The prospect of "loose fiscal policy + re-inflation" is gradually becoming clearer, the trend of deteriorating US dollar credit may be difficult to reverse, central bank gold purchases are expected to continue to strengthen, thereby driving the long-term bull market for gold. In the future, we may see a decoupling of real interest rates, the US dollar index, and gold.

The prospects of "expansive fiscal policy + re-inflation" are becoming clearer, the trend of deteriorating dollar credit is difficult to reverse, and central bank demand for gold is expected to continue to strengthen, thus driving a long-term bull market for gold. In the future, we may see a long-term decoupling of real interest rates, the usd, and gold.

Do real interest rates and the US dollar index really explain the price of gold?

Are real interest rates the opportunity cost of holding gold? We believe this understanding neglects changes in US dollar credit. In fact, since the US dollar is not a completely risk-free currency, investors buying gold can be seen as buying "insurance" against US dollar default. What investors really need to compare is the real interest rate and the probability of US dollar default. If US dollar credit deteriorates significantly, even with rising real interest rates, gold may still be very attractive, as was typical during the 1970s stagflation era.

Are real interest rates the opportunity cost of holding gold? We believe this understanding neglects changes in US dollar credit. In fact, since the US dollar is not a completely risk-free currency, investors buying gold can be seen as buying "insurance" against US dollar default. What investors really need to compare is the real interest rate and the probability of US dollar default. If US dollar credit deteriorates significantly, even with rising real interest rates, gold may still be very attractive, as was typical during the 1970s stagflation era.

Is the US dollar index negatively correlated with gold? This understanding may generally apply in most cases, but it is important to note that the devaluation of the US dollar relative to other currencies does not necessarily equate to a devaluation of the US dollar relative to gold. For example, after the 2008 financial crisis, the world entered a period of major monetary easing, which meant that all credit currencies relative to gold should depreciate. However, due to the Eurozone being deep in a debt crisis at that time, the US dollar index did not trend weaker. Therefore, a depreciation of the US dollar is positive for the price of gold, mainly because a depreciating US dollar often represents a weakening trend in US dollar credit. If the US dollar index cannot accurately reflect the changing trends in US dollar credit, the correlation between the US dollar and gold may disappear.

What is the underlying investment logic of gold?

As the highest level of currency, gold can be understood as the opposite asset of the credit currency system. When the credit currency system suffers negative impacts, it may catalyze an upward movement in the price of gold. Whether it is real interest rates or the US dollar index, the correlation shown with the movement of gold essentially stems from changes in US dollar credit trends. Ignoring changes in US dollar credit and directly relying on historical statistical experiences may lead to incorrect conclusions.

How should future investment opportunities in gold be viewed?

Trump's policy proposals tend to lean towards larger fiscal expansion to support the economy, which means that the US economy may still maintain good performance, but this could pose obstacles to downward inflation. Under the combination of 'loose fiscal policy + re-inflation,' the pressure on US interest expenses may further increase, thereby raising the long-term deficit center, leading to continuous deteriorating pressure on the US dollar credit, thus supporting gold's long-term strength. It has been observed that the pace at which global central banks increase their gold holdings significantly precedes the pace of expansion of US debt, indicating that global central banks' expectations regarding US dollar credit are one of the significant factors in determining whether to buy gold. Therefore, against the backdrop of a potential further acceleration in the speed of US debt expansion, the demand for gold from global central banks may further strengthen, thus continuing to be an important driver of the gold bull market.

In the short term, after Trump was elected as the President of the United States, gold fluctuated weaker, mainly due to the pressure of a strong US dollar and concerns about potential fiscal contraction. However, we believe that this round of strong US dollar trading may be nearing its end, and the 'Government Efficiency Department' led by Musk may not actually have real power. Potential proposals such as streamlining government departments may face significant resistance. Before these proposals are actually implemented beyond expectations, the impact on gold prices may be limited. The expansion of deficits and accumulated debts under the background of 'loose fiscal policy + re-inflation' is a more certain trading clue. Therefore, we believe that the current phase of correction has brought good allocation opportunities, which can be actively monitored.

Is Gold 'De-Anchoring'?

