不仅仅是Waymo频频发力,特斯拉等“洋萝卜”也对无人驾驶产业虎视眈眈。在10月10日正式推出无人驾驶出租车CyberCab后,特斯拉CEO埃隆・马斯克在第三季度财报电话会议上透露,已经面向特斯拉员工开启自动驾驶出租车测试,并有望在明年正式开启服务。

不仅仅是Waymo频频发力,特斯拉等“洋萝卜”也对无人驾驶产业虎视眈眈。在10月10日正式推出无人驾驶出租车CyberCab后,特斯拉CEO埃隆・马斯克在第三季度财报电话会议上透露,已经面向特斯拉员工开启自动驾驶出租车测试,并有望在明年正式开启服务。"Bend down" to break the profit dilemma?

The global self-driving industry is experiencing a life-and-death race. On October 30, Waymo, an autonomous car company under Google's parent company Alphabet, announced that its Waymo One (autonomous taxi) service is providing 0.15 million paid trips per week. This also means that Waymo's weekly volume has increased by 150% in just 2 months, tripling in half a year.

Although Waymo's current total volume of self-driving orders is less than didi Chuxing, Google's parent company is increasing its investment in Waymo to support its expansion into new cities and further develop its autonomous driving technology capabilities. On October 26, Waymo announced the completion of a $5.6 billion oversubscribed Series C financing round, the largest funding round raised by Waymo to date.

Not only is Waymo frequently exerting efforts, but "foreign carrots" like Tesla are also eyeing the self-driving industry. After officially launching the self-driving taxi CyberCab on October 10, Tesla CEO Elon Musk revealed during the third-quarter earnings conference call that autonomous driving taxi testing has been opened to Tesla employees and is expected to officially launch the service next year.

Not only is Waymo frequently exerting efforts, but "foreign carrots" like Tesla are also eyeing the self-driving industry. After officially launching the self-driving taxi CyberCab on October 10, Tesla CEO Elon Musk revealed during the third-quarter earnings conference call that autonomous driving taxi testing has been opened to Tesla employees and is expected to officially launch the service next year.

With the pincer attack of Google, Tesla, and other "foreign carrots", the global self-driving industry has reached a critical moment of "life or death", and autonomous driving has become the forefront battlefield of global technological competition. Wen Yuen Information Act (WRD.US) prospectus shows that by 2030, the global and mainland Chinese market for autonomous driving will reach approximately $1745 billion and $639 billion, respectively. The compound annual growth rates from 2022 to 2030 are 91% and 100%.

Looking at the domestic situation, although there are many players in the self-driving industry in China, only didi Chuxing has achieved large-scale and routine testing. It is also one of the few in China that has the hope of stepping onto the international stage and competing with the likes of Waymo and Tesla.

Against this backdrop, Wen Yuen Information Act, as China's first autonomous driving company to commercially operate Robotaxi on open roads, is increasingly highlighting its unique position to challenge the status of the "world's first stock of universal autonomous driving".

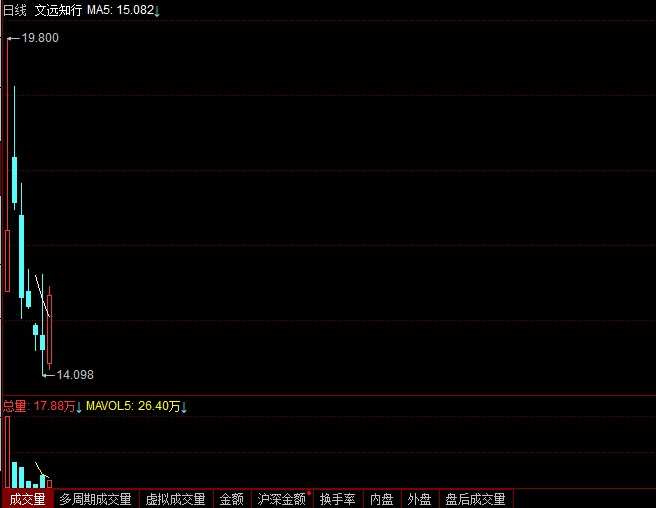

However, WeRide did not gain much favor in the capital markets. Despite triggering a circuit breaker twice on the first day of listing due to a significant increase, with a peak surge of over 27% during the day and closing up 6.77% at $16.55 per ADS. However, the company's stock price subsequently fell for several days, falling below the IPO price within just three days of listing. As of the close on November 4th, the stock closed at $15.46 per ADS, with a total market value of approximately $4.244 billion, still below the IPO price of $15.5.

