The Federal Reserve has taken longer than Wall Street expected to withdraw liquidity from the market, but Trump's victory may make the prospect of ending QT more urgent.

Since the COVID-19 pandemic in 2020, the Federal Reserve has been extra cautious to avoid surprising Wall Street with its views on interest rates, the economy, or inflation, and even facing criticism for 'saying too much.'

However, when it comes to the massive balance sheet and the liquidity it deems necessary to maintain market equilibrium, the Federal Reserve may face criticism for being tight-lipped.

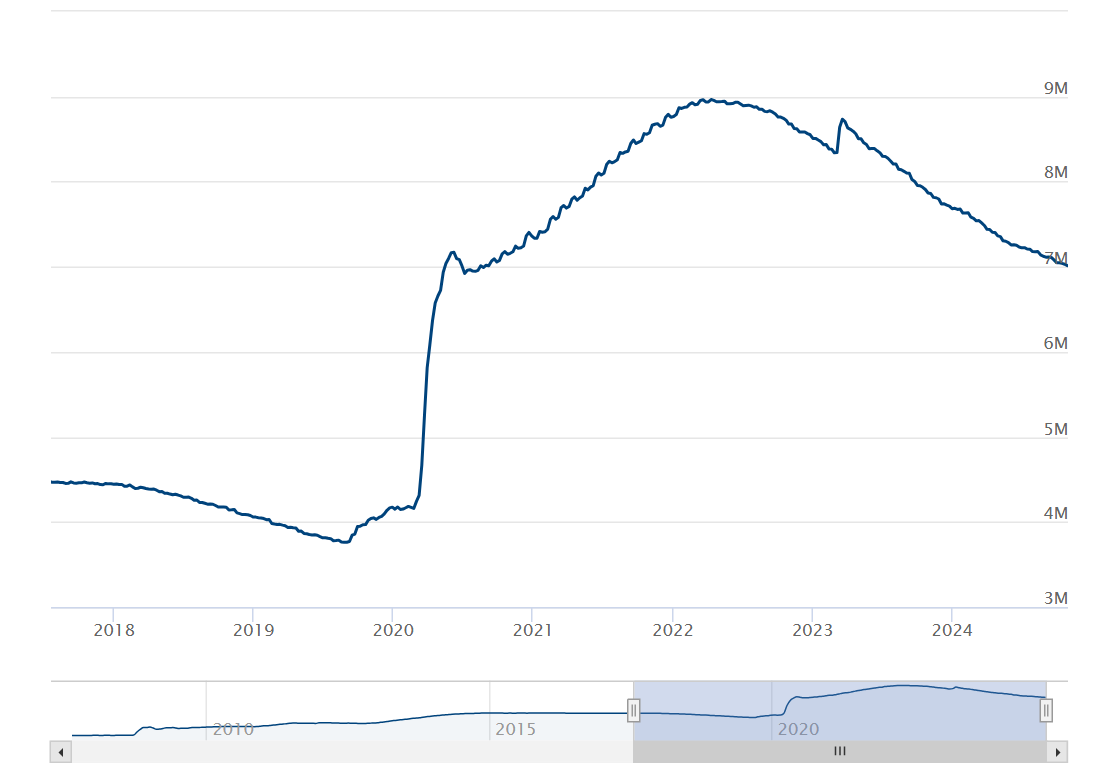

The total size of the Federal Reserve's balance sheet has dropped below $7 trillion for the first time since August 2020, indicating that the current round of shrinking the balance sheet has reached about $2 trillion. The Federal Reserve stated in its latest announcement on Thursday that it will maintain the same scale of balance sheet reduction, that is, reducing $25 billion of US Treasuries and $35 billion of MBS per month.

The total size of the Federal Reserve's balance sheet has dropped below $7 trillion for the first time since August 2020, indicating that the current round of shrinking the balance sheet has reached about $2 trillion. The Federal Reserve stated in its latest announcement on Thursday that it will maintain the same scale of balance sheet reduction, that is, reducing $25 billion of US Treasuries and $35 billion of MBS per month.

Brij Khurana, Senior Managing Director at Wellington Management Company, pointed out that earlier this year, it was widely believed that the Federal Reserve would end quantitative tightening (QT) by the end of 2024, a process of reducing the balance sheet by allowing its assets to mature.