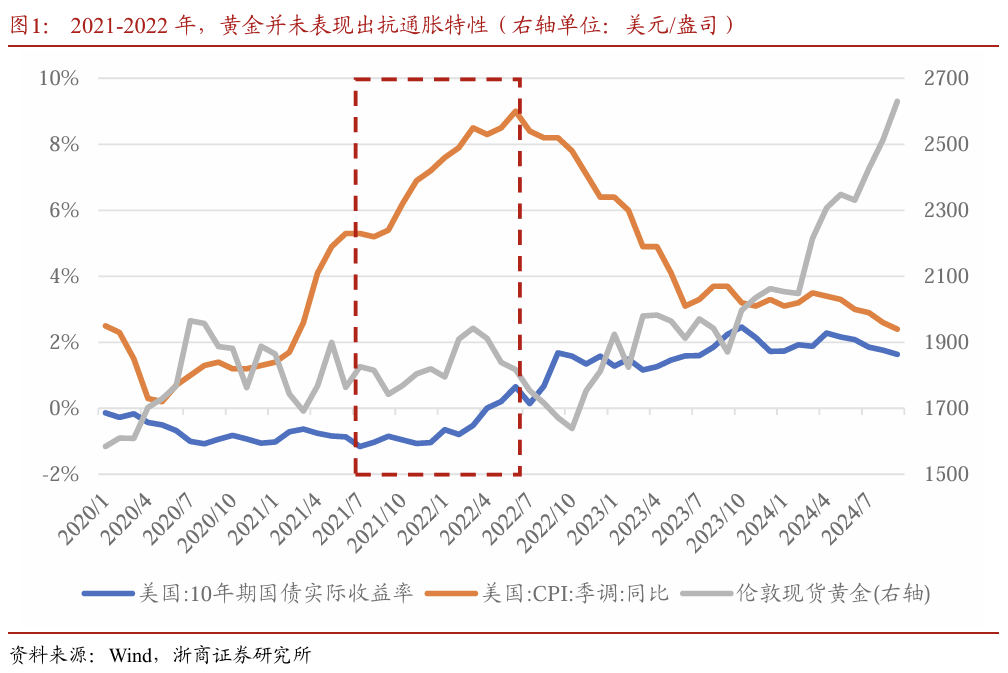

In October 2024, against the backdrop of waning interest rate cut expectations, rising real interest rates, an uptrend in the US dollar index, and easing geopolitical concerns, gold continued to set historical highs, displaying a trend that decouples from traditional pricing factors, showing stronger performance beyond market expectations. Market explanations have mostly focused on re-inflation concerns triggered by Trump's policies. However, this viewpoint still cannot explain the contradiction within traditional analytical frameworks - the simultaneous rise of real interest rates and gold prices. For example, during the significant inflation surge in the US in 2021-2022, as real interest rates rose, gold showed overall oscillatory adjustments and did not exhibit anti-inflation characteristics.

To determine the future trend of gold, we need to clarify whether the recent 'abnormal' performance of gold is indeed disconnected from the fundamentals. What is the core logic driving the gold bull market? Below, we will, on one hand, conduct a simple review of historical gold bull markets to identify the core drivers of each bull market, and on the other hand, through logical deduction, explain the core mechanism behind the anomalies.

Historical Evolution of Gold Bull Market

Since the dissolution of the Gold Standard, gold has experienced two long bull markets from 1976-1980 and 2001-2011, let's briefly review each of them.

1976-1980

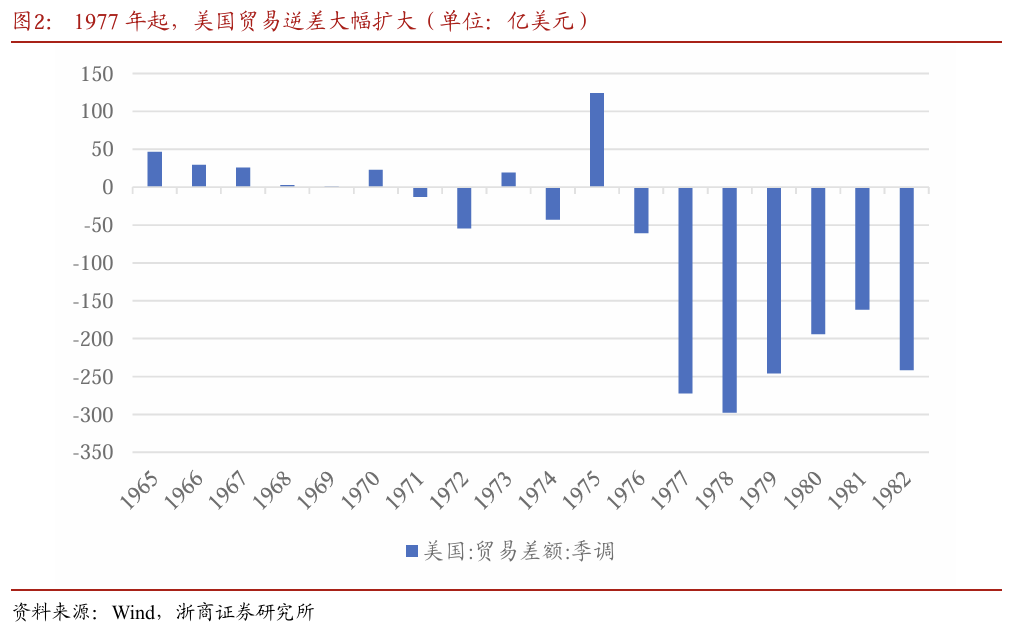

1977-1978: The deterioration of the international balance of payments triggered the US dollar crisis. Starting from 1977, the United States transformed from a trade surplus to a trade deficit, with the deficit significantly expanding, causing concerns in the market about the US dollar's credit issues, leading to a sharp devaluation of the dollar. From January 1977 to October 1978, the US dollar index fell by 21%, while during the same period, gold rose by 80%.

