针对选举的对冲解除;重新杠杆化;回购;FOMO;衡量期权隐含波动率变化所致Delta变化的Vanna。

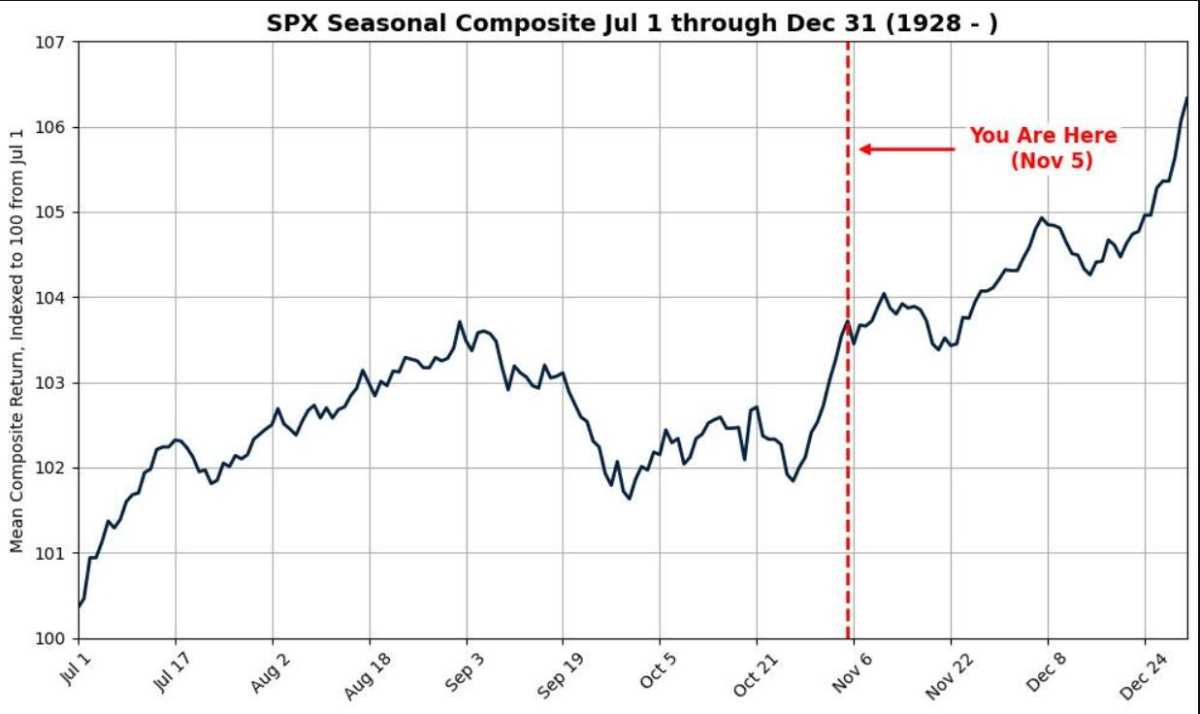

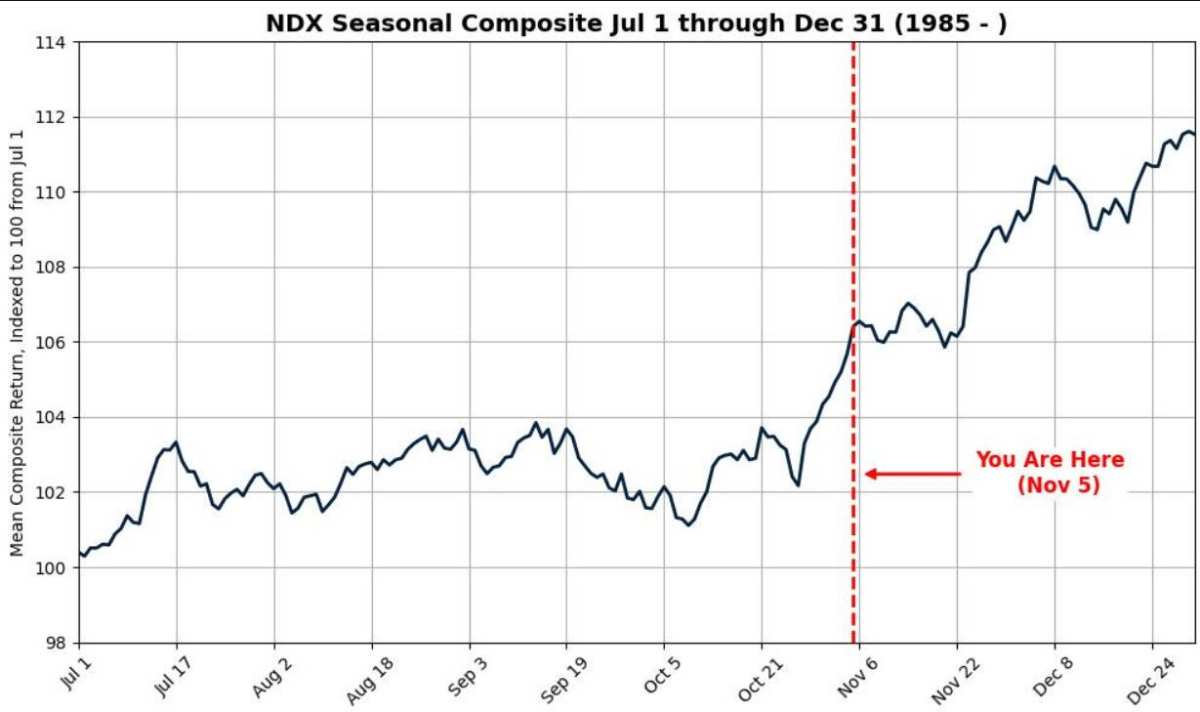

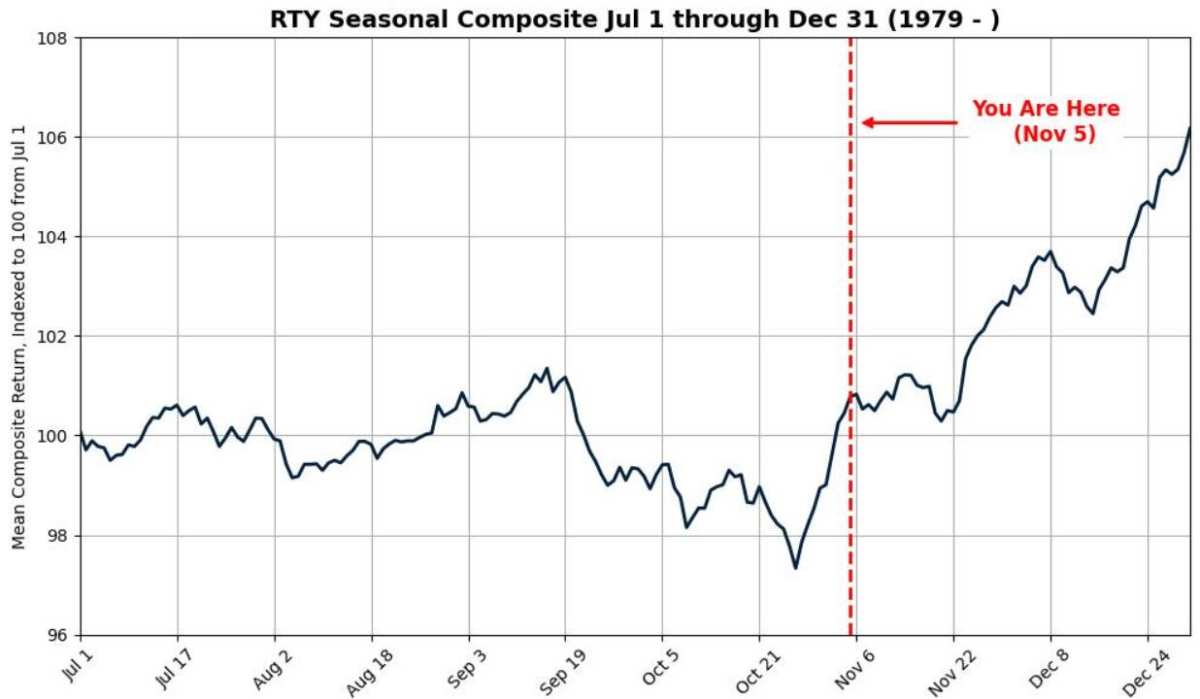

针对选举的对冲解除;重新杠杆化;回购;FOMO;衡量期权隐含波动率变化所致Delta变化的Vanna。Goldman Sachs expert Rubner stated that since 1928 in election years, the average return of the s&p 500 index from November 5th to December 31st is 3.38%; since 1985 in election years, the average return of nasdaq 100 during this period is 0.79%; since 1979 in election years, the average return of russell 2000 during this period is 7.94%.

Goldman Sachs research fund flow expert Scott Rubner predicted last month that by the end of this year, the S&P 500 index will soar well above 6000 points, and last week he said that U.S. stocks are entering the best fourth quarter trading phase in nearly a century. After Trump's election victory, Rubner once again exclaimed that the uptrend in the U.S. stock market will start from Wednesday, November 6th, this year, and may rise even higher than investors expect. Following the decline in U.S. stocks in October, he does not rule out a larger-scale stock market rebound led by capital rotation.

Rubner stated that during this year's best trading season, the mechanical rebalancing of funds will form a feedback loop of institutional FOMO psychology. This Wednesday, the five major funds tracked by Rubner include:

Hedging unwinding for elections; re-leveraging; buybacks; FOMO; Vanna measuring Delta changes due to changes in implied volatility of options.

Rubner believes that the short-term unwinding of election hedges has created demand for synthetic options. He mentioned that this Monday, the CBOE put/call options ratio hit the highest level since September 24, 2021. Releveraging slows down, volatility controls, and high-risk parity relending.

Regarding share buybacks, Rubner reiterated that companies are the top buyers in the U.S. stock market. Previously, Rubner's report stated that Goldman Sachs believes the corporate buyback window will open on Monday, October 28th. Data from the Goldman Sachs trading desk shows that since 2007, November has historically been the month with the largest buyback volume in a year, accounting for 10.40% of the annual buyback volume. Goldman Sachs estimates that the value of buyback stocks executed in 2024 will be $960 billion, and the value of November's share buybacks will be $100 billion.

Rubner also reiterated the above data and mentioned again that he estimated the daily volume for the 19 trading days of NovemberVolume-weighted average pricedemand is about 6 billion US dollars, which may also have a greater potential demand impact on days with lower liquidity during the holiday period.

In terms of institutional trading, Rubner mentioned that there were signs of continuous decline in institutional portfolios on the election night of November 5. Goldman Sachs' Prime Brokerage (PB) team stated that the aggregate exposure of stock fund managers with fundamental strategies in the US market has dropped to the lowest level since March 2023.

On the seasonal factors, Rubner used data from nearly a century to show that US stocks have historically risen from November to December each year, with the S&P's ROI exceeding 3% during this period in election years:

Since 1928, the average ROI of the S&P 500 index from November 5 to December 31 each year is 2.68%; since 1928 in election years, from November 5 to December 31, the average ROI of this index is 3.38%.

Since 1985, the average ROI of the Nasdaq 100 index from November 5 to December 31 each year is 5.53%; since 1985 in election years, from November 5 to December 31, the average ROI of this index is 0.79%.

Since 1979, from November 5 to December 31 each year,E-mini Russell 2000 Index the average return rate is 5.7%; in election years since 1979, from October 15 to December 31 each year, the index has an average return rate of 7.94%.

Editor/Lambor