Accumulated losses exceeded 5.1 billion yuan over the past three and a half years.

According to the prospectus, WeRide, established in 2017, has been conducting autonomous driving research, testing, and operations in 30 cities across 7 countries globally. It is the only technology company that holds autonomous driving licenses in China, the UAE, Singapore, and the United States. WeRide has rich practical experience in technology research and development, commercialization, and corporate management both domestically and internationally. It has established strategic partnerships with several top global OEMs and Tier 1 suppliers, including the Renault-Nissan-Mitsubishi Alliance, Yutong Group, Guangzhou Automobile Group, and Bosch.

WeRide Inc. is committed to developing safe and reliable self-driving technology, with application scenarios covering smart travel, intelligent freight transport, and intelligent sanitation. It has entered the commercial operation stage of autonomous driving, forming five major product matrices including Robotaxi, Robobus, Robovan, Robosweeper, and Advanced Driving Solution, providing various services such as online car-hailing, on-demand public transportation, local freight transport, intelligent sanitation, and advanced intelligent driving solutions.

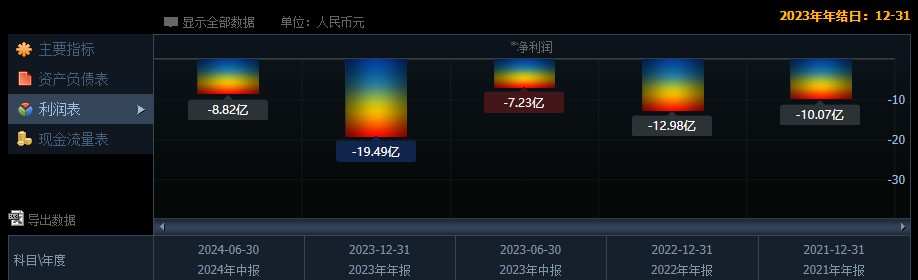

In terms of performance, from 2021 to the first half of 2024 (hereinafter referred to as the reporting period), the company's revenue was 0.138 billion yuan, 0.528 billion yuan, 0.402 billion yuan, and 0.15 billion yuan respectively. The revenue has declined since 2023; while the net income for the same period was approximately -0.882 billion yuan, -1.949 billion yuan, -1.298 billion yuan, and -1.007 billion yuan, resulting in an accumulated loss of about 5.17 billion yuan over three and a half years.

R&D expenses are the main reason for the losses. According to the prospectus, from 2021 to the first half of 2024, the company's R&D expenses were approximately 0.443 billion yuan, 0.759 billion yuan, 1.058 billion yuan, and 0.517 billion yuan, with a total R&D investment of 2.777 billion yuan over three and a half years. The substantial R&D investment and slow commercialization progress remain major challenges facing WeRide.

In terms of commercialization, Wenyuan Zhihang's two main sources of revenue: one is the sales of L4 level self-driving cars, including various types of robot vehicles and sensor kits; the other is to provide L4 self-driving and advanced driving assistance systems (ADAS) services, covering operations, technical support, ADAS research and development and other comprehensive services.

In addition, the prospectus data shows that from 2021 to 2023, Wenyuan Zhihang's self-driving taxis sold less than 20 in total, with 5, 11, and 3 sold in 2021, 2022, and 2023, respectively; the sales volume of self-driving minibuses sold 38, 90, and 19 in three years.

These financial data show that although Wenyuan Zhihang is rapidly expanding its business scale and user base, it still faces a daunting task in improving profitability. In the future, it must accelerate the pace of business diversification and commercialization.

