大摩预计,小米将继续给出“乐观的”三季报,将对小米(01810.HK)的目标价从26港元上调至35港元,按周五收盘价计

大摩预计,小米将继续给出“乐观的”三季报,将对小米(01810.HK)的目标价从26港元上调至35港元,按周五收盘价计Da Ma believes that the market performance of Xiaomi SU7 has exceeded expectations and the strong momentum is expected to continue. The SU7 Ultra has significantly improved the brand image, and the upcoming SUV model will be a major catalyst for performance. At the same time, the price increase of the new smart phone is expected to improve the mid-term profit margin, and the gross margin of the AIoT business is expected to continue to significantly improve. The report has raised the target price of Xiaomi by 35% to 35 Hong Kong dollars, stating that any pullback is a good buying opportunity.

In the second quarter report released in August, Xiaomi's car-making subsidiary delivered the 'best-ever quarterly report', with record high revenue.

On the eve of Xiaomi's third quarter report to be released next Monday, Morgan Stanley issued a report stating: Xiaomi is still the preferred choice, don't exit too early!

Morgan Stanley expects that Xiaomi will continue to provide an 'optimistic' third quarter report, raising the target price for Xiaomi (01810.HK) from HK$26 to HK$35, based on Friday's closing price. This implies that Xiaomi's stock still has a 25% upside potential, and the upcoming SUV model is expected to be a significant catalyst.

Morgan Stanley expects that Xiaomi will continue to provide an 'optimistic' third quarter report, raising the target price for Xiaomi (01810.HK) from HK$26 to HK$35, based on Friday's closing price. This implies that Xiaomi's stock still has a 25% upside potential, and the upcoming SUV model is expected to be a significant catalyst.

In terms of financial performance, Morgan Stanley predicts that Xiaomi's earnings per share (EPS) in 2024 will reach 0.88 yuan, and will reach 0.98 and 1.09 yuan in the following years.

Morgan Stanley: Any pullback is a 'good buying opportunity'!

In the financial report, Morgan Stanley maintains a 'buy' rating on Xiaomi, believing that any pullback may be a good buying opportunity for long-term investors.

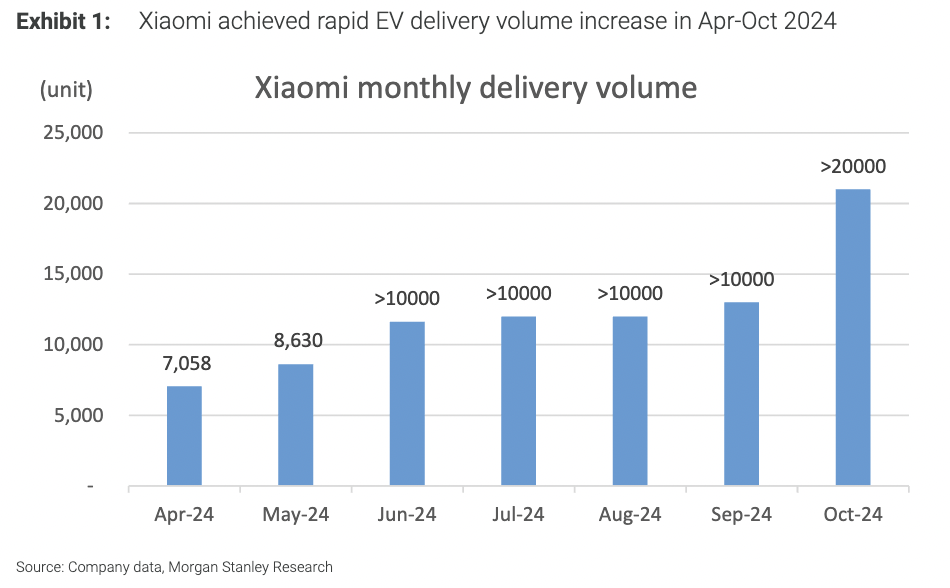

Regarding the electric vehicle business, the research report points out that Xiaomi's electric car shipments in October exceeded 0.02 million units, marking a significant milestone in the company's production capacity improvement.

At the same time, with the continuous growth of orders for the Xiaomi SU7 model, resulting in backlog orders exceeding expectations, delivery waiting time exceeding 20 weeks, indicating that strong sales momentum will continue.