However, based on the Federal Reserve's survey of primary dealers, expectations for ending QT have been delayed in recent months. Additionally, a few weeks ago, Dallas Fed President, Robert Kaplan - often referred to as the chief architect of the central bank's balance sheet - stated in a speech, 'Liquidity seems abundant.'

Her remarks surprised Khurana, especially with bank reserve reductions, increased usage of the Federal Reserve's overnight reverse repurchase tool (a closely watched liquidity indicator) around month-end. Benchmark borrowing rates are also rising, a sign of potential pressures bubbling up in financial market pipelines.

Khurana said, 'They seem satisfied with this now.'

How far is the Fed from ending QT?

Barclays interest rate strategist Joseph Abate said in September that the Fed should announce the end of QT at the November meeting and stop QT in December.

The global interest rate strategist at Bank of America believes that when the Fed's first rate cut in four years arrives, QT will end. However, despite the Fed's extensive rate cuts in September, the Fed still allows a certain amount of US Treasury bonds and agency mortgage-backed securities to leave its balance sheet every month.

After the global financial crisis of 2007-08 and during the COVID-19 pandemic, the Fed significantly increased its asset holdings, leading its balance sheet to swell to nearly $9 trillion two years ago. At that time, the Fed's goal was to mitigate the extent of the US economic downturn by boosting risk appetite and capital markets, and controlling long-term interest rates.

The trickier part is how to return the balance sheet to a more normal level after the turmoil. During the period from the global financial crisis to the onset of the pandemic, the Fed only slightly reduced its holdings.

To maintain order, the Fed has been reducing its balance sheet for two years. At the peak of the reduction, the Fed allowed up to $95 billion of US Treasury bonds and agency mortgage-backed securities to mature without reinvestment each month. In June this year, it slowed the pace of reduction, allowing up to $25 billion of Treasury securities to mature monthly, down from $60 billion previously, while keeping the cap on agency mortgage-backed securities reduction unchanged at $35 billion.

Fed officials say they hope any QT will 'be like watching paint dry,' quietly in the background without causing a disturbance. The Fed's overall goal is to reduce liquidity in the banking system to a 'plentiful' quasi-level without falling into 'scarce' territory.

Logan said in October that reserve balances were $3.2 trillion, up from $1.7 trillion at the beginning of 2020. Kularna stated that Wall Street estimates the minimum bank reserve requirements may approach $3 trillion.

It is currently unclear where the threshold for the Federal Reserve to stop QT may be, as well as whether there is a risk of withdrawing too much liquidity from the market in this process. The Federal Reserve described the "adequate" level of bank reserve as "uncertain" in May, but indicated that it would handle "unknown" situations cautiously.

Lou Crandall, Chief Economist of Wrightson ICAP, said in a phone interview, "They are far from ending QT." Instead, he stated that the Fed's goal is to "gradually reach the target" while hoping to avoid market turmoil in the process of reducing the balance sheet.

The impact of the elections

The message conveyed by the Federal Reserve to the market is that its plan for achieving an economic soft landing mainly focuses on interest rates rather than the size of its balance sheet.

On Thursday local time, the Federal Reserve continued to cut interest rates by 25 basis points, bringing its policy rate to a range of 4.5% to 4.75%. However, the victory of former President Trump in the election could have a significant impact on interest rate prospects.

Trump has promised that if elected, he will implement more tariffs and tax cuts, which could reignite inflation, limit future rate cuts by the Federal Reserve, and further increase the US deficit.

Andrzej Skiba, Head of Fixed Income at Royal Bank of Canada Global Asset Management, said, "The worst-case scenario is high inflation and an economic slowdown, an outcome that the Federal Reserve does not want to see."

In this scenario, Skiba expects the Federal Reserve to keep interest rates in a restrictive range and stop reducing its balance sheet. If the elections bring additional tax cuts and regulatory relaxation, he expects this to be beneficial for the stock market but harmful for bonds.

Crandler said that the areas currently monitored by the Fed to help gauge the level of "adequate" reserve levels are not showing any warning signals, but the moment to end QT may arrive when the next Congress must reach an agreement on the US debt ceiling.

As recently pointed out by MarketWatch editor Greg Robb, the current debt ceiling suspension is set to expire on January 1 next year. If no agreement is reached, the Treasury will need to once again start depleting its general account to meet its obligations until an agreement can be reached.

Wrightson said, "You must safely navigate the debt limit deadlock before this becomes a meaningful discussion."

Editor/Rocky