这位德银分析师说,从这一点出发,直觉告诉我们,如果特朗普获胜,黄金将走高(+2%),而如果哈里斯获胜,黄金将走低(-2%)。不过,正如高盛也指出的那样,Hsueh预计黄金抛售将是短暂的,因为亚洲进口和央行需求将抵消投机性期货的资金流出。

这位德银分析师说,从这一点出发,直觉告诉我们,如果特朗普获胜,黄金将走高(+2%),而如果哈里斯获胜,黄金将走低(-2%)。不过,正如高盛也指出的那样,Hsueh预计黄金抛售将是短暂的,因为亚洲进口和央行需求将抵消投机性期货的资金流出。Deutsche Bank simulated the performance of gold under the Trump and Harris administrations, the results were shocking, and it also inspired the gold bulls.

In a must-read special report by Michael Hsueh at Deutsche Bank, the csi commodity equity index strategist examined the performance of the best asset in 2024 - gold in the next five years, and more importantly, simulated the comparison between the Trump and Harris administrations. The results are shocking and encouraging for the gold bulls.

As pointed out by Huseh, the safe haven properties of gold mean that it can fully express anxiety about the departure from the status quo. Therefore, gold's response to the election will mainly depend on the disruptive breakthroughs former President Trump has shown in trade, immigration, and foreign policies.

The Deutsche Bank analyst said that from this point, intuition tells us that if Trump wins, gold will rise (+2%), while if Harris wins, gold will fall (-2%). However, as Goldman Sachs also pointed out, Hsueh expects the selling of gold to be short-lived, as Asian imports and central bank demand will offset the outflow of speculative futures funds.

The Deutsche Bank analyst said that from this point, intuition tells us that if Trump wins, gold will rise (+2%), while if Harris wins, gold will fall (-2%). However, as Goldman Sachs also pointed out, Hsueh expects the selling of gold to be short-lived, as Asian imports and central bank demand will offset the outflow of speculative futures funds.

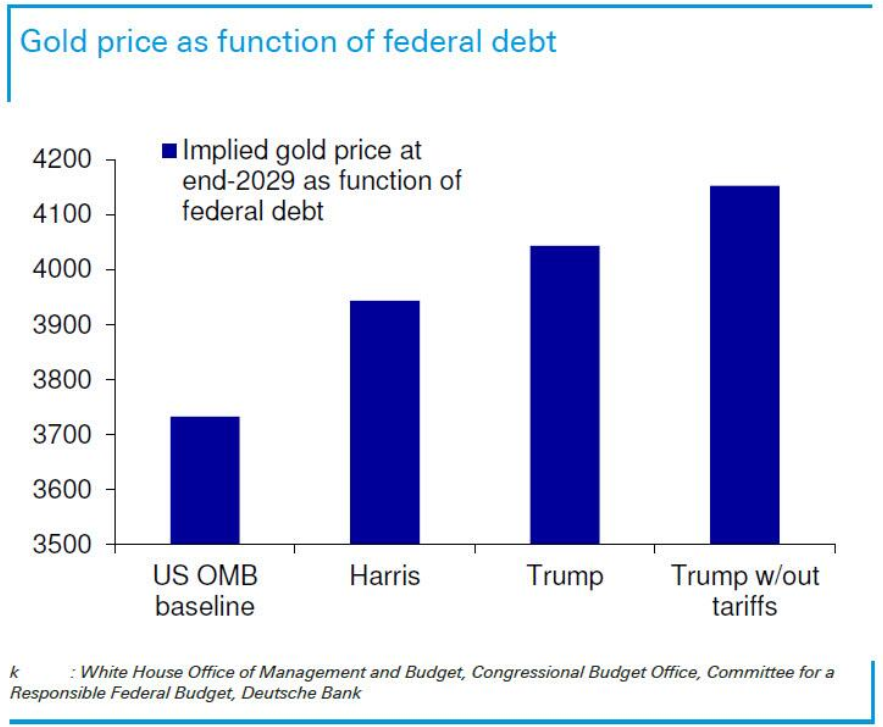

Moreover, gold's positive response to federal debt growth is obvious. Some banks, like Deutsche Bank, expect Trump's budget plan to lead to an increase in the debt growth trajectory, although the potential budget assessment of the Harris administration also indicates an upward deviation from the baseline. In other words, regardless of who takes office, U.S. debt will be much higher in 5 years. That is to say, Trump's government, which does not impose import tariffs, will put federal debt on an exceptionally high-growth trajectory, meaning that the gold price at the end of 2029 could reach as high as $4150 per ounce, with the baseline forecast at $3730 per ounce.

