成也萧何、败也萧何。

成也萧何、败也萧何。How can we further improve?

After many years of transformation, "Standing firm in the forefront of the retail industry" remains the unfulfilled wish of China Citic Bank (601998.SH) over the years.

In the first three quarters of 2024, China Citic Bank recorded revenues of 162.21 billion RMB and a net profit attributable to shareholders of 51.826 billion RMB. The year-on-year growth rates of the two were 3.83% and 0.76% respectively, highlighting the phenomenon of "increased revenue but not increased profit".

Success has its own causes, and failure has its own causes.

Success has its own causes, and failure has its own causes.

From the perspective of profit composition, the growth in revenue and the stagnation in net profit are closely related to China Citic Bank's retail business, which is considered the main focus of transformation.

In the first three quarters, the year-on-year growth rate of net non-interest income was as high as 11.17%, 10.5 percentage points higher than the interest part, boosting the overall revenue growth by 3.83%.

However, in the first half of the year, retail credit impairment losses increased by 57.65% year-on-year, leading to an overall 2.34% expansion in operating expenses.

China Citic Bank's development of its retail business has a long history.

As early as 2014, China Citic Bank, which has always been famous for its corporate business, has adopted a "light capital" strategy and embarked on a "retail transformation road".

In the following nearly 10 years, the bank's "retail transformation" path has become increasingly clear, and the relationship between corporate, retail, and financial market businesses has evolved from the initial "one core and two wings" with corporate as the core to "all three driving forces".

In 2021, China Citic Bank, whose retail business contributes more than 30% of its pre-tax profit, has set a new goal to "firmly establish itself in the top tier of retail" in 3 years.

The deadline of 3 years has arrived. Looking at the AUM (retail asset management scale) indicators of joint-stock banks, China Citic Bank still has a considerable gap to reach the ideal of the "top tier of retail."

The rapid development of the retail business has not helped China Citic Bank achieve a breakthrough in performance ahead of its peers.

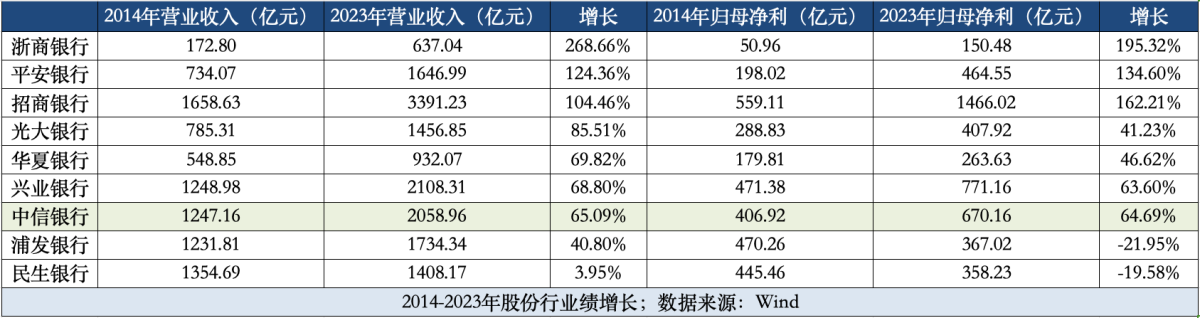

From 2014 to 2023, China Citic Bank's performance has been relatively mediocre, achieving double-digit growth in revenue and net profit only in 2015.

Compared with peer joint-stock banks, over the past decade, China Citic Bank's revenue and profit growth rates have been in the middle of the industry, unable to match institutions like Zhejiang Commercial Bank, Ping An, and CM Bank in achieving "doubling" performance.

Unfinished 'retail expectation'

Vertically speaking, the retail transformation in the past decade has almost reshaped the business structure of the former 'corporate king'.

In 2014, China Citic Bank launched the 'retail strategy secondary transformation,' planning to optimize management mechanisms, branch capacity, and create advantages in retail channels, products, and team systems over a three-year period.

During this period, retail remained a significant 'weakness' in China Citic Bank's business.

In that year's pre-tax profit composition, the proportions of financial markets, corporate, and retail were 57.9%, 46.3%, and 2.4% respectively.

While the revenue share of the retail banking division was nearly 20%, it contributed only 2% of the profit.

The significant weakness spurred the determination for 'retail transformation'.

At that time, China Citic Bank focused on expanding branches and developing new products, establishing a nearly 1500-person retail training team, while aggressively promoting new products such as 'salary pot,' 'mortgage loans,' online loans, credit card loans, and more.

Afterwards, China Citic Bank's 'Retail Road' gradually became more systematic.

From 2015 to 2018, the positioning of the retail business gradually shifted from the 'two wings' in the 'one body and two wings' model to being equal with the core of the 'three-pronged' strategy, alongside corporate business.

