① Last night's U.S. October CPI data, which fully met market expectations, did not create significant waves in the market; ② However, the data still boosted market confidence in the Fed's potential interest rate cut next month and stimulated a rebound in short-term U.S. treasury notes.

According to the financial community on November 14 (edited by Xiaoxiang), Wednesday's U.S. October CPI data, which fully met market expectations, did not create significant waves in the financial market. However, the data still boosted market confidence in the Fed's potential interest rate cut next month and stimulated a rebound in short-term U.S. treasury notes.

Market data shows that the latest bids drove the two-year U.S. treasury yield down by about 6 basis points on Wednesday, to 4.296%. Compared to long-term treasury bonds, the two-year treasury bonds have a closer relationship with the Fed's interest rate decisions.

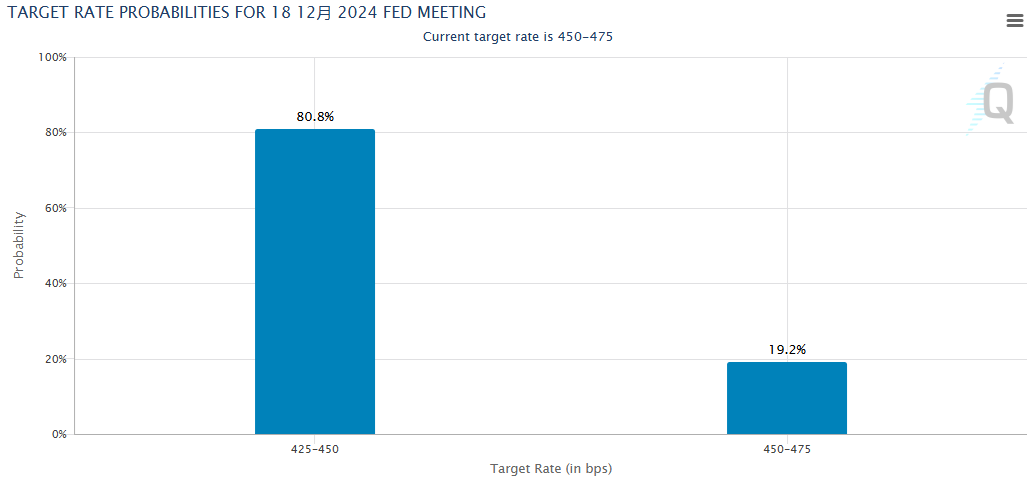

Interest rate market traders have currently increased the expected probability of the Fed cutting rates again on December 18 from about 58% earlier on Wednesday to about 80%.

Interest rate market traders have currently increased the expected probability of the Fed cutting rates again on December 18 from about 58% earlier on Wednesday to about 80%.

Although the U.S. Labor Department's CPI data for October announced that day only met expectations, this performance still somewhat relieved concerns about inflation prospects following Trump's election victory. Over the weeks surrounding the election on November 5, bond traders had significantly lowered their expectations for further interest rate cuts by the Fed within the next year.

Lindsay Rosner, head of multi-industry fixed income investments at Goldman Sachs Asset Management, stated, "The core inflation rate remains stable, making it likely for the Fed to cut rates in December. After a series of unusual fall data, today's data has eased concerns about a potential slowdown in the pace of interest rate cuts."

The U.S. Labor Department's data released on Wednesday showed that October CPI rose 2.6% year-on-year, meeting market expectations, although it rebounded from 2.4% last month, halting a six-month decline in CPI; core CPI remained at 3.3%, the same as September. After the data was released, National Economic Council Director Brainard issued a statement saying that the October CPI data is close to pre-pandemic levels. The Biden administration will continue to work to reduce key household expenses such as housing and medical costs while opposing policies that would undermine the process of lowering inflation.

Rick Rieder, Chief Investment Officer of BlackRock Global Fixed Income, wrote in an email, "Overall, the report did not exceed the range that the Fed considers roughly in line with its inflation target. However, in some industries, the rate of (improvement in inflation) changes has clearly slowed down."

