报告写道:

报告写道:Goldman Sachs advises to continue holding the most short-sold stocks until the end of January next year, as a decrease in interest rates, avoidance of an economic recession, resolution of election uncertainties, and Trump's overwhelming victory will create an environment favorable for a rebound driven by 'animal spirits,' which benefits low-quality stocks.

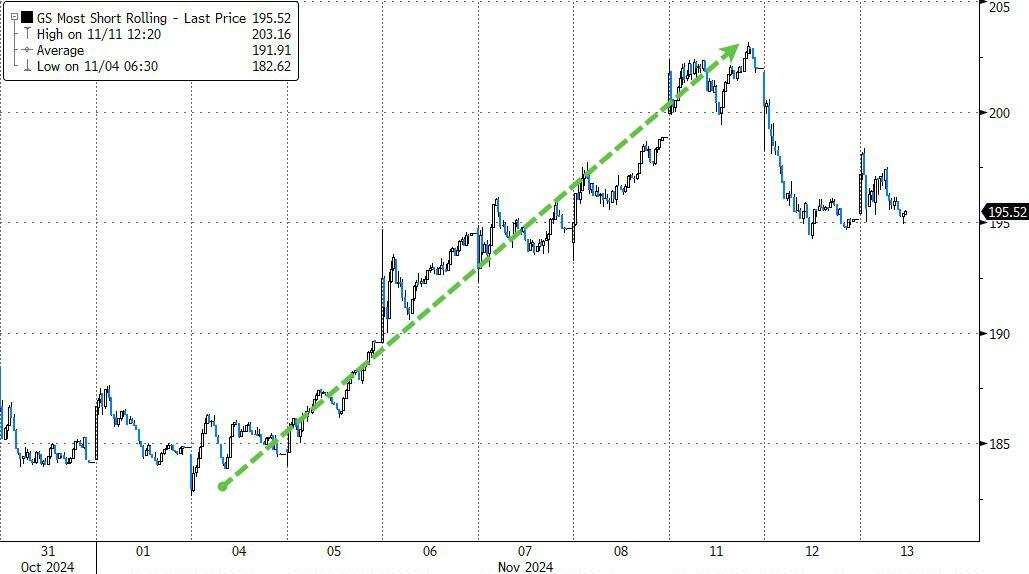

Before Trump's trade pause on Tuesday, as of Monday this week, a basket of the most short-sold stocks tracked by Goldman Sachs had accumulated a rise of over 11% within five trading days. The Goldman Sachs trading department expects this phenomenon of popularity for the most shorted stocks to continue until January next year when Trump is sworn in as president.

A report from Goldman Sachs trader Guillaume Soria states that Goldman Sachs's trading department believes that by the end of this year, the stocks with the highest levels of short selling, as well as lower-quality stocks including high floating rate bonds and low momentum stocks, will face increased risk of repricing.

The report states:

The report states:

"We are entering a pro-cyclical environment (our cyclical stocks combined with defensive stocks achieved the second best performance of all time in a single day), while short-term interest rates are gradually declining."

Goldman Sachs analyzed the returns, beta values, leverage, momentum, dividend yields, and other indicators after the elections of Republican candidates for U.S. president in 2000, 2004, and 2016, and found that the factor returns when Republicans are elected indicate that previously lost investments and high beta stocks will increase in size. High beta stocks often trade well, while large cap stocks have a hit rate of only 100% inferior to small cap stocks, momentum often performs poorly, while value and yields outperform growth.

Therefore, Goldman Sachs recommends continuing to hold the most shorted stocks until the end of January next year, as they anticipate:

Interest rates are lowered,

The usa economy has avoided a recession,

The uncertainty of the election has been eliminated,

Trump's overwhelming victory has brought a rebound driven by 'animal spirits', creating a favorable environment for low quality stocks.

Goldman sachs report pointed out that over the past decade, the low quality stock basket performed best in January, June, and November, with the current November and next January accounting for two of them.

Goldman sachs found that since the large-scale shareholding reduction/replenishment appeared in July of this year, short selling has generally been increasing and has reached a high level since the beginning of the year, leaving room for short covering before the end of the year.

The report mentions that Goldman sachs' high floating rate bond basket has already broken upward compared to the s&p 500 index, breaking a downward trend that lasted for more than four years. The combination of cyclical stocks and defensive stocks has achieved the best performance since 2020. Momentum is entering the worst three-month phase for this indicator in over twenty years: from November to January.

The trading situation of stocks that incurred losses in the past is consistent with those heavily short sold this year, both being impacted by rising long-term interest rates, and now the rise in interest rates should alleviate somewhat.

In addition, Goldman Sachs traders recently predicted that after the trading frenzy driven by the U.S. elections ends, rotation pressure will continue to be a significant feature of the U.S. stock market, as investors shift their funds into small cap stocks and seek opportunities in cyclical/inflation themes. Goldman Sachs trader Mike Washington stated that with the elections, the Federal Reserve, and the Bank of England each lowering rates by 25 basis points, the 10-year U.S. Treasury yield fell by 7 basis points to 4.30% within a week, revealing signs of investor fatigue amid yield fluctuations and the long earnings reporting cycle.

Goldman Sachs strategists continue to favor risk in asset allocation, increasing shareholding in U.S. stocks and high yield bonds while reducing shareholding in Europe. Strategists, including Christian Mueller-Glissmann, wrote in a report on November 11 this Monday,Implied volatilitythe reset suggests that investors should look for specific hedges or options overlays, as a bond sell-off may put pressure on stocks.

Editor/rice