1979-1980: The Second Oil Crisis + Geopolitical Conflicts. In 1978, the Iranian Revolution overthrew the Pahlavi dynasty, leading to severe social unrest. From the end of 1978 to early March 1979, Iran ceased oil exports for 60 days, triggering the Second Oil Crisis. Crude oil prices surged, causing US CPI to rise to nearly 15% year-on-year, leading to stagflation. Subsequently, on November 4, 1979, the Iran hostage crisis erupted as militants seized the US Embassy in Iran, holding 52 American diplomats and civilians hostage. On December 24, 1979, the Soviet Union invaded Afghanistan, igniting the Afghan War. The prolonged crisis events significantly boosted risk aversion sentiment, with investors flocking to gold. Between January 2, 1979, and January 21, 1980, gold prices surged by 276%.

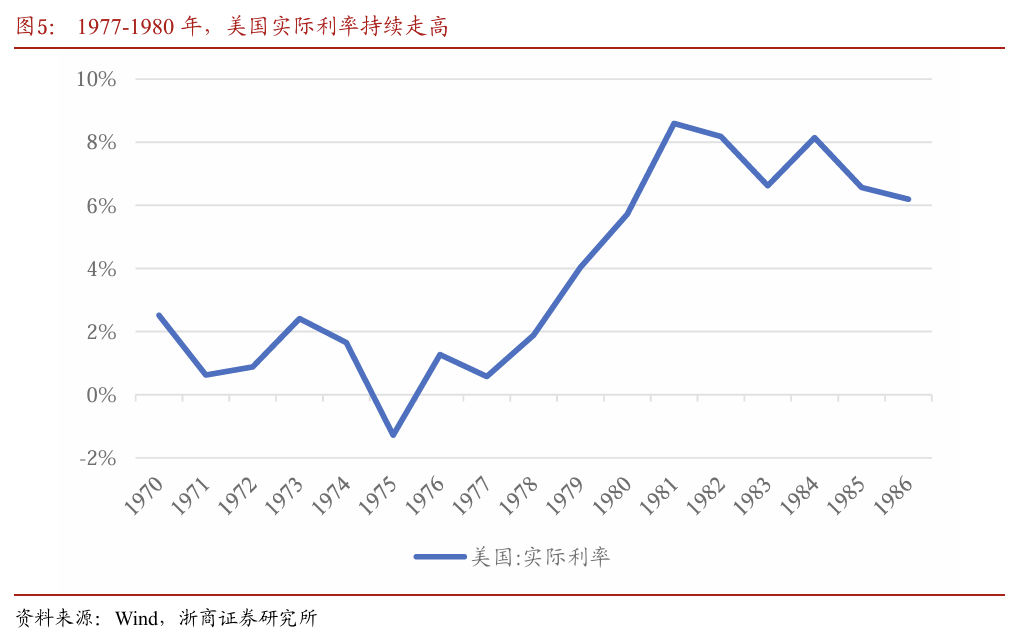

However, it is important to note that as shown in Figure 4, during this period, although US inflation spiked, the Federal Reserve implemented substantial interest rate hikes. Real US interest rates continued to rise from 1977 to 1980, showing a trend where real interest rates rose in tandem with gold prices.