Currently, Xiaomi is expanding its distribution and service network, and starting the construction of the second electric vehicle factory, which will help increase income and enhance economies of scale.

In addition, Morgan Stanley also stated that for the newly launched SU7 Ultra, although it is not expected to be a significant driver of sales, it significantly improves the brand image.

The report indicates that although the pricing of this model is high, market response remains very enthusiastic: Xiaomi SU7 Ultra pre-sale price of 0.8149 million yuan, bookings opened for 10 minutes, and the milestone of 3680 units was reached.

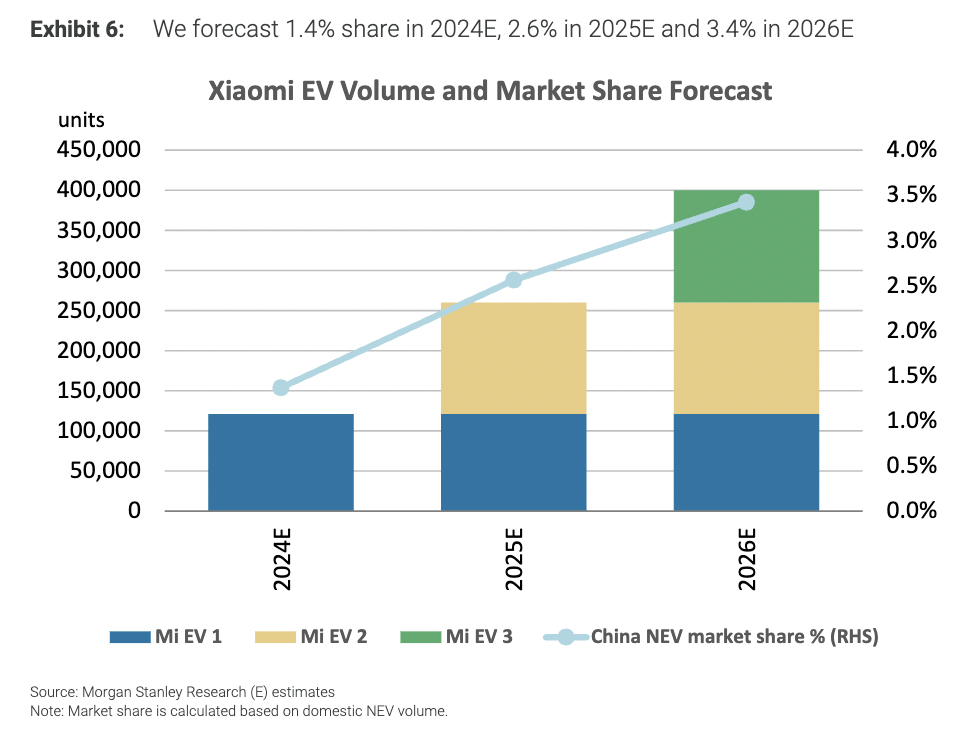

Taking into account the above factors, Morgan Stanley has raised its annual sales expectations for Xiaomi automobiles from 0.23 million-0.25 million units to 0.26 million-0.4 million units, maintaining the gross margin expectations unchanged. It is expected that the accumulated automobile gross profit from 2024 to 2026 will increase from 34.9 billion yuan to 39.3 billion yuan.

It is expected that after the launch of the second electric SUV, Xiaomi's market share in the electric vehicle market will reach 2.6% in 2025 and 3.4% in 2026.

