2024年以来,消费复苏仍然存在一定压力,除家电存在明显的海外扩张逻辑,其他基于国内消费为主的消费板块仍然居后,现有的性价比消费会逐渐理性化,精神消费相关的行业供给端更加确定,有望持续跑赢。

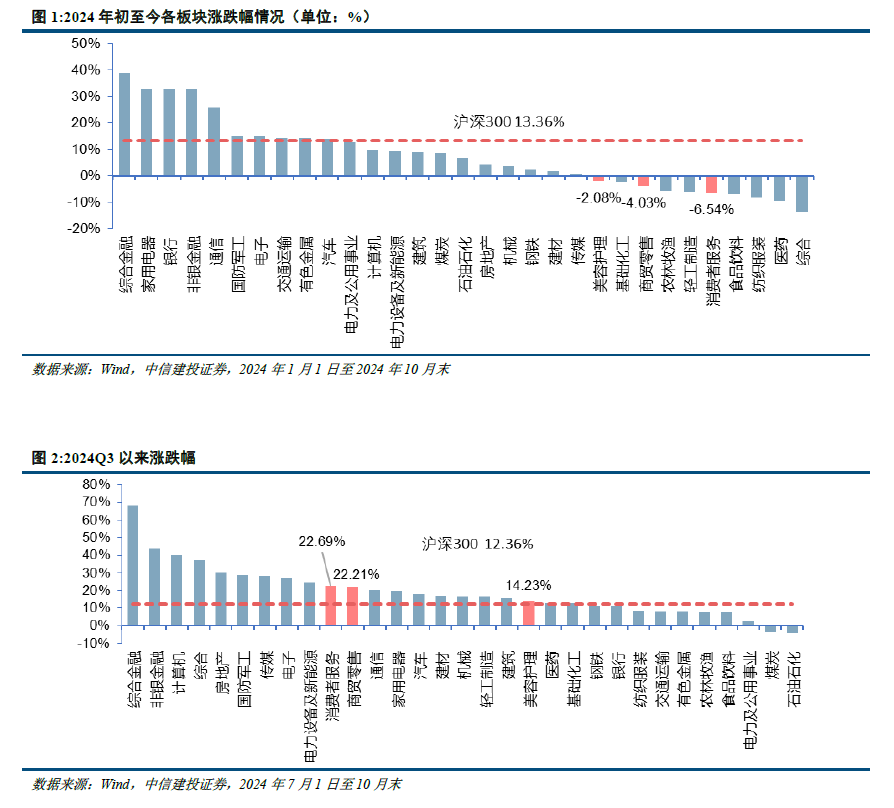

2024年以来,消费复苏仍然存在一定压力,除家电存在明显的海外扩张逻辑,其他基于国内消费为主的消费板块仍然居后,现有的性价比消费会逐渐理性化,精神消费相关的行业供给端更加确定,有望持续跑赢。As of the end of October 2024, the trend of the beauty and care sector was -2.08%, commerce and retail -4.03%, consumer services -6.54%. Despite the recent market warming, it still lags behind the CSI 300 Index.

Smart Financial APP learned that China Securities Co., Ltd. released research reports stating that as of the end of October 2024, the trend of the beauty and care sector was -2.08%, commerce and retail sector was -4.03%, and consumer services were -6.54%. Even with the recent market warming, they still lag behind the CSI 300 Index. The prosperity of the domestic and foreign consumer sectors continues to decline, most industries will still face pressure in the fourth quarter, but industries at the bottom of the supply side are gradually increasing. Rational cost-effectiveness is the active choice of current consumers, with the transmission of policy efforts expected to trigger inflation expectations. It is recommended to pay attention to the expected performance of flexible industries such as dining, supermarkets, and gold.

Main viewpoints of Zhongxin Jiandao are as follows:

Since 2024, there is still some pressure on consumption recovery. Apart from home appliances showing significant overseas expansion logic, other consumption sectors mainly focused on domestic consumption are still lagging behind. Existing cost-effective consumption will gradually rationalize, and the supply side of industries related to spiritual consumption becomes more certain, expected to continue to outperform.

Since 2024, there is still some pressure on consumption recovery. Apart from home appliances showing significant overseas expansion logic, other consumption sectors mainly focused on domestic consumption are still lagging behind. Existing cost-effective consumption will gradually rationalize, and the supply side of industries related to spiritual consumption becomes more certain, expected to continue to outperform.