By the end of 2018, the bank's pre-tax profit from retail business accounted for an increased proportion of 29%; reaching 34.7% by the end of 2021.

At a key point where profit contribution exceeded 30%, China Citic Bank released the 'New Three-Year Plan' in 2021, proposing wealth management as the pivot point, leveraging 'sector integration, public-private collaboration, and group synergy' to achieve a 'leveraged jump' in retail financial business.

It is within this plan that China Citic Bank explicitly states the goal of 'three years later, the overall scale and strength of the retail business will stand firm in the top echelon of the industry.'

However, after 2021, the rapid growth of the retail business came to a sudden halt.

Although at this point the bank's reform of the retail sector involved organizational changes, management methods, business layout, talent recruitment, and various other aspects, it can be described as a 'systemic reshaping.'

Due to factors such as the impact of the epidemic, slowing consumption, and declining interest rates, the effects of the new round of plans were minimal.

In the first half of 2024, the proportion of China CITIC Bank's retail business profit has dropped from the peak of 34.7% to 6.1%.

However, in vertical comparison, China CITIC Bank's retail channels and products have both made breakthroughs over the past 10 years.

By the end of the first half of 2024, the number of domestic branches has increased by 18.62% compared to the end of 2014, and the monthly active users of the mobile APP are nearly three times the total number of mobile banking customers at the end of 2014.

However, from a horizontal perspective, the bank still struggles to "stand firmly in the first echelon" in the retail business.

In the first half of 2024, the AUM of China CITIC Bank increased by 4.25% from the beginning of the year to 4.42 trillion yuan.

Among joint-stock banks, CM Bank and Industrial Bank continue to lead China CITIC Bank in AUM size; Ping An Bank, which is slightly behind in scale, is also narrowing the gap in scale with the highest interbank growth rate of 6.64%.

How to further advance

Since 2014, after starting the transformation, the growth rate of china citic bank corporation's retail business ranks among the top in joint-stock banks.

However, it has only risen to the "second-tier", always lacking the opportunity to further advance.

Especially after 2021, with fluctuations in household income, slowing consumption, coupled with a downturn in property, asset depreciation, mortgage shrinking... The overall retail growth rate and asset quality of banks are facing some fluctuations.

Against the backdrop of the overall industry slowdown, the rising star of retail represented by china citic bank corporation is also falling behind the "first-tier", widening the gap even further.

The gap is reflected in both quantity and quality dimensions.

One is the business scale and growth rate represented by AUM.

In the first half of 2024, china citic bank corporation's AUM reached 4.42 trillion yuan, ranking at the forefront of the "second-tier" among joint-stock banks; the growth rate reached 4.25%, surpassing industrial bank and shanghai pudong development bank.

However, there is a significant gap in the above two indicators compared to the "first-tier" cm bank.

Second, the poor asset-liability structure and asset quality behind the scale.

For example, in the first half of the year, the personal deposit cost rate of China Citic Bank was 2.29%, while that of CM Bank was only 1.51%; the personal loan non-performing loan ratio of China Citic Bank increased by 0.09 percentage points to 1.3% from the beginning of the year, while that of CM Bank rose by 0.01 percentage points to 0.9%.

Fluctuating asset quality directly affects net profit performance.

In the first half of the year, China Citic Bank's retail business credit impairment losses reached 25.537 billion yuan, accounting for 74.3% of all credit impairment losses, directly causing a 76.21% decline in pre-tax profits of the retail business.

Tang Shuhui, Deputy General Manager of the Risk Management Department of the bank, stated at the performance release conference that the company will vigorously control new and old retail asset quality under pressure.

Tang Shuhui stated, “We are confident in ensuring a stable closure of asset quality.”

Optimizing credit structure and rigorously screening customer access also means that the growth rate of retail credit may face continued pressure.

In the final analysis, China Citic Bank Corporation's "retail transformation" needs to go further, still needing to have a core advantage as a strong point.

Deputy General Manager and Chief Risk Officer Hu Gang shared at the press conference, "Compared with banks of similar size, our unique endowment lies in synergy."

For example, in terms of products, the bank focuses on customer investment and financing, payment settlement needs, providing a continuously enriched private banking product spectrum, while continuously optimizing property mortgage, credit loans and other block product in personal loan business, ultimately optimizing a tiered customer service system for "mass, affluent, VIP, private banking".

However, in the increasingly intense competition, institutions with the "synergy" advantage are by no means only China Citic Bank Corporation.

In the future competition of the retail blue ocean, how can China Citic Bank Corporation expand the "synergy" power, harness the advantages brought by financial control to the extreme, still requires more exploration and change over a longer period of time.