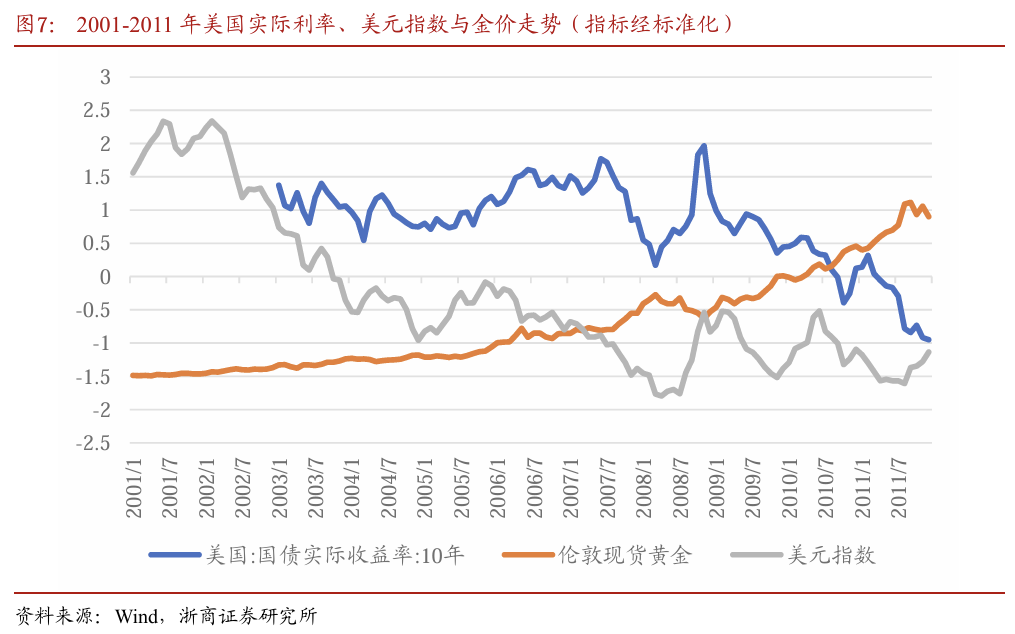

2001-2011

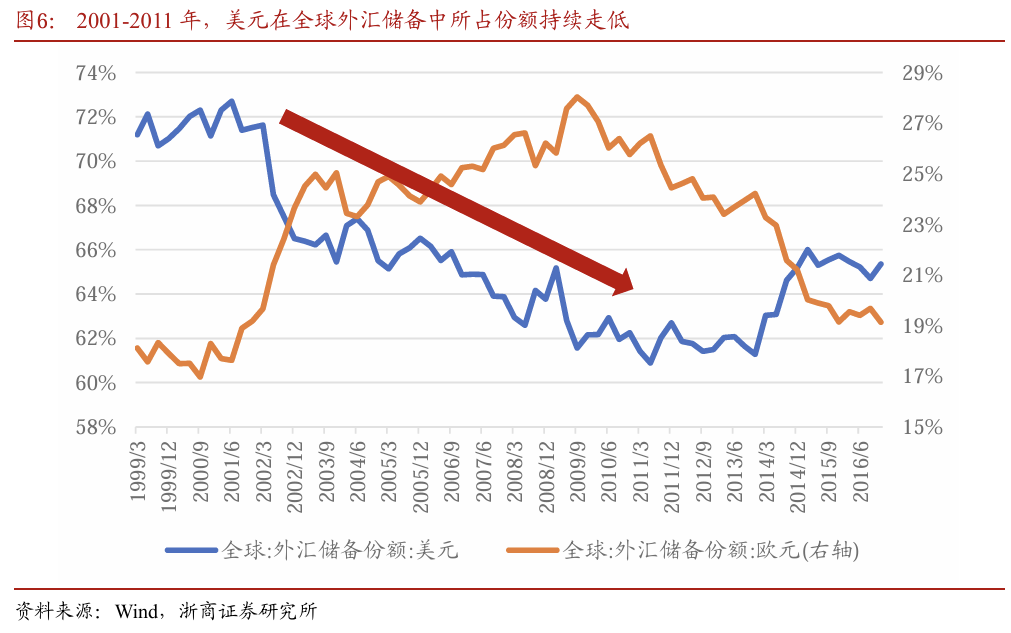

The continued decline in the US dollar's reserve currency status has driven the bull market in gold. In January 1999, the euro was officially launched and gradually became an important global reserve currency starting from 2001, challenging the US dollar's status. The US dollar's share in global foreign exchange reserves has continuously declined from 73% in 2001Q2 to 61% in 2011Q2. Along with the restructuring of the global credit monetary system, the US dollar has been continuously depreciating, fueling the bull market in gold. Additionally, after the 2008 financial crisis, the Federal Reserve initiated quantitative easing, further weakening the credibility of the US dollar.

From the trend of indicators during this period, we can also observe two characteristics:

1. Between 2003 and 2007, real interest rates fluctuated at high levels overall, showing weak correlation with the gold price trend, and only began to exhibit negative correlation after 2007.

2. The US dollar index hit a bottom around March 2008, followed by volatile movements, failing to reflect the decline in US dollar credit caused by the Federal Reserve's quantitative easing. Logically, the US dollar index reflects the exchange rate relationship between the US dollar and a series of other credit currencies. If the US dollar credit weakens synchronously with other currency credits, the US dollar may not significantly depreciate compared to other credit currencies, but it may depreciate compared to gold.

How to understand the logic of gold investment

Traditionally, it is often believed that: (1) Gold is an interest-free asset, and the real interest rate serves as the opportunity cost of holding gold. A decrease in the real interest rate tends to increase the demand for gold; (2) As a commodity priced in USD, a depreciation of the USD is bullish for the price of gold.

However, combining with the previous analysis, these two related relationships may become ineffective over a longer period of time. For example, gold and real interest rates rose simultaneously from 1977-1979, and from 2008-2011, the USD index oscillated at the bottom while the price of gold surged. We believe that this is because the market's interpretation of these influencing factors has not touched the essence:

1. Is the real interest rate the opportunity cost of holding gold? We think this understanding overlooks the changes in USD credit. In fact, since the USD is not a completely risk-free currency, investors buying gold can be seen as buying 'insurance' against USD default. What investors really need to compare is the real interest rate with the probability of USD default. If USD credit deteriorates significantly, even if real interest rates rise, gold may still be highly attractive, as seen in the typical case of the 1970s inflationary era.

2. Is the USD index negatively correlated with gold? This understanding may apply in most cases, but it is important to note that a depreciation of the USD compared to other currencies does not necessarily equate to a depreciation against gold. For example, after the 2008 financial crisis, the global economy entered a period of monetary easing, meaning that all credit currencies compared to gold should depreciate. However, due to the Eurozone being deeply mired in a debt crisis, the USD index did not weaken trend-wise during the same period. Therefore, a depreciation of the USD is bullish for the gold price, primarily because a depreciating USD often represents a weakening trend in USD credit. If the USD index fails to correctly reflect the changing trend of USD credit, the correlation between the USD and gold may disappear.

In summary, whether it is the real interest rate or the USD index, the correlation exhibited with the trend of gold can fundamentally be understood as the trend change in USD credit. Ignoring the changes in USD credit and basing conclusions directly on historical statistical experiences may lead to incorrect deductions.

How to determine future investment opportunities in gold?

