Bloomberg macroeconomic strategist Simon White believes that while it is generally believed that Trump's policies will fuel inflation in the USA, the market currently still underestimates the inflation outlook. He stated that, based on risk adjustment, inflation-linked bonds remain one of the best assets to combat rising inflation.

According to media reports, after Trump's election victory, the U.S. Treasury Inflation-Protected Securities (TIPS) market became active, with breakevens rising by more than 10 basis points. However, experts pointed out in their article that the market has not fully reflected the inflation risks exacerbated by the election results.

Bloomberg macroeconomic strategist Simon White wrote on ZeroHedge that Trump's victory is not a necessary factor for triggering U.S. inflation, but it will indeed contribute to inflation. He analyzed that current price growth has stabilized, but the mythical 'last mile' to inflation has turned into a marathon. Robust economic growth, strong corporate profit margins, China's increasing stimulus measures, and the nearly $2 trillion fiscal deficit in the U.S. have already put inflation on the path to recovery. And if Trump governs as expected, implementing policies of tariff hikes, tax cuts, and increased spending, inflation risks will further intensify.

However, he still believes that the market underestimates the inflation outlook. Among the changes in U.S. bond yields on Wednesday, only about 40% came from breakevens. Breakeven inflation is the difference between nominal bond yields and Treasury Inflation-Protected Securities (TIPS) yields. This value reflects the market's expectations for future inflation rates: when breakeven points rise, it indicates that the market expects future inflation to increase; conversely, when breakeven points drop, it indicates the market expects inflation to weaken.

However, he still believes that the market underestimates the inflation outlook. Among the changes in U.S. bond yields on Wednesday, only about 40% came from breakevens. Breakeven inflation is the difference between nominal bond yields and Treasury Inflation-Protected Securities (TIPS) yields. This value reflects the market's expectations for future inflation rates: when breakeven points rise, it indicates that the market expects future inflation to increase; conversely, when breakeven points drop, it indicates the market expects inflation to weaken.

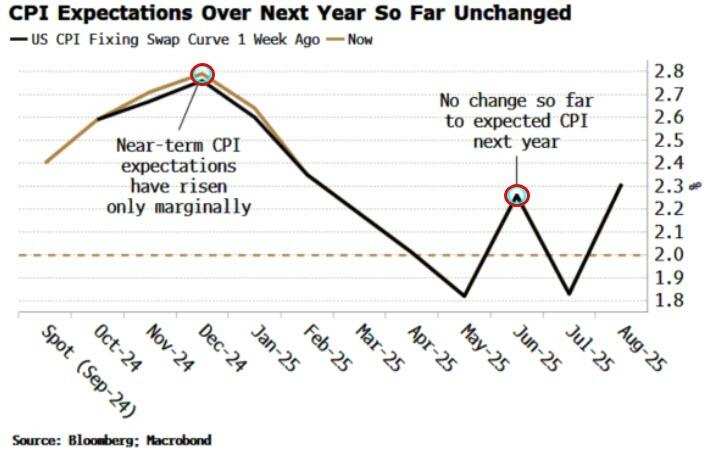

In addition, 'CPI fixing swaps', the market's expectations for CPI in the next 12 months, have remained almost unchanged. Specifically, these swaps reflect the market's expectations for the level of CPI over a certain period in the future (usually 12 months). If the market believes that future inflation will rise, the price of CPI fixing swaps will increase because both trading parties have a higher demand for the risk of future high inflation.

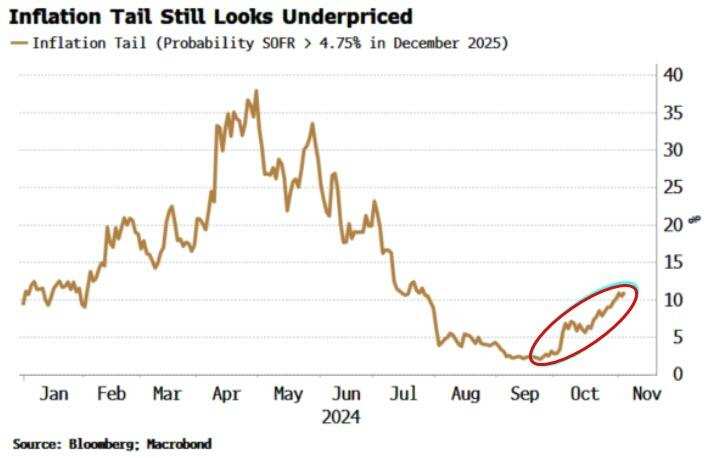

White stated that although such products have poor liquidity and may have daily fluctuations, observing SOFR options can also convey similar information. The probability of extreme tail risks for inflation remains low, where the risk refers to the Fed being forced to raise rates to over 4.75% in December 2025 (assuming the Fed will cut rates by 25 basis points as expected at Thursday's meeting and then need to raise rates again next year). Although the probability of this scenario has been increasing, it currently remains slightly above 10%.

Therefore, White believes that it seems to require significant force to compel the Federal Reserve to raise interest rates again next year. He thinks that the current situation may seem reasonable, but when the range of possible outcomes for the development prospects of inflation is as broad as it is now and inflation has shown stickiness, a 10% probability seems too low.

He believes that, based on risk adjustments, TIPS is still one of the best assets to combat rising inflation.

Previously, several financial institutions have warned that Trump's presidency may change the future interest rate policy path of the Federal Reserve.

According to the latest research report released by Bank of America Merrill Lynch, if Trump takes office and implements fiscal expansion, the Federal Reserve may raise its expectations for neutral interest rates. In addition, if the new president significantly imposes tariffs, the Federal Reserve may temporarily pause rate cuts due to concerns about the impact on inflation and economic growth. JPMorgan has also warned that if Trump wins on Wednesday, the Federal Reserve may pause the easing cycle as early as December, with the bank expecting a 25 basis point rate cut in November.