有经济学家表示,未经通胀调整的零售销售额持续超预期增长,很大程度上显示出“粘性通胀”促使消费者们需要用更多的钱买相同的东西,既反映出韧性十足的消费者支出支撑下美国经济“软着陆”愈发明朗,也在一定程度上反映出“再通胀”苗头,毕竟未剔除通胀带来的影响。

有经济学家表示,未经通胀调整的零售销售额持续超预期增长,很大程度上显示出“粘性通胀”促使消费者们需要用更多的钱买相同的东西,既反映出韧性十足的消费者支出支撑下美国经济“软着陆”愈发明朗,也在一定程度上反映出“再通胀”苗头,毕竟未剔除通胀带来的影响。After the retail sales figures without adjustment for inflation were revised upwards by 0.8% in September, they increased by 0.4% in October, exceeding the general expectations of economists.

According to the Securities Times app, U.S. retail sales, dubbed as "terrifying data," indicate that American consumer spending remains resilient. In October, U.S. retail sales continued to exceed expectations, mainly driven by auto sales. Other categories of sales also showed acceleration as American consumers entered the holiday season. October U.S. retail sales showed strong consumer spending, a core support of the U.S. economy. However, it also indicated a rising trend in inflation, leading to a significant cooling of rate cut expectations for the Fed in December and 2025 in the bond market after the retail data was released.

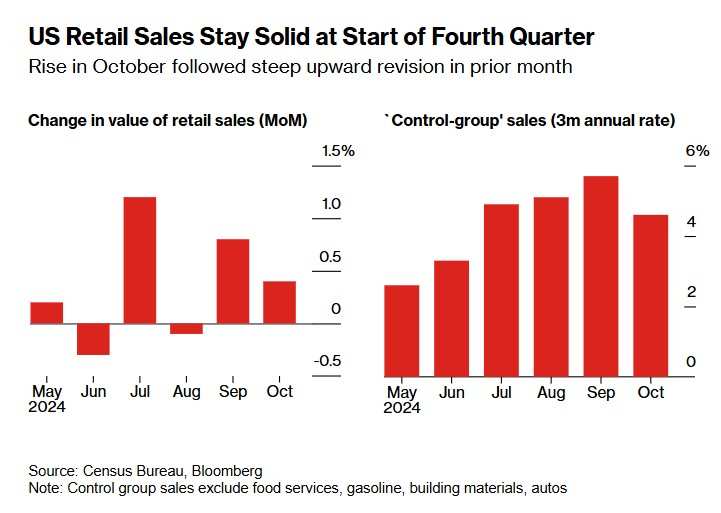

The latest data released by the U.S. Department of Commerce on Friday showed that after the retail sales figures without adjustment for inflation were revised upwards by 0.8% in September, they increased by 0.4% in October, surpassing the general expectations of economists. Excluding auto sales, retail sales increased by a marginal 0.1%.

Some economists suggest that the continuous better-than-expected growth of retail sales without adjustment for inflation largely reflects the phenomenon of "sticky inflation," where consumers need to spend more money to purchase the same goods. This reflects the resilience of consumer spending supporting the "soft landing" of the U.S. economy and also indicates some signs of "reinflation," as the impact of inflation is not excluded.

Some economists suggest that the continuous better-than-expected growth of retail sales without adjustment for inflation largely reflects the phenomenon of "sticky inflation," where consumers need to spend more money to purchase the same goods. This reflects the resilience of consumer spending supporting the "soft landing" of the U.S. economy and also indicates some signs of "reinflation," as the impact of inflation is not excluded.

In the U.S. bond market, traders have already begun pricing in expectations of "reinflation." They anticipate that persistent sticky inflation and a series of policies under the Trump administration, including tax cuts, immigration crackdowns, and tariffs, known as the "MAGA policies," may turn "reinflation" into a reality. The 10-year U.S. Treasury yield may even approach 5%, potentially affecting stock and other risk assets.

Reportedly, among the 13 categories in the retail report, 8 categories saw growth, with the most significant increase in retail sales coming from electronics and appliance stores. Auto sales saw the largest increase in three months. The growth rate in e-commerce sales was moderate, possibly reflecting discount activities during Amazon Prime Day, as well as similar scale promotions by retail giants like Walmart and Target.

The good news is that the U.S. economy remains resilient, but the bad news is that "reinflation" seems to be looming closer.

The September retail sales data, which exceeded expectations, indicates that even with rising inflation, American consumers have shown strong resilience in their spending over the last few months of the year, which may suggest a very stable consumer performance during this year's holiday shopping season in the USA.

However, the concerning news is that the inflation rate, especially core inflation excluding energy and food prices, remains high. Some large retailers have already started considering larger price increases as they anticipate that import tariffs on goods will increase under the leadership of elected President Donald Trump, leading to a sharp decrease in the quantity of goods sold in the market and therefore prices are expected to continue to rise.