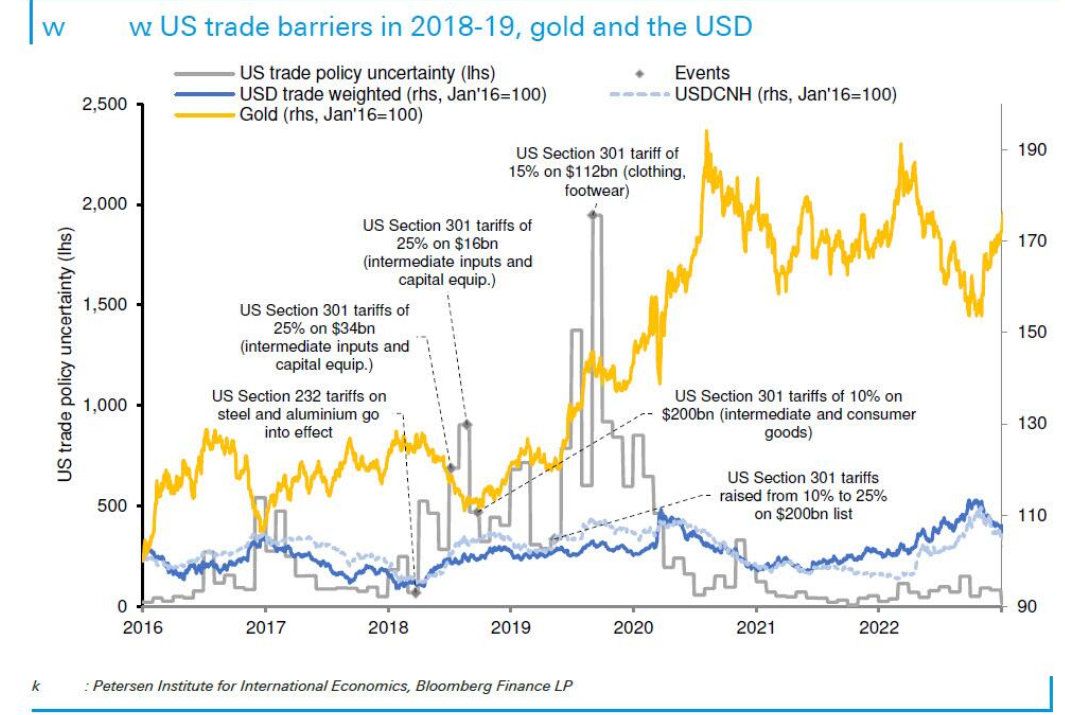

On the other hand, in the context of trade policy, the potential impact of a stronger dollar on gold remains unclear, with many unknown factors: the results of bilateral trade negotiations, and the behavioral responses of importers, exporters, and consumers. Studies of the 2018-19 situation suggest that gold could decline, although this is partly influenced by the Fed's interest rate hike cycle.

As for immigration policies, Trump will once again deviate from the status quo, but here we can see the importance of the composition of Congress; without a 'red wave,' Congress will have more room to restrict efforts to deport immigrants.

Of course, in the event of a Harris victory, controversial results are always possible, but given the difficulty of predicting the outcome in this scenario, this can only be seen as a footnote. Gallup polls on election accuracy and the possibility of voter fraud show that partisan divisions have been increasing since 2016.

Here are some key points mentioned in the deutsche bank report.

1. Based on the evaluation of the fiscal policies of Trump and Harris, the specific gold price calculated by deutsche bank's model is:

Including a fixed model growth rate of 1.4% per year for the gold price, and based on the assumed gold price of $2700 per ounce at the end of 2024, this means the gold prices at the end of 2029 are as follows:

Baseline prediction: $3730 per ounce (nominal annual compound growth rate of 6.7%)

Under the Harris administration: $3940 per ounce (nominal annual compound growth rate of 7.9%)

Under the Trump administration: $4040 per ounce (nominal annual compound growth rate of 8.4%)

Under the condition of Trump not imposing tariffs: $4150 per ounce (nominal annual compound growth rate of 9.0%)

2. The importance of trade policy can be said to be paramount, but due to the counteractive effect of the appreciation of the US dollar, the impact of trade policy on gold is not clear. Consider the following important factors:

a) Inflation. The Trump administration may impose new tariffs on all countries and may impose higher tariffs on goods from China. Recent experience has shown that as the average tariff on imports increases from 1.6% to 5.4%, the higher costs are largely passed on to US companies and consumers.

b) US dollar appreciation. Academic studies have found that currency changes partially offset the increase in tariffs. This is because domestic producers can raise prices of goods, and the central bank will choose a more contractionary monetary policy.

c) Safe assets. The increase in uncertainty of trade policy will drive up the value of safe assets including the US dollar and gold.

