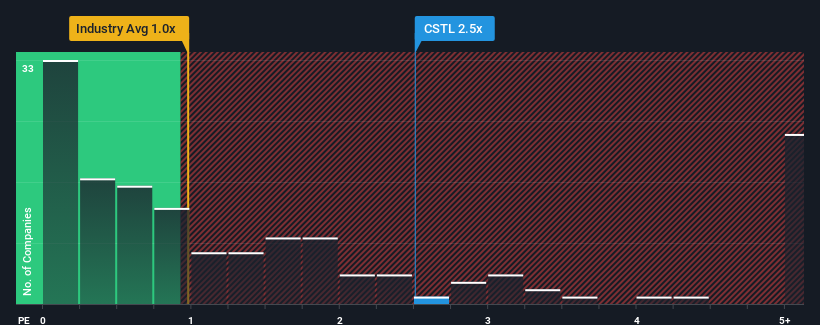

Castle Biosciences, Inc.'s (NASDAQ:CSTL) price-to-sales (or "P/S") ratio of 2.5x may not look like an appealing investment opportunity when you consider close to half the companies in the Healthcare industry in the United States have P/S ratios below 0.9x. However, the P/S might be high for a reason and it requires further investigation to determine if it's justified.

What Does Castle Biosciences' Recent Performance Look Like?

Recent times have been advantageous for Castle Biosciences as its revenues have been rising faster than most other companies. It seems the market expects this form will continue into the future, hence the elevated P/S ratio. However, if this isn't the case, investors might get caught out paying too much for the stock.

Want the full picture on analyst estimates for the company? Then our free report on Castle Biosciences will help you uncover what's on the horizon.How Is Castle Biosciences' Revenue Growth Trending?

In order to justify its P/S ratio, Castle Biosciences would need to produce impressive growth in excess of the industry.

Taking a look back first, we see that the company grew revenue by an impressive 62% last year. The strong recent performance means it was also able to grow revenue by 261% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Taking a look back first, we see that the company grew revenue by an impressive 62% last year. The strong recent performance means it was also able to grow revenue by 261% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Shifting to the future, estimates from the nine analysts covering the company suggest revenue should grow by 0.9% each year over the next three years. With the industry predicted to deliver 7.2% growth each year, the company is positioned for a weaker revenue result.

With this information, we find it concerning that Castle Biosciences is trading at a P/S higher than the industry. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. There's a good chance these shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with the growth outlook.

The Final Word

Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

Despite analysts forecasting some poorer-than-industry revenue growth figures for Castle Biosciences, this doesn't appear to be impacting the P/S in the slightest. The weakness in the company's revenue estimate doesn't bode well for the elevated P/S, which could take a fall if the revenue sentiment doesn't improve. Unless these conditions improve markedly, it's very challenging to accept these prices as being reasonable.

There are also other vital risk factors to consider and we've discovered 2 warning signs for Castle Biosciences (1 can't be ignored!) that you should be aware of before investing here.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.