Despite an already strong run, Turning Point Brands, Inc. (NYSE:TPB) shares have been powering on, with a gain of 31% in the last thirty days. The last month tops off a massive increase of 144% in the last year.

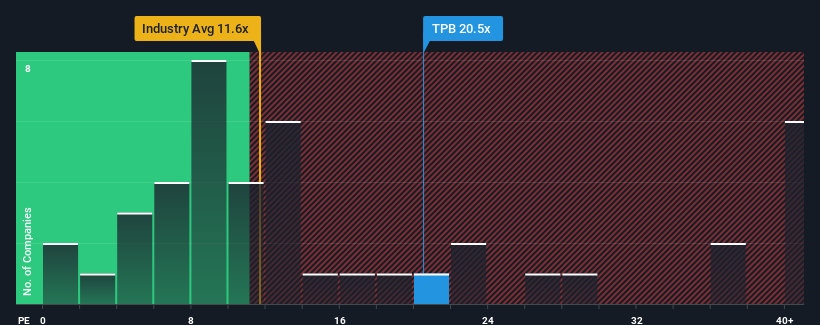

Even after such a large jump in price, it's still not a stretch to say that Turning Point Brands' price-to-earnings (or "P/E") ratio of 20.5x right now seems quite "middle-of-the-road" compared to the market in the United States, where the median P/E ratio is around 19x. While this might not raise any eyebrows, if the P/E ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

Turning Point Brands certainly has been doing a good job lately as it's been growing earnings more than most other companies. It might be that many expect the strong earnings performance to wane, which has kept the P/E from rising. If not, then existing shareholders have reason to be feeling optimistic about the future direction of the share price.

Does Growth Match The P/E?

There's an inherent assumption that a company should be matching the market for P/E ratios like Turning Point Brands' to be considered reasonable.

There's an inherent assumption that a company should be matching the market for P/E ratios like Turning Point Brands' to be considered reasonable.

If we review the last year of earnings growth, the company posted a terrific increase of 292%. Despite this strong recent growth, it's still struggling to catch up as its three-year EPS frustratingly shrank by 7.1% overall. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

Turning to the outlook, the next year should generate growth of 11% as estimated by the three analysts watching the company. With the market predicted to deliver 15% growth , the company is positioned for a weaker earnings result.

In light of this, it's curious that Turning Point Brands' P/E sits in line with the majority of other companies. It seems most investors are ignoring the fairly limited growth expectations and are willing to pay up for exposure to the stock. These shareholders may be setting themselves up for future disappointment if the P/E falls to levels more in line with the growth outlook.

The Bottom Line On Turning Point Brands' P/E

Its shares have lifted substantially and now Turning Point Brands' P/E is also back up to the market median. While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

Our examination of Turning Point Brands' analyst forecasts revealed that its inferior earnings outlook isn't impacting its P/E as much as we would have predicted. When we see a weak earnings outlook with slower than market growth, we suspect the share price is at risk of declining, sending the moderate P/E lower. Unless these conditions improve, it's challenging to accept these prices as being reasonable.

It is also worth noting that we have found 2 warning signs for Turning Point Brands that you need to take into consideration.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with a strong growth track record, trading on a low P/E.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.