"Robust fiscal policies + re-inflation" prospects are becoming clearer, and the trend of deteriorating USD credit may be challenging to reverse:

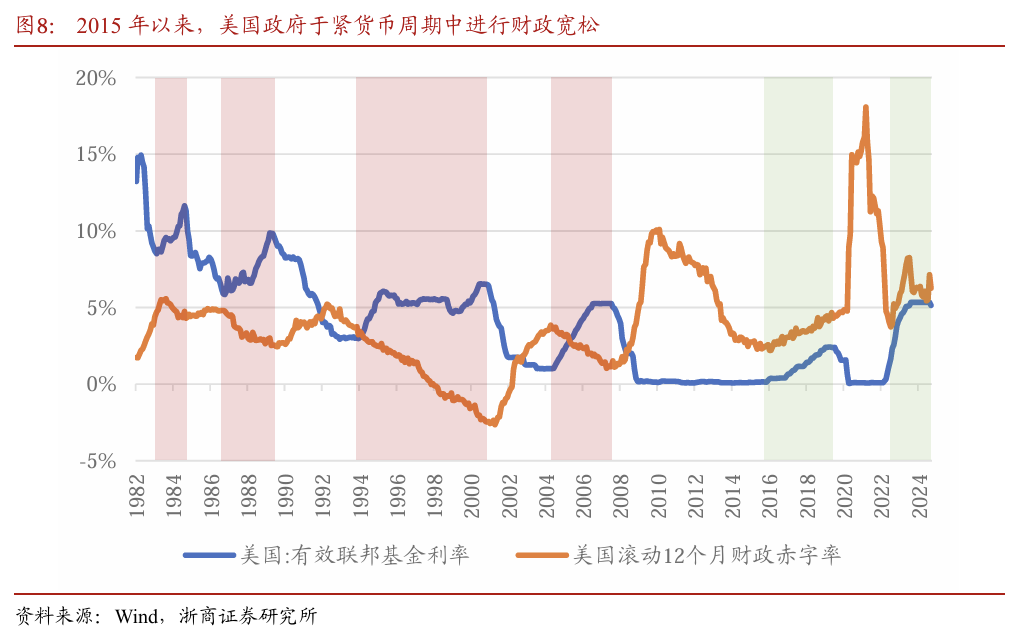

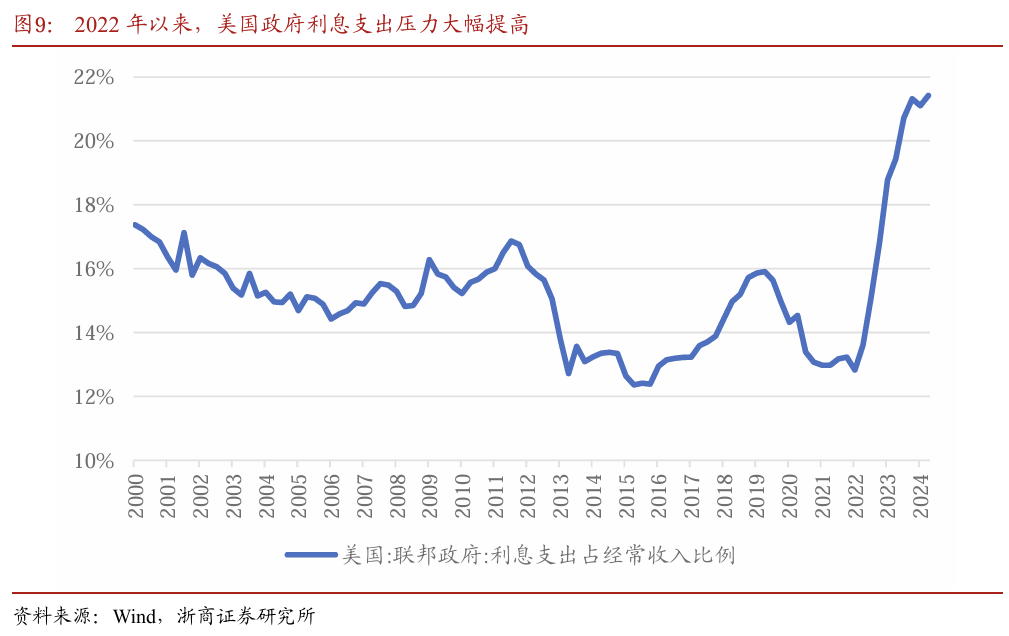

1. Sustained robust fiscal policies have led to a significant increase in interest expenses. In this cycle, the U.S. economy has been able to avoid a 'hard landing' during the interest rate hike cycle, largely thanks to the unusually proactive fiscal policy of the U.S. government. Since 1982, during monetary tightening cycles, fiscal policies often tightened simultaneously. However, since the interest rate hike cycle began in 2015, even during this cycle, the U.S. government's deficit rate has tended to expand, reaching a nearly 8% deficit rate in 2023. However, substantial fiscal expansion during the interest rate hike cycle has increased the debt repayment pressure on the U.S. government, with interest expenses accounting for over 20% of recurring income. This implies that high interest expenses will become a rigid expenditure for the U.S. government in the future, which may drive a systemic upward shift in the U.S. government's deficit rate, leading to a faster accumulation of U.S. debt pressure.

