As the first major data after the US election, the US CPI report for October, scheduled to be released at 9:30 pm on Wednesday Beijing time, may obviously have a crucial impact on the future policy path of the Federal Reserve; This also prompts some Wall Street people to start considering whether the next market trading theme will gradually shift from the past week's glamorous 'Trump trade' to a rate-oriented perspective around the Federal Reserve's rate cut process.

Caixin News, November 13th (Editor Xiaoxiang) Before the crucial US inflation report was released, the overnight violent rise in the US stock market finally lost momentum. The panic surrounding the sell-off of US bonds (US bond yields soaring significantly) gradually began to burn towards US stocks, while the Bloomberg US Dollar Index further touched the highest level in two years.

As the first major data after the US election, the US CPI report for October, scheduled to be released at 9:30 pm on Wednesday Beijing time, may obviously have a crucial impact on the future policy path of the Federal Reserve. This also prompts some Wall Street people to start considering whether the next market trading theme will gradually shift from the past week's glamorous 'Trump trade' to a rate-oriented perspective around the Federal Reserve's rate cut process.

The momentum of US stocks has cooled off slightly.

Market data shows that the US stock market collectively fell on Tuesday, and the S&P 500 index ended the previous four trading days of gains. Some popular targets of the 'Trump trade' became one of the most eye-catching losers on Tuesday. Tesla fell by 6.1%, Trump's media and technology group fell by nearly 9%, small cap stocks seen as potential beneficiaries of Trump's re-election generally came under pressure, with the Russell 2000 small-cap index falling by 1.87% to 2389.46 points.

Market data shows that the US stock market collectively fell on Tuesday, and the S&P 500 index ended the previous four trading days of gains. Some popular targets of the 'Trump trade' became one of the most eye-catching losers on Tuesday. Tesla fell by 6.1%, Trump's media and technology group fell by nearly 9%, small cap stocks seen as potential beneficiaries of Trump's re-election generally came under pressure, with the Russell 2000 small-cap index falling by 1.87% to 2389.46 points.

Mark Malek, Chief Investment Officer at Siebert, said that the US stock market may have already risen too much. He believes that the market has now eliminated the uncertainty of pending election results, and some lingering headwinds in the core economy are once again becoming people's focus.

While US stocks softened, the frenzy of selling in the US bond market continued. US Treasury yields rose collectively on Tuesday, as bond investors returned to the market after the long weekend and continued to digest President-elect Trump's tax cuts and trade tariff policies, which are seen as inflationary and could also slow down the pace of interest rate cuts by the Federal Reserve.

The two-year US Treasury yield, sensitive to expectations of US rates, rose to 4.367% at one point on Tuesday, the highest level since July 31. The yield rose by 8.8 basis points at the close, to 4.342%, marking the largest single-day increase since early October. In other tenor varieties, the 10-year US Treasury yield surged by 12.9 basis points to 4.437%. The 30-year US Treasury yield increased by 10.3 basis points to 4.581%.

With the increasingly obvious interest rate advantage brought about by the surge in US bond yields, the US Dollar Index is also climbing further in the forex market. The US Dollar Index, which measures the US dollar against six major currencies, rose 0.51% on Tuesday to 105.96, briefly hitting 106.17 during the session, the highest since early May.

Thierry Albert Wizman, global interest rates and forex strategist at Macquarie in New York, said, "People are still concerned about the inflation outlook under Trump's tariffs and anti-immigration policies. Of course, we will also focus on Wednesday's consumer price index. If people see a CPI higher than expected on Wednesday, coupled with the prospect of tariffs under the Trump administration, you will understand why the bond market has been so tense."

Chris Montagu, a strategist at Citigroup, also pointed out that as investors begin to take profits, the post-election rally in the US stock market may stall.

A critical test is coming tonight.

In fact, with overnight Federal Reserve officials "naming names", inflation data may become a key factor in determining whether to cut interest rates in December. The importance of the US October CPI data tonight has been greatly elevated.

Neel Kashkari, President of the Minneapolis Fed, said on Tuesday that he would focus on the upcoming inflation data to determine whether another rate cut at the Fed's December meeting is appropriate. When asked what factors could lead policymakers to hit the pause button next month, he noted, "Only a significant surprise in inflation could lead to such a significant change in outlook."