Currently, the company's cash and cash equivalents amount to only 1.83 billion yuan. At the current rate of loss, the cash on Wenyuan Zhihang's books is only enough to run the company for just over a year. Therefore, Wenyuan Zhihang urgently needs to go public in the United States to raise funds by issuing stocks.

Can 'Leaning Downward' Break the Profit Dilemma?

As mentioned above, Wenyuan Zhihang's 'car-making' commercial monetization model has not been successful, and the embarrassing situation of single-digit product sales has caused the company's hardware revenue from Wenyuan Zhihang to plummet by 70%.

However, Wenyuan Zhihang has now welcomed its own white knight - Bosch. According to the prospectus, Bosch injected development fees of 0.15 billion and 0.1 billion RMB into Wenyuan in 2022 and 2023 respectively. This money has become a key factor in Wenyuan Zhihang's rescue.

According to the contract between the two parties, Wenyuan Zhihang will enter the L2 race track from L4, starting to provide L2-3 level self-driving large-scale mass-produced and market-applications for passenger vehicles.

Simply put, instead of producing cars, they are now starting to sell Asia Vets 'service packages'.

Moreover, for Shenzhen New Land Tool Planning & Architectural Design, which set L4 as its initial goal, developing L2 smart driving is even more technologically advantageous.

In the first half of 2024, Shenzhen New Land Tool Planning & Architectural Design and Bosch's 'Bosch China Advanced Intelligent Driving Solution' realized mass production and delivery, successively installed on Chery Star Way Starry Era ES and Starry Era ET.

Nowadays, revenue from autonomous driving services has gradually become the core revenue of Shenzhen New Land Tool Planning & Architectural Design. From 2021 to 2023, the proportion of product revenue of Shenzhen New Land Tool Planning & Architectural Design decreased from 73.5% to 13.5%, while service revenue proportion increased significantly, reaching 0.037 billion yuan, 0.19 billion yuan, 0.348 billion yuan, with proportions of 26.5%, 36.0%, 86.5%, gradually shifting to a light asset operation model.

In fact, Shenzhen New Land Tool Planning & Architectural Design 'leans down' from L4 level to L2 level assisted driving, which is the best 'blood recovery' strategy for most autonomous driving companies in the short term.

For example, XM Intelligent Driving's solutions have already been implemented in some Toyota and Lexus models, Momenta has relatively in-depth cooperation with Mercedes-Benz and BMW Brilliance, Haomo Intelligent Driving's HPilot intelligent driving system has also been installed on multiple models under Great Wall Motor.

However, as more and more auto manufacturers turn to independent research and development of autonomous driving technology (such as Xiaopeng, Huawei, and other enterprises, which have accumulated rich technological achievements), future competition may become more intense.

In fact, L4 autonomous driving companies have not given up exploring the ultimate vision of Robotaxi (driverless taxi). After all, this is the foundation for survival and also has broad commercial prospects.

According to Frost & Sullivan's forecast, Robotaxi services are expected to be commercialized around 2026, with the global market size expected to reach $0.29 billion in 2025 and grow to $66.6 billion in 2030. China has the potential to become the world's largest Robotaxi market, with market sizes projected to reach $0.2 billion and $39 billion in 2025 and 2030 respectively.

On October 15, WeRide announced the launch of the new generation mass-produced Robotaxi GXR, co-developed with Geely for remote operation.

As a mass-produced Robotaxi model, WeRide's GXR relies on its self-developed L4-level autonomous driving software and hardware system to provide industry-leading L4-level public road operation capabilities, capable of handling complex scenarios such as rush hours, mixed traffic, and night-time high-speed driving.

Huafu Securities analyst Lu Yufeng stated that advanced autonomous driving technology is accelerating its commercialization process, entering a new stage in regulations, technology, and capital operations. After years of development and accumulation, the industry is on the threshold of explosive growth.

The implementation of technology is always lengthy, especially for Robotaxis involving vehicle-road coordination, undoubtedly requiring a longer cycle. WeRide's successful IPO is expected to gain sufficient financial support and a first-mover advantage, but profitability remains an unavoidable issue for them.