application stocks are also very few.

Editor/Somer