Although (c) is clearly positive for gold, the combination of (a) and (b) is ambiguous because the balance between the two depends on the extent of (a)'s impact on monetary policy and interest rates. From (a) to (b), policymakers tend to overlook one-time shocks, which is a favorable environment for gold, while preemptive and forceful policy responses may have a negative impact on gold.

The situation in 2018-2019 highlights the potential ambiguity of gold price. We see that gold is not insensitive to the US dollar. In the first stage of the tariff war in 2018, gold initially fell as the trade-weighted US dollar rose by 5%. However, as the momentum of the US dollar slowed down towards the end of 2018, gold began to recover, rising above the starting level of 2018 in early 2019.

3. In terms of immigration policy, former President Trump's agenda would be another disruption to the status quo, bullish for gold. Deutsche Bank believes that this may even outweigh concerns about inflation, as deporting immigrants will reduce demand and supply. It is noteworthy that immigration policy and deporting immigrants are listed as the top two items in Trump's policy agenda, while tariffs have not actually emerged. To facilitate the deportation of immigrants, Trump cited the Alien and Sedition Acts of 1798. The Act allows for the deportation of 'aliens,' but has only been used during wartime in the past.

There are two points to clarify. First, critics of expelling immigrants may argue that the executive branch is overreaching. This means unlike the tariff issue, the legislative branch can provide a balancing role. In the 'Red Wave' scenario, Congress may succumb to the potential Trump administration's immigration agenda. However, according to the Brennan Center for Justice, in cases of congressional disagreement, Congress is more likely to constrain executive power by repealing the law.

Secondly, if indeed expulsion is carried out according to the law, it could also be a slow process as the law requires a 'full review and hearing' in US courts before deportation. The law also allows for reasonable resolution of affairs and departure.

Deutsche Bank believes that after Trump wins, there will be another clear divergence in foreign policy favorable to gold. Compared to Harris's status quo, Trump's public statements indicate his different attitude towards foreign policy.

Major differences include Trump's proposal to stop US aid to Ukraine, skepticism towards NATO, including doubts about the US commitment to collective defense, and reducing US involvement in NATO.

On the Iran issue, Trump has historically taken a more adversarial position, withdrawing from the JCPOA nuclear agreement in 2018 and reintroducing sanctions on Iranian crude oil, reducing Iranian production and exports by nearly 2 million barrels per day between 2018 and 2020. With Iranian crude oil exports rising again since 2022, Trump may lean towards tightening sanctions enforcement.

Harris is likely to endorse a different approach. In 2018, she criticized the US withdrawal from the JCPOA as 'reckless' and in 2019 expressed intentions to rejoin the JCPOA, stating, 'It's an agreement that can prevent Iran from obtaining nuclear weapons.'

On the issue of Ukraine, Trump criticized the scale of US security aid, implying that if elected, he would seek to terminate US aid and claiming he would swiftly arrange through negotiations to end the war.

In contrast, Harris is likely to continue providing assistance to Ukraine and pledge to 'stand firmly with Ukraine and our NATO allies.'

In Gallup's opinion polls, the divergence of confidence in the accuracy of the presidential election between the parties has widened to the highest level since at least 2004, at 10. Confidence among Republicans steadily declined from 55% in 2016 to 28% in 2024, while Democrats' confidence remained stable around 84%.

Similar party divisions have also emerged in expectations regarding election-related issues. More Republicans anticipate problems with illegal or fraudulent voting, while more Democrats anticipate problems with refusing to concede. Therefore, if Vice President Harris wins, there is certainly tail risk for gold, given the contested election results and potential need to extend the vote-counting period to resolve disputes.

The upward trend of gold will be strengthened by a Trump victory and interrupted by a Harris victory.

In short, Deutsche Bank believes that after a Trump victory, gold's initial reaction to the election results will be positive, mainly because his policies are seen as deviating from the status quo, bringing greater uncertainty. This, coupled with accelerated federal debt growth and the complexity of potentially ignoring the impact of tariffs on gold, will influence the market.

On the other hand, a Harris victory would mean a narrowing of the risk premium, but any selling pressure on gold is expected to be short-lived, as Asian imports and central bank demand will offset speculative futures outflows.