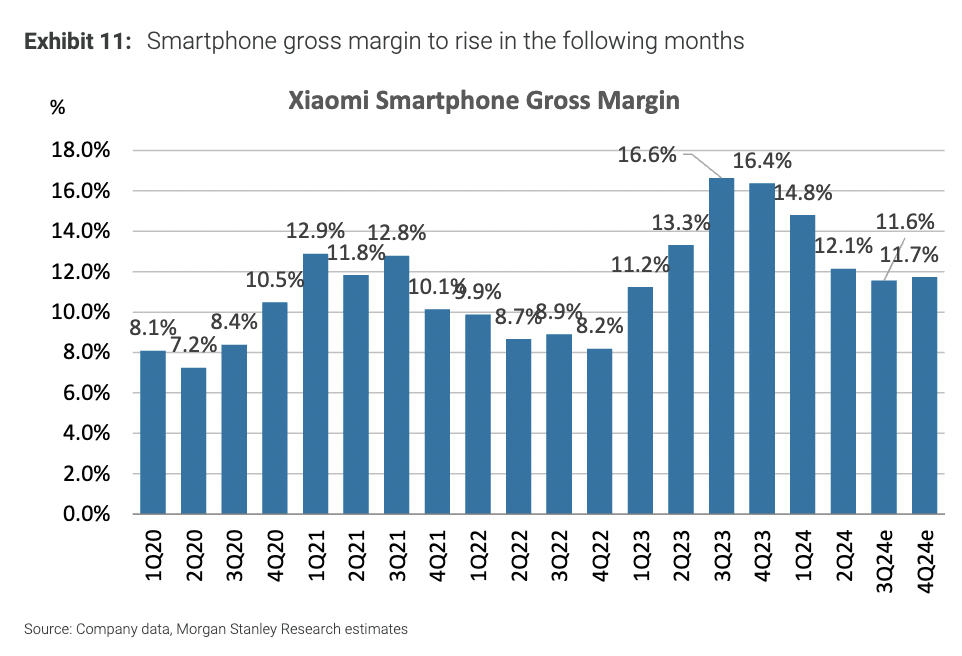

In terms of smart phone business, the report suggests that although Xiaomi's new smart phone pricing has increased, sales momentum remains strong. Morgan Stanley found through the supply chain inspection that orders for models like Xiaomi 15 continue to increase.

Morgan Stanley believes that the increase in average selling price helps offset component costs, which is favorable for profit margins in the next 6-12 months; if component costs decrease in 2025, it may bring a pleasant surprise to gross margin.

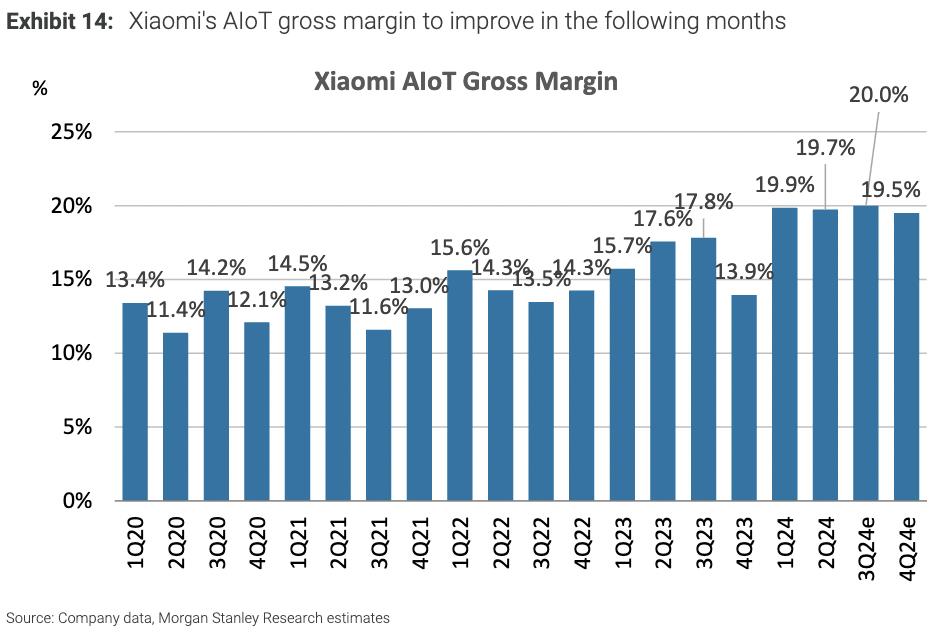

Regarding AIoT business, the report indicates that the second quarter's market performance of AIoT business was outstanding, with significant growth in shipments of tablets, air conditioners, refrigerators, and washing machines. Data shows that Xiaomi's AIoT gross margin has increased from 13-15% to 19-20% in the past few quarters.

Morgan Stanley predicts that with product portfolio optimization and cost synergies, AIoT's gross margin is expected to continue to improve.