The data shows that the so-called control group sales – a measurement that includes the government's estimate of US commodity spending in GDP – unexpectedly dropped by 0.1% in October, the most significant decline since the beginning of 2023 after the largest increase. This indicator excludes food services, car dealers/auto retailers, building materials stores, and gas stations.

However, over the past three months, annualized sales of the control group have unexpectedly increased by 4.6% year-on-year, indicating a strong start to the US economy at the end of the year following strong growth in the third quarter. However, the potential continuous rise in core inflation may present an unfavorable trend, possibly continuing to suppress expectations of a rate cut by the Federal Reserve.

Combining the upward trend inflation data released earlier this week, these data may lead Federal Reserve officials to proceed cautiously with further interest rate cuts. Federal Reserve Chairman Jerome Powell stated at an event on Thursday that the recent performance of the US economy has been 'very good,' potentially prompting policymakers to proceed with interest rate cuts more cautiously.

Following the data release, the yield on 10-year US Treasury bonds rose significantly, while the three major US equity index futures continued to weaken.

Some economists believe that while retail data is strong, the outlook for retailers remains challenging because after experiencing years of high stock prices, prices are still rising, although not as dramatically as in 2022; furthermore, current forecasts suggest that the consumer group with medium to low incomes may have slightly constrained spending compared to last year's holiday shopping season. Additionally, the calendar effect of fewer shopping days between Thanksgiving and Christmas this year is expected to have a negative impact on sales.

Economists will closely monitor the sales on 'Black Friday' and 'Cyber Monday' to understand consumer interest in the American holiday shopping frenzy. Next week, Walmart and Target's financial reports will also help guide the market's outlook on American consumption and inflation.

Before the announcement of October retail sales, the overall CPI in the United States in October increased by 0.24% (expected 0.20%), and the core CPI recorded 0.28% (expected 0.30%), basically meeting expectations; the total overall CPI in October has maintained at 0.2% level for four consecutive months, and the core CPI has also remained at 0.3% level for three consecutive months. From a structural perspective, the rebound of housing inflation and the relative stability of other core service items all indicate that the momentum of inflation is still continuing to rise. These are significant signs of a 're-inflation,' with the risk of inflation rising far greater than the downside risk. More importantly, Trump's 'MAGA policy expectations' will further catalyze expectations of inflation uptrend.

Expectations of a substantial decrease in Fed interest rate cuts, with some traders even betting on a pause in rate cuts in December.

Fed Governor Adrienne Kugler stated that policymakers must simultaneously focus on the central bank's inflation and employment goals, pointing out that the labor market is cooling, and progress towards the Fed's 2% inflation goal is slowing. Kugler said on Thursday: 'The trends of monetary tightening and cooling labor market continue but are slowing, meaning we need to continue to focus on the two aspects of our task.'

Minneapolis Fed President Kashkari, who has taken a hawkish stance since 2023, warned in a recent interview that if inflation unexpectedly rises before December, it could lead the Fed to pause rate cuts.

In a recent statement, FOMC voter and St. Louis Fed President Musallam said, 'Recent information indicates that inflation may be leveling off on a downward trajectory, and the risk of it even rising has increased. Data shows the economy is 'stronger than before, even possibly much stronger,' and several core inflation indicators have 'slightly increased.'

Fed Chair Powell said on Thursday that the strong growth of the US economy allows policymakers to be patient in determining the extent and pace of rate cuts. Powell said in a speech to business leaders in Dallas: 'The economy has not sent any signals that we need to cut rates urgently. The current strong performance of the economy allows us to make decisions more cautiously.' 'We are getting closer to our 2% long-term inflation target, but we haven't reached it yet. We are committed to completing this task,' Powell said. He also mentioned that the process of achieving this goal may 'occasionally encounter some setbacks.'

The CPI and PPI data released this week both show that US inflation is sticky and showing signs of heating up, prompting rate futures traders to significantly reduce their expectations for the Fed's rate cuts in December and next year. The 'CME Fed Watch Tool' shows that after the release of rising CPI, PPI, and strong retail sales data, the probability of a Fed pause in rate cuts in December has increased from less than 30% to close to 40%, and bets on the Fed cutting rates only twice next year, rather than the previously expected 4 cuts before this week's inflation and retail data came out.

David Kelly, Chief Global Strategist at JPMorgan Asset Management, warned earlier this week that if Trump wins the US election, the Fed may even pause its rate easing cycle as early as December. Following Trump's announcement of winning the presidential election, economists from Nomura now predict that the Fed will only cut rates once in 2025, compared to their previous forecast of 4 rate cuts in 2025.