Ferrari's third-quarter shipments fell by 2.2% year-on-year, with a 29% year-on-year decline in the Chinese market and a 2.4% year-on-year decline in the US market, and did not revise the annual performance guidance it provided in August, with the stock price falling more than 6.9% in regular trading hours on Tuesday.

Ferrari has raised its performance guidance every Q3 since 2016, except for 2018 and this year.

On Tuesday, November 5th, before the US market opens, Italian luxury car brand Ferrari announced its 2024 third-quarter performance.

1) Key Financial Figures:

1) Key Financial Figures:

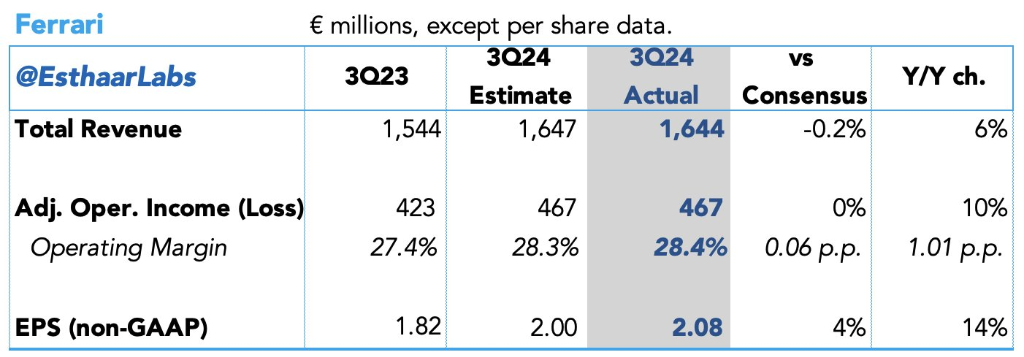

Revenue: Revenue for the third quarter was 1.64 billion euros, a 6.5% year-on-year increase, market expectations were 1.64 billion euros; among which, automotive and spare parts revenue was 1.4 billion euros, up 5.3% year-on-year, market expectations were 1.42 billion euros; sponsorship, commercial, and brand revenue was 0.174 billion euros, up 20% year-on-year, market expectations were 0.1617 billion euros.

Net Income: Adjusted net income for the third quarter was 0.375 billion euros, a 13% year-on-year increase, market expectations were 0.3698 billion euros.

EBITDA: Adjusted EBITDA for the third quarter was 0.638 billion euros, a 7.2% year-on-year increase, market expectations were 0.6338 billion euros; adjusted pre-tax profit was 0.467 billion euros, up 10% year-on-year, market expectations were 0.4633 billion euros; adjusted pre-tax profit margin was 28.4%, higher than the same period last year's 27.4%, market expectations were 28%.

EPS: Diluted earnings per share adjusted for the third quarter were 2.08 euros, compared to 1.82 euros in the same period last year, with market expectations at 2.03 euros;

Free Cash Flow: Industrial free cash flow for the third quarter was 0.364 billion euros, with market expectations at 0.3427 billion euros.

Delivery Volume: The delivery volume in the third quarter was 3,383 vehicles, a 2.2% decrease compared to the same period, with market expectations at 3,469 vehicles. In the segmented markets, delivery volume in Europe, the Middle East, and Africa was 1,426 vehicles, a 2% increase, with market expectations at 1,486 vehicles; in the Americas, the delivery volume was 1,070 vehicles, a 2.4% decrease, with market expectations at 1,097 vehicles; in China, the delivery volume was 281 vehicles, a 29% decrease, with market expectations at 348.4 vehicles; and in other Asia-Pacific regions, the delivery volume was 606 vehicles, a 6.3% increase, with market expectations at 582.27 vehicles.

After the financial report was released, Ferrari's US stocks fell more than 6.9% during regular trading hours, but have since risen over 31% year-to-date.

Analysts point out that while Ferrari's third-quarter profits were slightly better than analyst expectations, Ferrari did not raise its full-year performance guidance provided in August. Moreover, the market is very concerned about the shipment volume. The overall downturn in the automotive industry has also impacted Ferrari, with declining core business of luxury car shipments. Delivery volume in the third quarter decreased by 2.2% year-on-year, with a 29% decline in the Chinese market and a 2.4% decline in the US market.

The market is worried about the slowdown in luxury goods consumption, not just in automobiles. Even companies selling luxury goods, such as LV and Gucci's parent company Kering Group, are warning that business is becoming increasingly difficult.

Despite the decline in shipment volume, Ferrari found that customer demand for customized vehicles has increased. Ferrari CEO Benedetto Vigna stated:

"Ferrari's performance in the third quarter once again achieved growth, which benefited from a richer variety of products provided by the company and an increasing number of customers' demand for personalized customization. This confirms that Ferrari will adhere to the commitments made on Capital Markets Day in 2022, and our orders are already booked until 2026. We now have more confidence in achieving our annual targets."

Goldman Sachs analyst George Galliers and others maintain a "neutral" rating on Ferrari's stock, with a 12-month target price of 470 euros ($508). They noted on Tuesday:

"Ferrari has raised its performance guidance every third quarter since 2016 (except for 2018), so the lack of an increase this year could be seen as disappointing. Ferrari has reiterated its 2024 financial year guidance and stated that despite ongoing cost increases, they are more confident in achieving their targets."

Market expectations for Ferrari's EBITDA (earnings before interest, taxes, depreciation, and amortization) and EBIT (earnings before interest and taxes) are currently about 2.5% and 2.6% higher than Ferrari's lower-end guidance. Meanwhile, Ferrari's lower-end guidance also implies a reduction of approximately 11% in adjusted EBIT for the fourth quarter;

We expect Ferrari's performance guidance to remain conservative as in previous years. Ferrari stated that their orders are booked until 2026, and orders for the new F80 model have already been fully allocated."