Mawson Infrastructure Group Inc. (NASDAQ:MIGI) shares have had a really impressive month, gaining 46% after a shaky period beforehand. The annual gain comes to 250% following the latest surge, making investors sit up and take notice.

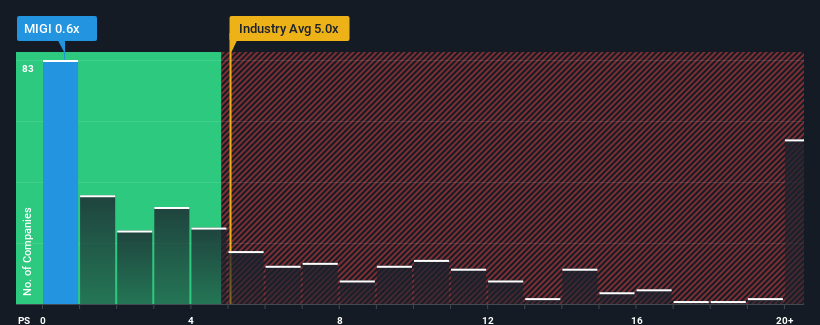

Even after such a large jump in price, Mawson Infrastructure Group's price-to-sales (or "P/S") ratio of 0.6x might still make it look like a strong buy right now compared to the wider Software industry in the United States, where around half of the companies have P/S ratios above 5x and even P/S above 13x are quite common. However, the P/S might be quite low for a reason and it requires further investigation to determine if it's justified.

What Does Mawson Infrastructure Group's P/S Mean For Shareholders?

As an illustration, revenue has deteriorated at Mawson Infrastructure Group over the last year, which is not ideal at all. Perhaps the market believes the recent revenue performance isn't good enough to keep up the industry, causing the P/S ratio to suffer. Those who are bullish on Mawson Infrastructure Group will be hoping that this isn't the case so that they can pick up the stock at a lower valuation.

Although there are no analyst estimates available for Mawson Infrastructure Group, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.Is There Any Revenue Growth Forecasted For Mawson Infrastructure Group?

In order to justify its P/S ratio, Mawson Infrastructure Group would need to produce anemic growth that's substantially trailing the industry.

In order to justify its P/S ratio, Mawson Infrastructure Group would need to produce anemic growth that's substantially trailing the industry.

Retrospectively, the last year delivered a frustrating 9.7% decrease to the company's top line. Still, the latest three year period has seen an excellent 267% overall rise in revenue, in spite of its unsatisfying short-term performance. Accordingly, while they would have preferred to keep the run going, shareholders would definitely welcome the medium-term rates of revenue growth.

Comparing that to the industry, which is only predicted to deliver 25% growth in the next 12 months, the company's momentum is stronger based on recent medium-term annualised revenue results.

In light of this, it's peculiar that Mawson Infrastructure Group's P/S sits below the majority of other companies. It looks like most investors are not convinced the company can maintain its recent growth rates.

The Key Takeaway

Even after such a strong price move, Mawson Infrastructure Group's P/S still trails the rest of the industry. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

We're very surprised to see Mawson Infrastructure Group currently trading on a much lower than expected P/S since its recent three-year growth is higher than the wider industry forecast. Potential investors that are sceptical over continued revenue performance may be preventing the P/S ratio from matching previous strong performance. It appears many are indeed anticipating revenue instability, because the persistence of these recent medium-term conditions would normally provide a boost to the share price.

You need to take note of risks, for example - Mawson Infrastructure Group has 5 warning signs (and 2 which are a bit unpleasant) we think you should know about.

If you're unsure about the strength of Mawson Infrastructure Group's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.