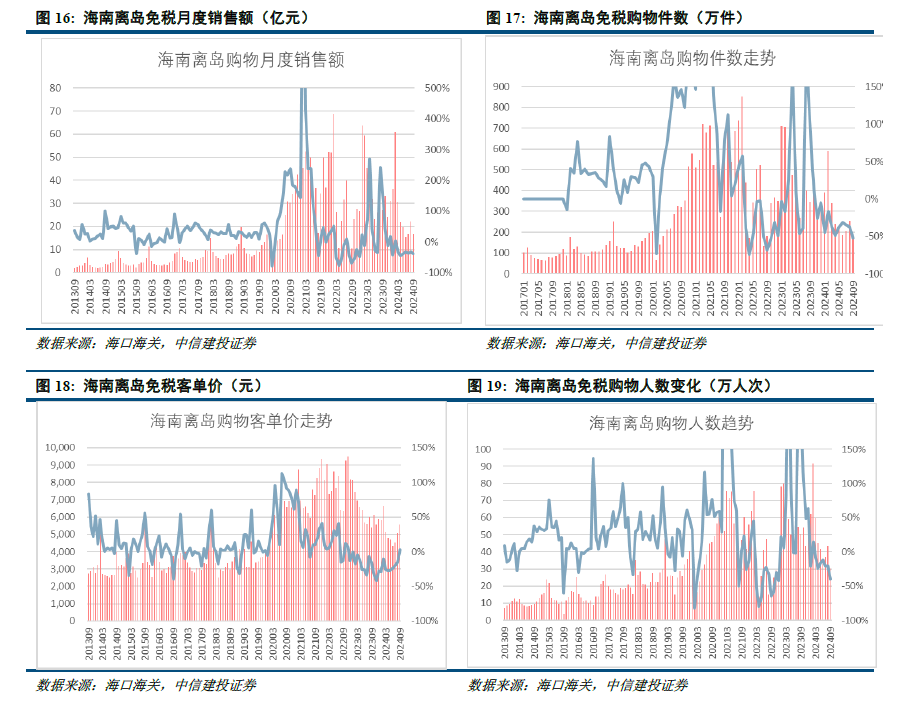

Duty-free sector: Sales have been under pressure this year, with the gradual cultivation of local duty-free policies, some restoration at airport ports, stable competition in Hainan region, enriching the development of newly added properties in the second round of duty-free business on outlying islands, awaiting development from quantity to quality. Inbound and outbound tourism continues to recover, with noticeable optimization in rental prices at core airport ports, focusing on sales marginal trends.

Tourism, gambling: The number of tourists traveling within the year continues to recover and rise, with a great resilience in performance by leading companies, highlighting the essential attributes of discretionary spending. Structurally, attention is focused on the growing proportion of the lower-tier market and the silver-haired tourist group. The Macau region has seen good recovery in customer flow and spending power, with the market share of leading gambling licenses stabilizing and property increment gradually releasing. The OTA track has a competitive advantage, with stable traffic empowerment.

Hotels: Business travel demand has shown weak recovery so far this year, but leisure demand continues to grow, with high industry supply growth and leading companies optimizing supply. Hotel sectors with strong pro-cyclical properties await improvements in the overall macroeconomic expectations to drive valuation rebound. The validation of high-end ecological brand positioning and supply chain capabilities can still bring alpha, with room for further improvement in chain linkages in the long term.

Dining: Under the strategy of high-frequency iteration, the price wars in medium and large cities are still ongoing. It is expected that in the next two years, the industry will continue to be in a period of optimized supply and brand iteration, testing the comprehensive operational and cost management capabilities of companies. Leading companies currently have stable cash flow, with the same-store performance gradually stabilizing in 24Q3, while overseas expansion, multi-branding, and new models may become growth points.

Medical aesthetics: Overall performance of medical aesthetic demand is relatively weak due to macroeconomic factors, with mature products experiencing noticeable slowdowns on both the production and sales ends. The industry logic itself leans more toward product cycle logic, with the growth of individual stocks directly related to pipelines and segmented tracks, making the stock cycle more identifiable.

Cosmetics: Most companies did not exceed Q3 revenue expectations, and higher profit growth is often driven by cost optimization. The gross sales difference to a certain extent reflects the brand's lifecycle, but the narrowing of this indicator in the overall industry is more of a common trend under changes in industry channel traffic. With actual asset turnover improvement, ROE can still achieve growth.

General retail and going global: With the gradual weakening of stimulus policies, inflation expectations are expected to rise, thereby boosting the performance of the supermarket sector with the most elasticity. Recommended to pay attention to: Jiajiayue (603708.SH); The continuous prosperity of the shipbuilding industry, the accumulated speed of orders may exceed market expectations, and the performance of capacity expansion is restrained. It is recommended to continue to focus on Sumec Corporation (600710.SH) with high dividends, low valuations, and long-term growth potential. Domestically, globally powerful companies are gradually emerging, whether online on multiple platforms or offline focusing on physical stores. Means of dealing with risk factors such as tariffs, exchange rates, etc., are also becoming more mature and reliable.

Gold and jewelry: The continuous rise in gold prices suppresses demand for jewelry, but under the direct sales model, demand control is more precise, reacting faster compared to the franchise model.

Risk warning

1. The timing and extent of US rate cuts may differ from market expectations, causing significant fluctuations in related assets such as gold, US Treasury bonds, and the US dollar index, impacting the operation of related businesses.

2. The hotel supply and demand are in tight balance, and the continued weak trend in business demand may lead to funding pressures for franchisees and a potential impact on store opening intentions, thereby affecting the clearance of supply in the hotel industry and the realization of the accelerated development logic of leading players.

In the dining industry, the continuous price war may intensify further in top-tier cities. In the process of channel customer acquisition cost increasing, it is difficult to pass on costs to the upstream and downstream; secondary brand development, product innovation, and industry chain extension are below expectations.

In the cosmetic industry, the efficiency of traffic conversion is lower than expected, and competition loses to international brands. The cost of traffic acquisition keeps rising, domestic brands still need time for overall cultivation, facing direct competition pressure from international brands.

Tougher regulations in the medical aesthetics field bring emotional impact; upstream companies' new product development and approval progress are below expectations; competition at the product end is increasingly fierce; expansion of medical aesthetic institutions faces difficulties, and the new institutions have a longer period of profit and loss balance.

If the USA experiences an economic recession and insufficient consumer demand, it may cause damage to some economies, resulting in an imbalance in the global trade system, affecting the recovery of foreign trade demand.

Significant fluctuations in gold prices affect residents' consumption willingness. The continued decline in the number of marriages and newborns may impact the terminal demand for celebratory gold jewelry.