10月CPI同比上涨2.6%,较前月的2.4%上升0.2个百分点,环比0.2%持平前值;

10月CPI同比上涨2.6%,较前月的2.4%上升0.2个百分点,环比0.2%持平前值;Bank of America Merrill Lynch stated that the CPI and core CPI in the United States in October are expected to remain flat compared to the previous month, with increases of 0.2% and 0.3% respectively. This is unlikely to cause a significant change in inflation expectations and will not threaten the Fed's inflation target. Bank of America Merrill Lynch also emphasized not to go against market trends, as the post-election momentum typically lasts for the following weeks.

With the dust settling on the US election and the November interest rate cut by the Federal Reserve, market attention quickly shifts to the heavyweight inflation data to be released this week, especially the US Consumer Price Index (CPI).

At 21:30 on Wednesday, Beijing time, the US Bureau of Labor Statistics will release the October CPI data. Market consensus expectations:

In October, the CPI rose by 2.6% year-on-year, an increase of 0.2 percentage points from the previous month's 2.4%, and remained flat at 0.2% month-on-month compared to the previous value;

The core CPI maintained a year-on-year and month-on-month growth rate of 3.3% and 0.3% respectively.

Bank of America Merrill Lynch stated that the US October CPI and core CPI are expected to increase by 0.2% and 0.3% month-on-month, but this increase is not likely to have a significant impact on interest rates.

Analysts from the institution, including Ohsung Kwon, stated in a report released last week that although there is pressure for prices to accelerate during the economic recovery, this is not expected to cause a major change in inflation expectations or threaten the Fed's inflation target.

Slowing down the betting on interest rate cuts

Last week, the Federal Reserve's FOMC cut interest rates by 25 basis points as expected by the market. Powell said in a press conference after the meeting that the fight against inflation is not over, core inflation remains somewhat high, the job market continues to cool very slowly, the Fed will continue to cut rates, but if inflation cools down and the economy remains strong, the rate cuts can be slower. The upcoming U.S. election will not affect monetary policy in the short term, while the future impact of fiscal policy will be taken into consideration, with U.S. deficits and fiscal policies acting as economic barriers.

Although the Fed did not hint at pausing its actions, Wall Street's bets on slowing rate cuts seem to be quietly warming up. Goldman Sachs currently expects the Fed to cut rates by 25 basis points at the December, January, and March meetings, and then by 25 basis points in June and September next year. Previously, Goldman Sachs predicted 25 basis point cuts in May and June.

Currently, CME tools show a 65% probability of a rate cut by the Fed in December and a 23.6% probability of a further rate cut in January next year.

Bank of America Merrill Lynch pointed out that despite the election results being a 'foregone conclusion,' policy uncertainty remains high. The Fed cut rates by 25 basis points as scheduled at the November monetary policy meeting, indicating that a rate cut in December is possible. This suggests that the Fed may remain vigilant about the current economic conditions and be prepared to take further easing measures to support economic growth.

Do not go against market trends, especially in the short term.

Bank of America Merrill Lynch also emphasized not going against market trends, especially the short-term uptrend after the U.S. election.

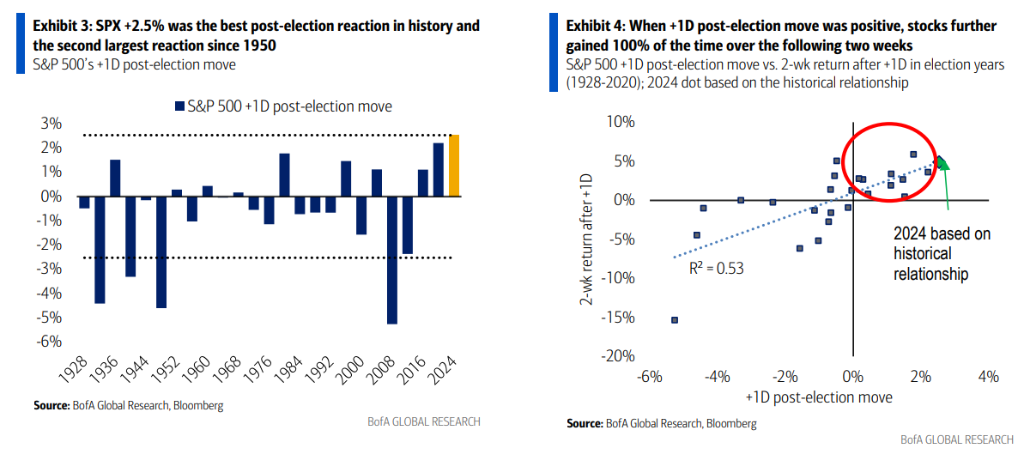

The report points out that the post-election momentum typically lasts for the following weeks. When the stock market achieves a significant increase on the first day after the election, historical data shows that in the following two weeks of past election cycles, the market has been positive 100% of the time. Interest rates have also essentially returned to pre-election levels, at least easing the main concerns of stocks for now.

Following this round of elections, the S&P 500 index rose 2.5% on the first day after the results were announced, achieving its best performance since 1928.

Editor/ping