He believes that the market always seems to react to CPI data, and there may be sharper observations today, but we think a quick glance at the calendar indicates that core CPI and core PCE should prompt the Federal Reserve to lower interest rates again at the next meeting, and then interpret the inflation trajectory from there.

Regarding the latest inflation report, well-known Federal Reserve commentator and 'New Federal Reserve News Agency' Nick Timiraos wrote on Wednesday that the latest report may not be sufficient to prevent the Federal Reserve from cutting rates again in December. However, given the previous strong consumer spending and stable hiring, stronger inflation may spark more intense debate among officials at the next meeting about whether to slow the pace of rate cuts at the beginning of next year.

Timiraos wrote that investors' positive reaction to this report may partially be due to comfort over the elected president Trump and the Federal Reserve not immediately clashing. Trump repeatedly called for lower interest rates during his first term. Economists believe some of the policies proposed by Trump, such as increasing tariffs, may drive inflation higher.

Federal Reserve Chair Powell hinted at a press conference last week that the Federal Reserve is prepared to respond to stronger-than-expected data or 'volatility'. However, he believes that some price stickiness reflects lagging effects of previous increases, rather than new sources of price pressure. For example, overall rents continue to rise at historical highs under the influence of the CPI, but the rate of rent increases for new leases has been modest for over a year.

'This is just a catching-up issue. It doesn't truly reflect current inflation pressure. It reflects past inflation pressures,' Powell stated at the time, 'Obviously, we haven't declared victory, but we feel that inflation will continue to decline along a bumpy path, which is very much in line with this trend.'

Timiraos also mentioned that if Federal Reserve officials insist on cutting rates in December, the focus may turn to what factors might lead them to slow the pace of rate cuts next year.

In fact, several Federal Reserve officials expressed their views on this on Wednesday. Kansas City Fed President George stated that the Federal Reserve's rate cut actions so far show decision-makers' growing confidence in declining inflation, but the future path of rate cuts remains to be seen. St. Louis Fed President Bullard indicated that the Federal Reserve's inflation and employment targets are achievable, but he emphasized that with price growth still above the Federal Reserve's 2% target, officials should keep policy 'moderately restrictive'.

From the performance of the bond market, the drop in long-term U.S. Treasury yields was relatively small after the CPI data was released, and there was even a rebound in the context of a surge in new corporate bond sales. The yield on 10-year U.S. Treasury notes rose 2.2 basis points to 4.454% at the close, while the yield on 30-year U.S. Treasury notes increased 6.4 basis points to 4.639%.

Market participants indicate that due to the large issuance of csi enterprise bonds on Wednesday, the yields on long-term bonds, led by the indicators of 10-year treasury notes, have risen. Wall Street traders typically prefer to lock in the borrowing costs of the csi enterprise bonds they underwrite. In this process, traders will sell treasury notes, raising their yields as a hedge to secure the borrowing costs of the bond issuance before the transaction completes. Once the bonds are sold, traders will buy treasury notes to exit the 'rate lock.'

Of course, despite the warming expectations of interest rate cuts in December, concerns about the unclear prospects for rate cuts, especially next year, are clearly one of the reasons why long-term u.s. bonds struggle to sustain a rebound.

Rosner from goldman sachs asset management believes that due to the high uncertainty in fiscal and trade policies, with the chill of the new year approaching, the Federal Reserve may choose to slow down the pace of easing.

ClearBridge Investments strategist Josh Jamner pointed out that the CPI data in line with expectations indicates that, despite substantial progress in combating high inflation, the 'last mile' challenges are greater. As inflation remains stable, today’s data will not have a significant impact on market narrative.

However, some industry insiders believe that long-term u.s. bond yields will eventually follow the decline of short-term bond yields.

Stephen Jen, CEO of Eurizon SLJ, stated that the u.s. 10-year treasury notes yield is already too high, and he considers 3.5% to be a reasonable valuation level. He wrote that the impending Trump administration's policies may yield more positive fiscal outcomes than the market currently assumes, thus some typical Trump trades could be shaken.

Editor/Somer