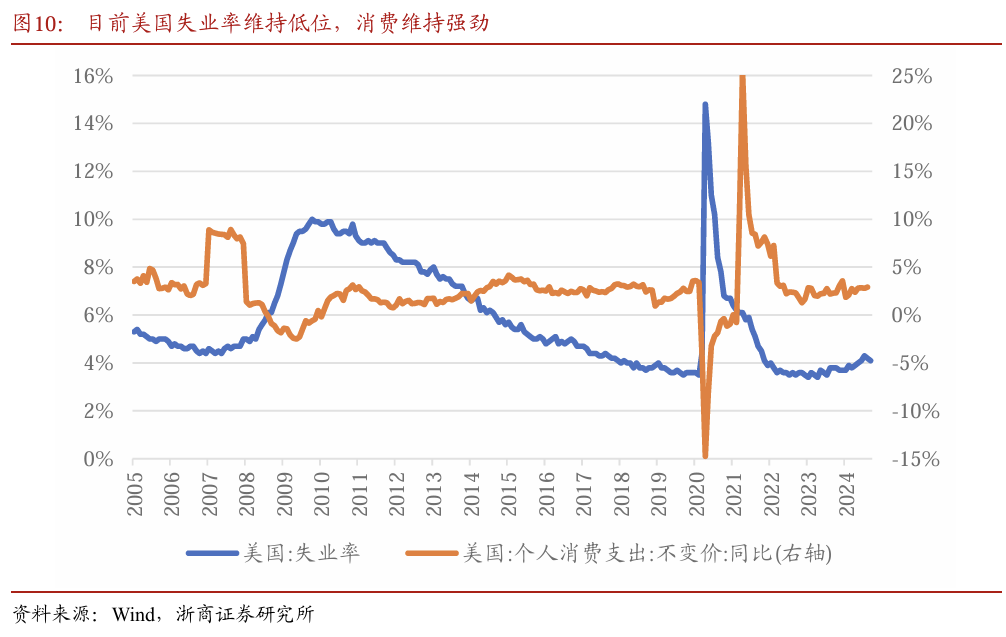

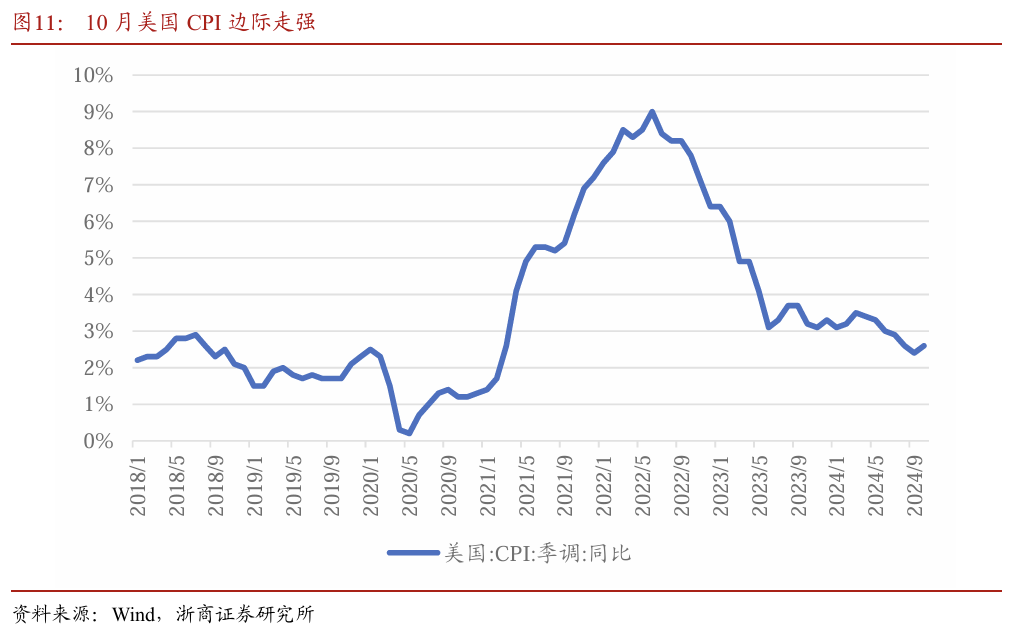

Against the backdrop of the strong resilience of the US economy, extensive fiscal policy may lead to an increase in inflation risks, with significant resistance to downward pressure on US interest rates in the future. Currently, with the support of extensive fiscal policy, the US economy shows strong resilience, maintaining a low unemployment rate, while personal consumption expenditure remains robust. Looking ahead, after Donald Trump is re-elected as the next US president, his policy stance tends towards larger-scale fiscal expansion to support the economy, implying that the US economy may continue to perform well, which could hinder downward inflation. In fact, US CPI in October has shown marginal strength, and if subsequent fiscal stimulus intensifies, the risk of reflation may significantly increase. Under the combination of 'extensive fiscal policy + reflation,' the pressure on US interest payments may further increase, thereby further elevating the long-term deficit center, which will create sustained deteriorating pressure on the US dollar credit, thereby supporting the strengthening of gold.