"If we see higher-than-expected inflation between now and then, it could make us stand still. It's hard to imagine that the labor market will really heat up between now and December. Time is running out," Kashkari pointed out.

The Federal Reserve cut rates by 25 basis points last Thursday, marking the second consecutive rate cut. While Fed officials' forecasts in September suggested rate cuts of 25 basis points at both the November and December meetings, investors have reduced their bets on a rate cut at the Fed's final meeting this year, given the stalled progress in inflation and strong economic growth.

It is generally expected in the industry that the U.S. CPI for October to be announced tonight is expected to rise by 2.6% year-on-year, up 0.2 percentage points from the previous month of 2.4%, and is expected to remain flat at +0.2% month-on-month; core CPI year-on-year and month-on-month growth rates are expected to remain at 3.3% and 0.3% respectively.

Inflation has now become a major focus issue in this year's U.S. election, with dissatisfaction with the economy and consumer prices seen as one of the key factors driving former President Trump's return to the White House.

Quincy Krosby, Chief Global Strategist at LPL Financial, stated in an interview that inflation data has indeed fallen significantly, but the problem for ordinary consumers is that the prices of many things, such as a pound of chicken breasts in the grocery store, are still higher than they were four or five years ago.

The U.S. Labor Department's CPI for September, released last month, saw a slight year-on-year decrease to 2.4%, well below the nearly 9% peak during the pandemic. However, the data for September also showed that prices in areas such as food, clothing, auto insurance, and airfare are still facing upward pressure. "The market will be concerned about this," Krosby said, noting that any specific signs of rising inflation in October could trigger a stock market pullback. Following the election, the stock market is already "close to overbought status."

Tani Fukui, Economist at Metlife Investment Management, pointed out that there has been significant market volatility since the election. She believes that any major surprises in the CPI report on Wednesday could trigger more significant market fluctuations, although perhaps not as drastic as in the days following the election. Fukui said, "While I hope inflation can be controlled, I don't think we have completely achieved that goal yet."

According to a survey by 22V Research, 31% of investors indicate that tonight's U.S. CPI data will trigger "safe-haven" reactions, with only 14% of investors saying it will trigger "risk appetite." 55% of investors expect the market's response to the CPI to be "mixed/negligible."

Meanwhile, in the 22V survey, 48% of investors still believe that core CPI is on a path favorable to the Federal Reserve, without significant financial environment tightening or economic recession. However, 44% of investors believe that the financial environment needs tightening. This proportion is the highest since April.

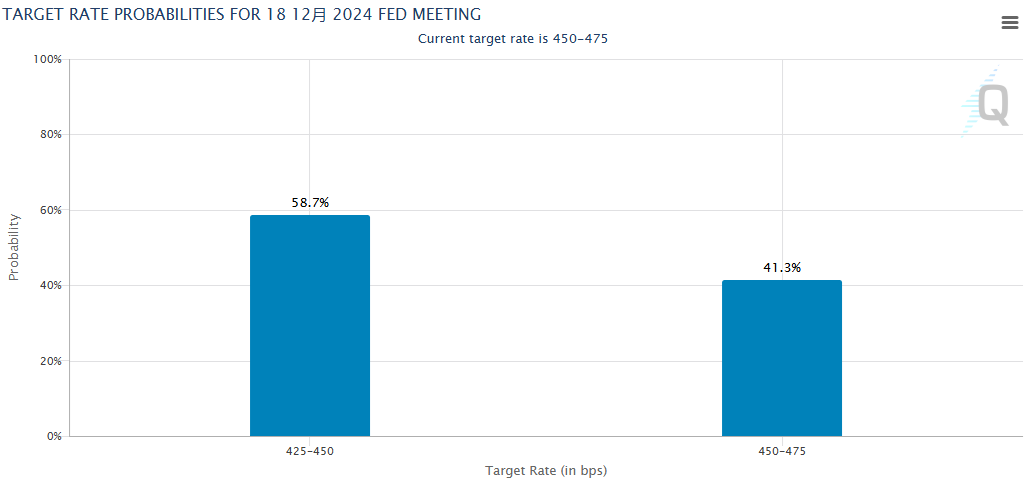

According to the CME FedWatch Tool, traders in the interest rates futures market currently estimate a 59% probability of a rate cut by the Federal Reserve in December, with a 41% probability of staying put.

Editor/Somer