The a.k.a. Brands Holding Corp. (NYSE:AKA) share price has fared very poorly over the last month, falling by a substantial 32%. Of course, over the longer-term many would still wish they owned shares as the stock's price has soared 121% in the last twelve months.

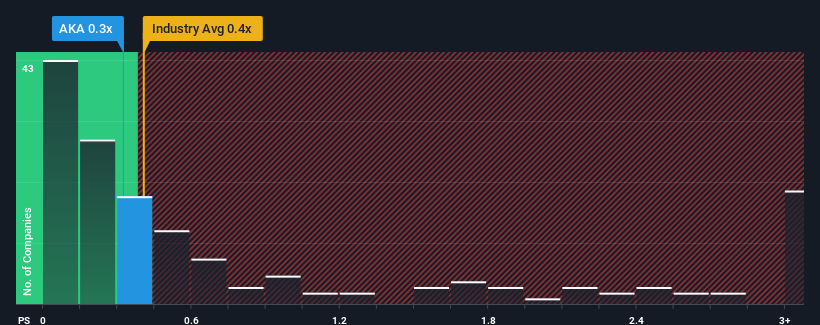

Even after such a large drop in price, there still wouldn't be many who think a.k.a. Brands Holding's price-to-sales (or "P/S") ratio of 0.3x is worth a mention when the median P/S in the United States' Specialty Retail industry is similar at about 0.4x. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

What Does a.k.a. Brands Holding's P/S Mean For Shareholders?

Recent revenue growth for a.k.a. Brands Holding has been in line with the industry. It seems that many are expecting the mediocre revenue performance to persist, which has held the P/S ratio back. If this is the case, then at least existing shareholders won't be losing sleep over the current share price.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on a.k.a. Brands Holding.How Is a.k.a. Brands Holding's Revenue Growth Trending?

In order to justify its P/S ratio, a.k.a. Brands Holding would need to produce growth that's similar to the industry.

In order to justify its P/S ratio, a.k.a. Brands Holding would need to produce growth that's similar to the industry.

Retrospectively, the last year delivered a decent 3.3% gain to the company's revenues. The solid recent performance means it was also able to grow revenue by 25% in total over the last three years. Accordingly, shareholders would have probably been satisfied with the medium-term rates of revenue growth.

Looking ahead now, revenue is anticipated to climb by 4.2% during the coming year according to the four analysts following the company. Meanwhile, the rest of the industry is forecast to expand by 4.3%, which is not materially different.

With this information, we can see why a.k.a. Brands Holding is trading at a fairly similar P/S to the industry. Apparently shareholders are comfortable to simply hold on while the company is keeping a low profile.

The Final Word

With its share price dropping off a cliff, the P/S for a.k.a. Brands Holding looks to be in line with the rest of the Specialty Retail industry. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

A a.k.a. Brands Holding's P/S seems about right to us given the knowledge that analysts are forecasting a revenue outlook that is similar to the Specialty Retail industry. At this stage investors feel the potential for an improvement or deterioration in revenue isn't great enough to push P/S in a higher or lower direction. If all things remain constant, the possibility of a drastic share price movement remains fairly remote.

You should always think about risks. Case in point, we've spotted 2 warning signs for a.k.a. Brands Holding you should be aware of, and 1 of them is a bit unpleasant.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.