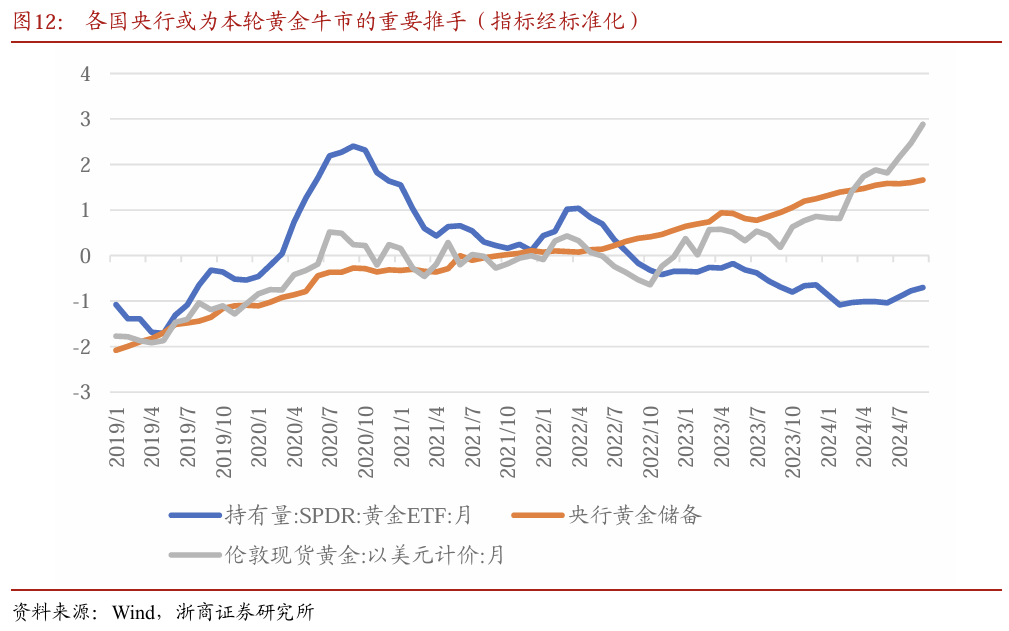

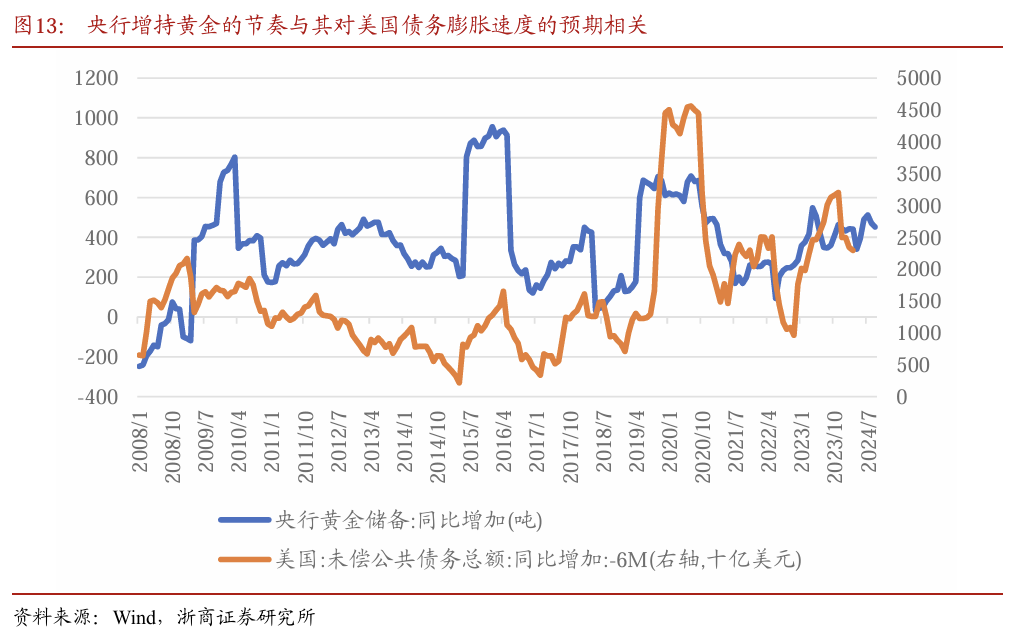

Central banks around the world are expected to continue to be important drivers of this round of the bull market for gold. Since 2021, while the holdings of gold ETFs representing ordinary investors have fluctuated downwards, central banks have continued to increase their holdings of gold, possibly making them the most significant driver of this round of the gold bull market. Historically, we have observed an interesting correlation: the pace at which central banks worldwide increase their gold holdings significantly precedes the pace of expansion of US debt. As the scale of US debt increases, indicating a worsening of US dollar credit, this observation suggests that global central banks' expectations of US dollar credit are one of the important factors influencing their decision to purchase gold.

