“川普2.0”之际,管理着5650亿美元资产的基金经理们像上次一样,真刀真枪地投入“特朗普交易”,看好美元、美股和小盘股等。

“川普2.0”之际,管理着5650亿美元资产的基金经理们像上次一样,真刀真枪地投入“特朗普交易”,看好美元、美股和小盘股等。Source: Wall Street See

After Trump's election victory, the US dollar, US stocks, and small cap stocks usually tend to strengthen. However, during Trump 1.0, from 2016 to 2020, the US dollar and small cap stocks performed poorly, failing to rise as expected, while the rise in US stocks was mostly attributable to the strength of technology stocks. Analysis suggests that the 'Trump trade' is not the same as 'Trump investment', it is more of a short-term market reaction rather than a long-term trend.

History always repeats itself. Whether in 2016 or 2024, after Trump's victory, the market often exhibits a subconscious "knee-jerk reaction": the performance of US stocks and the US dollar will generally be stronger than other assets.

At the "Trump 2.0" moment, fund managers overseeing $565 billion in assets are once again actively engaging in the "Trump trade," bullish on the US dollar, US stocks, and small-cap stocks.

At the "Trump 2.0" moment, fund managers overseeing $565 billion in assets are once again actively engaging in the "Trump trade," bullish on the US dollar, US stocks, and small-cap stocks.

However, an article by Sherwood News on November 13 raised the point that the "Trump trade" is more about the immediate market reaction after Trump's victory, rather than a sustainable, long-term investment strategy, not equivalent to "Trump investment." But looking back at the four years of "Trump 1.0" (2016 to 2020), US small-cap stocks, the US dollar, and other assets performed poorly and did not rise as expected.

Currently, the market still has a bullish view on the "Trump trade." But as for the subsequent development of the market, will it reverse again like in the "Trump 1.0" era?

"Version 1.0" of the "Trump trade" ended in overall failure.

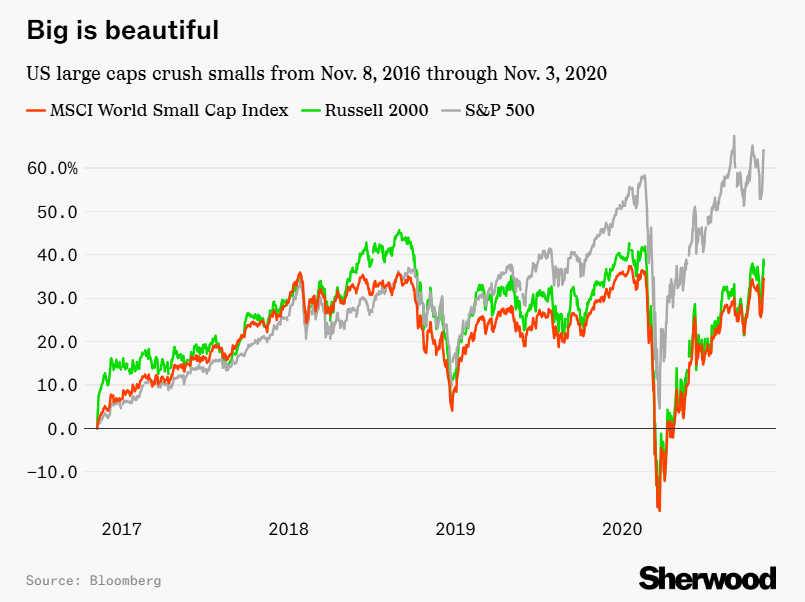

In 2016, US small-cap stocks led the way with a 10% advantage over large caps one month after Trump's unexpected victory.

As the time span lengthens, US small cap stocks significantly underperformed large cap stocks (s&p 500) by more than 20% from 2016 to the 2020 US presidential election date. Despite Trump's tax reduction policy benefiting domestic US companies, small cap stocks' response was relatively muted, performing even worse than small cap stocks in other developed markets.

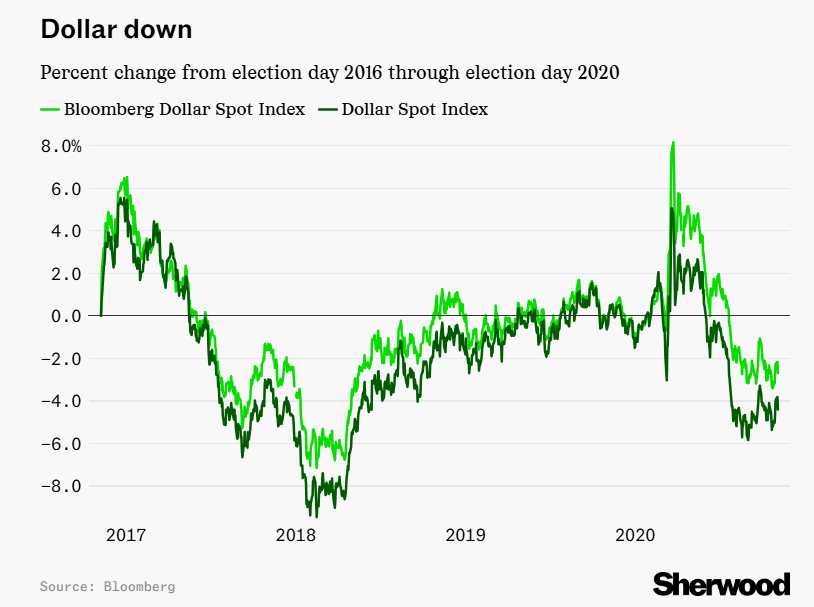

From 2016 to 2020, the US dollar did not perform strongly under the push of the 'Trump trade.' Both the US dollar index and the Bloomberg Dollar Index, including emerging market currencies, experienced declines, contradicting the market's initial expectations.

Next, the US stock market. The article points out that US stocks did indeed outperform the MSCI Global Market Index after Trump's victory, but such performance was also seen when Biden won and during Obama's two terms. The main contributor to the US stock market rise was not the 'Trump trade,' but rather the 'technology stock trade.'

The main factor behind the rise in US stocks was not the 'Trump trade,' but rather the 'technology stock trade.'

In contrast, the strength of the US stock market performance is more attributed to the leadership of technology stocks, especially the strong growth of the s&p 500 index and the nasdaq 100 index. The profitability of tech giants is the main reason why the US stock market has long outperformed global markets, driven more by technological innovation and global expansion rather than Trump's policy push. Even though Trump's tax reform helped enhance corporate profits, tech giants were not its main beneficiaries.

The 'Trump trade' returned in 2024, but this does not equate to 'Trump investment.'

In 2024, fund managers overseeing $565 billion in assets are reinvesting in 'trades' related to Trump – those popular trading strategies when Trump was elected in 2016, such as being bullish on the US stock market, the US dollar, and small cap stocks.

A survey by Bank of America's global fund managers reflects the change in investor views after the US election results were announced. Currently, the surveyed fund managers still favor the 'Trump trade,' believing that the US stock market remains the top choice for the 2025 market.

Meanwhile, they consider the US dollar to be the best-performing currency in the forex market.

However, the article points out that the 'Trump trade' should be called 'Trump reaction trades' instead of 'Trump investment'.

Although Trump's election typically triggers a series of reactions in the market, including the strong performance of the US dollar and small cap stocks, these 'Trump trades' are not long-term investment strategies but rely more on the short-term market sentiment following Trump's victory.

The current situation is similar to that of 2016, but can the market reactions in 2024 be sustained?

Editor / jayden