对于这份增收不增利的“成绩单”,有投资者在业绩说明会上直言,“公司今年业绩预估表现如何?”而公司高管却并未正面回应,仅表示有关公司2024年年度业绩情况请关注公司后续披露的有关业绩相关的临时公告及年度报告。

对于这份增收不增利的“成绩单”,有投资者在业绩说明会上直言,“公司今年业绩预估表现如何?”而公司高管却并未正面回应,仅表示有关公司2024年年度业绩情况请关注公司后续披露的有关业绩相关的临时公告及年度报告。

Image Source: Visual China Group

On November 15, Blue Whale News reported (Journalist Zhai Zhichao) that recently, "the first domestic EDA stock" Geling Electronics (688206.SH) held a performance briefing for the third quarter of 2024.

According to the financial report, the company's operating revenue for the first three quarters was 0.279 billion yuan, an increase of 25.74% year-on-year; the net income attributable to the parent company was -57.1647 million yuan, a decrease of 99.34% year-on-year; the net income attributable to the parent company after deducting non-recurring gains and losses was -43.37 million yuan, a decrease of 18.75% year-on-year.

Regarding this "report card" of increased revenue but decreased profits, an investor stated directly at the performance briefing, "How is the company's performance forecast for this year?" However, the company executives did not respond directly, only indicating that for information about the company's annual performance in 2024, please pay attention to subsequent disclosures of relevant performance interim announcements and annual reports.

Regarding this "report card" of increased revenue but decreased profits, an investor stated directly at the performance briefing, "How is the company's performance forecast for this year?" However, the company executives did not respond directly, only indicating that for information about the company's annual performance in 2024, please pay attention to subsequent disclosures of relevant performance interim announcements and annual reports.

Blue Whale News reporters noted that when looking at a longer time frame, the company began incurring losses in 2023, and the difficulty in profitability may be related to excessively high expense expenditures. It is understood that in the third quarter of this year, the company's research and development investment was 0.198 billion yuan, an increase of 32.54% year-on-year, accounting for as much as 71.12% of operating revenue. However, despite such R&D spending, the transformation of R&D outcomes is not significant.

A gross margin of over 90% but difficult to achieve profitability.

Gurun Electronics belongs to the EDA industry, which stands for Electronic Design Automation, an essential tool for designing large-scale integrated circuits, hence also known as the "mother of chips".

In December 2021, the company was listed on the star, with its main businesses primarily including EDA tool licensing, sales of semiconductor device characteristic testing instruments, and semiconductor engineering. Due to the listing occurring earlier than its peers, Huada Jiutian (301269.SZ) and Guangliwei (301095.SZ), it has been referred to by the market as the "first domestic EDA stock."

However, data shows that from 2020 to 2023, the company's revenue was 0.137 billion yuan, 0.194 billion yuan, 0.279 billion yuan, and 0.329 billion yuan respectively; the net income attributable to shareholders was 0.029 billion yuan, 0.029 billion yuan, 0.045 billion yuan, and -0.056 billion yuan.

At the same time, nearly half of the company's current revenue consists of accounts receivable. As of the end of the third quarter, the amount of accounts receivable was 0.124 billion yuan, accounting for about 45% of revenue. Market analysts have pointed out that a high proportion of accounts receivable to revenue can easily increase the company's financial pressure and bad debt risk.

It is understood that in the semiconductor industry, EDA tools play a crucial role in chip design and manufacturing, with very high technical requirements. The company's products have advantages in performance and functionality, thus achieving a higher gross margin. According to the third quarter report, the company's sales gross margin is 90.26%.

So, under such a gross margin, why is the company still struggling to be profitable? This may be related to excessively high costs. In the first three quarters of 2024, the company's R&D investment was 0.198 billion yuan, while the revenue during the same period was 0.279 billion yuan, leading to an R&D investment ratio of 71.12% relative to revenue. Additionally, the company's three expenses are also increasing. Data shows that the total sales, management, and financial expenses for the first three quarters were 99.554 million yuan, accounting for 35.66% of revenue, a year-on-year increase of 14.43%.

According to the third quarter report, the company's net margin is -20.67%, down 20.70 percentage points from the same period last year.

High R&D investment has not led to significant results.

It is understood that EDA plays an indispensable important role in chip design, positioned at the very top of the integrated circuit industry, characterized by high technical content and dense intellectual property.

As a highly influential player in the industry, GeLun Electronics understands its path well and has invested significantly in research and development in recent years. From 2021 to 2023, the company's R&D expenditure was 0.079 billion yuan, 0.14 billion yuan, and 0.234 billion yuan, which accounted for 40.99%, 50.21%, and 71.12% of revenue, respectively.

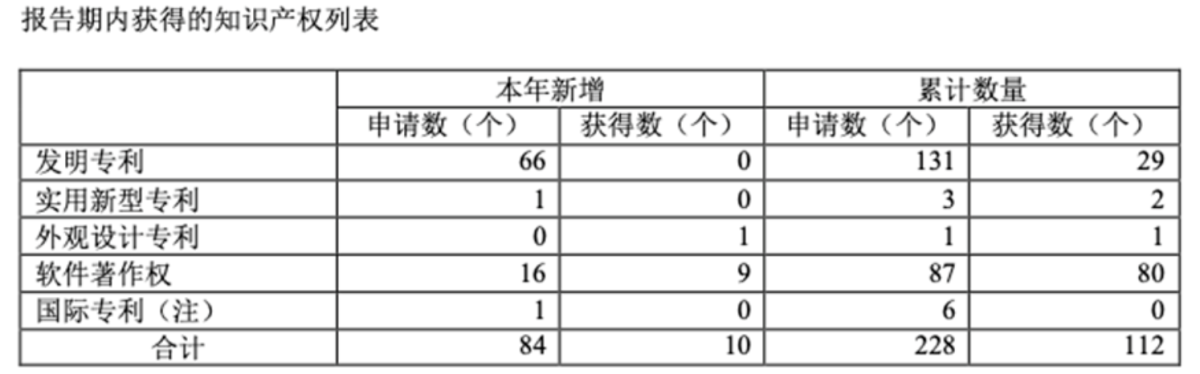

Although the company's R&D investment is high, the increase in the number of intellectual property achievements is not significant. The 2023 annual report shows that the company obtained only one "design patent" and nine "software copyrights," which does not show significant progress compared to the past.

Source: 2023 annual report

Image Source: Internet

Regarding the above statements, a reporter from Blue Whale News contacted Guangli Micro Consulting, and the staff member said that the number of patents can reflect the company's strength to a certain extent, but it also depends on the quality of those patents.

Additionally, compared to Huada Jiutian and Guangliwei, the company's advantages in intellectual property are not obvious. As of August 30, 2024, Gyrun Electronics has a total of 29 invention patents and 87 software copyrights globally, totaling 116 valid intellectual property rights; as of September 18, 2024, Guangliwei's number of patents has reached 160.

Source: Huada Jiutian 2023 annual report.

More critically, in the face of such substantial research and development investment, the company openly acknowledges the risk of research and development results not gaining market recognition, leading to an inability to achieve scalable sales. The company states that due to the critical role of EDA tools in the integrated circuit industry, the EDA industry is characterized by difficult product validation and high market entry barriers, especially for internationally renowned clients, who have high validation and recognition requirements for new companies and new products.