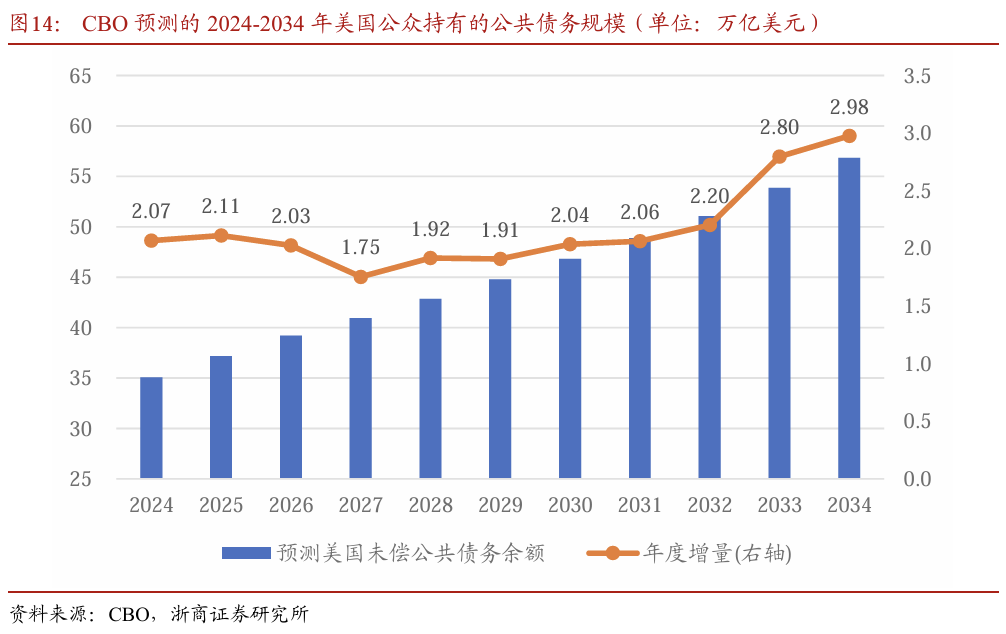

Looking ahead, according to the report released by the CBO (Congressional Budget Office) of the USA in June 2024, under the current circumstances, the US is expected to increase its debt by $2.11 trillion for the fiscal year 2025, higher than the $2.07 trillion in the fiscal year 2024. At the same time, based on the report recently released by the Federal Budget Accountability Committee, under a neutral assumption, Trump's economic policies may add $7.75 trillion to the US debt in the next 10 years, which means that the subsequent expansion rate of US debt may further intensify, leading to a possible increase in central bank demand for gold, thereby continuously boosting the price of gold.

In the short term, after the US election, from November 6th to 14th, gold continued to adjust, with a cumulative decline of 6.4%. The mainstream explanations in the market include:

1. After the election, uncertainty decreased, and Trump tended to quickly resolve geopolitical conflicts such as Russia and Ukraine, reducing the expected geopolitical risks, thereby reducing the safe-haven value of gold.

2. Trump's trades are cashed out, and funds are profit-taking.

3. The strong US dollar index suppresses the price of gold.

Combining the trends of various asset classes, the recent weakness in gold may come from strong US dollar suppression and potential concerns about fiscal contraction. From November 6th to 14th, Brent crude oil fell by 3.9%, London gold fell by 6.4%, while the US dollar index rose by 3.3%. Logically, if the decline in gold prices is mainly driven by downward geopolitical risk concerns, then oil prices should also significantly drop simultaneously, but the actual decline in oil prices is relatively small. Since the 12th, Brent oil has stopped falling and risen, deviating from the trend of gold prices. Secondly, after Trump's election, the US dollar strengthened significantly, indicating that Trump's trades have not ended, contradicting the explanation of profit-taking. Overall, we believe that the recent significant drop in gold prices is due to a combination of two factors: on one hand, driven by Trump's trades, the strong US dollar is exerting short-term pressure on gold prices; on the other hand, after Trump's victory, the formal announcement of the intention to establish the "Government Efficiency Department," and Musk's previous statement of cutting approximately $2 trillion in federal government expenditures to reduce the deficit will strengthen the US dollar's credit, leading to a decline in gold prices.

In the short term, we believe that the current adjustment in gold has been relatively sufficient, making it a good timing for layout. Regarding the US dollar trend, on one hand, the latest trends of the October US CPI and Core CPI are in line with market expectations, and inflation has not exceeded expectations further, indicating that the economy does not have a solid foundation for a significant US dollar appreciation; on the other hand, the market's interest rate cut expectations for 2025 have been revised down to only two cuts, indicating that trading has been relatively sufficient. With the strong uncertainty in the rhythm and intensity of Trump's policies, there is limited space for short-term trading rate increases, and the US dollar index may gradually shift to a fluctuating trend. As for Musk's announced spending reduction plan, at present, the position of the "Government Efficiency Department" is to provide advice and guidance from outside the government, which may not actually have real power. The potential proposals for streamlining government departments may face significant resistance, and the impact on gold prices may be limited until actual unexpected outcomes materialize. Under the background of "broad fiscal + re-inflation," the expansion of deficits and accumulation of debts are more certain trading clues.

Risk warning

Based on historical data statistics, the conclusion of this article is that there is a risk of failure in the future.

If the USA tightens fiscal discipline, it may lead to a decrease in the price of gold.

This article is from zheshang, edited by Jiang Yuanhua at China Fortune.