The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Aldeyra Therapeutics, Inc. (NASDAQ:ALDX) does carry debt. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we think about a company's use of debt, we first look at cash and debt together.

How Much Debt Does Aldeyra Therapeutics Carry?

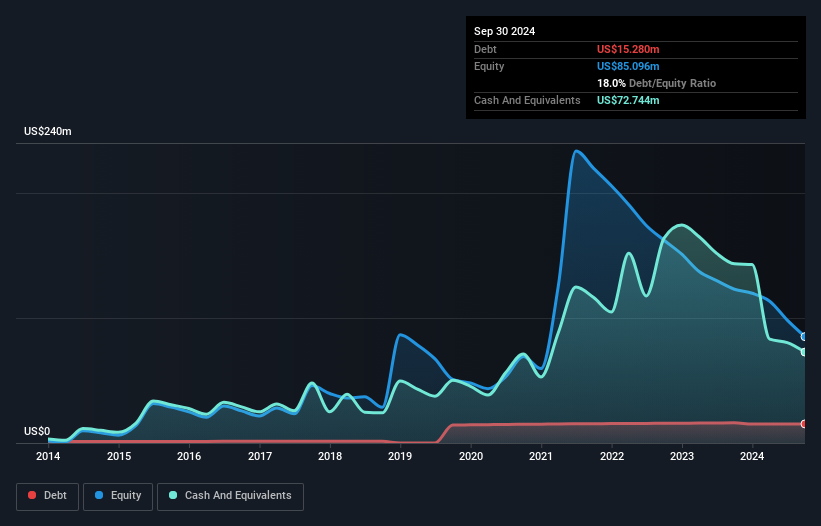

The image below, which you can click on for greater detail, shows that Aldeyra Therapeutics had debt of US$15.3m at the end of September 2024, a reduction from US$16.1m over a year. But on the other hand it also has US$72.7m in cash, leading to a US$57.5m net cash position.

A Look At Aldeyra Therapeutics' Liabilities

Zooming in on the latest balance sheet data, we can see that Aldeyra Therapeutics had liabilities of US$17.2m due within 12 months and liabilities of US$15.1m due beyond that. Offsetting this, it had US$72.7m in cash and US$40.0m in receivables that were due within 12 months. So it can boast US$80.5m more liquid assets than total liabilities.

Zooming in on the latest balance sheet data, we can see that Aldeyra Therapeutics had liabilities of US$17.2m due within 12 months and liabilities of US$15.1m due beyond that. Offsetting this, it had US$72.7m in cash and US$40.0m in receivables that were due within 12 months. So it can boast US$80.5m more liquid assets than total liabilities.

It's good to see that Aldeyra Therapeutics has plenty of liquidity on its balance sheet, suggesting conservative management of liabilities. Given it has easily adequate short term liquidity, we don't think it will have any issues with its lenders. Simply put, the fact that Aldeyra Therapeutics has more cash than debt is arguably a good indication that it can manage its debt safely. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Aldeyra Therapeutics can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Given its lack of meaningful operating revenue, Aldeyra Therapeutics shareholders no doubt hope it can fund itself until it has a profitable product.

So How Risky Is Aldeyra Therapeutics?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And we do note that Aldeyra Therapeutics had an earnings before interest and tax (EBIT) loss, over the last year. And over the same period it saw negative free cash outflow of US$31m and booked a US$45m accounting loss. But at least it has US$57.5m on the balance sheet to spend on growth, near-term. Overall, its balance sheet doesn't seem overly risky, at the moment, but we're always cautious until we see the positive free cash flow. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. We've identified 1 warning sign with Aldeyra Therapeutics , and understanding them should be part of your investment process.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.