刺激方案体现出北京不计一切代价刺激经济和消费复苏的决心,与此同时,作为经济增长主要推动力的科技公司不太可能受到决策者的干预。阿里巴巴是中国主要的电子商务公司和云服务供应商,该公司有望受益于前述两个因素。阿里巴巴的资产负债表强劲,预期市盈率为10.7倍,股票仍然很便宜。

刺激方案体现出北京不计一切代价刺激经济和消费复苏的决心,与此同时,作为经济增长主要推动力的科技公司不太可能受到决策者的干预。阿里巴巴是中国主要的电子商务公司和云服务供应商,该公司有望受益于前述两个因素。阿里巴巴的资产负债表强劲,预期市盈率为10.7倍,股票仍然很便宜。Source: Barron's Chinese Author: Nicholas Jaskinski Evan Greenberg, CEO of Chubb Ltd, has a highly influential fan - Warren Buffet, CEO of Berkshire Hathaway. Berkshire Hathaway disclosed last month that it held 6% of the shares in Chubb, one of the world's largest insurance companies, by the end of 2023. Berkshire itself is a major participant in the insurance industry, but it is not the only buyer. In the past year, Chubb's stock return, including dividends, was about 40%, surpassing the S&P 500 index's total return of 25%, and making the company's market capitalization reach $110 billion. This increase in market capitalization reflects Chubb's outstanding performance, which is attributed to its prudent underwriting practices and conservative management of its investment portfolio of about $140 billion. The company's earnings per share increased by 48% in 2023 and its book value per share increased by 21%. Greenberg is the son of Maurice "Hank" Greenberg, the former CEO of American International Group (AIG). Greenberg worked at AIG for 25 years, rising through the ranks. He left the insurance company in 2000 and took over Ace Limited in 2004. The company merged with Chubb in 2016, the largest M&A in the property and casualty insurance industry at the time. Today, Chubb is the largest commercial insurance provider in the United States, and the company is also known for its high-end homeowner insurance for the wealthy. However, about half of the company's premiums last year came from outside the United States. Asia has always been a growth area where the company is bullish: Although Asia accounts for 40% of global GDP, the insurance industry accounts for only 26% of the global insurance market share. This gap is expected to narrow over time. Greenberg sits on the board of several nonprofits that focus on international and Asian affairs. Barron's recently interviewed Greenberg about his underwriting philosophy, the challenges of dealing with increasingly frequent climate disasters, and US-China relations. Following are the edited excerpts of the conversation.

Author: Theresa Revas

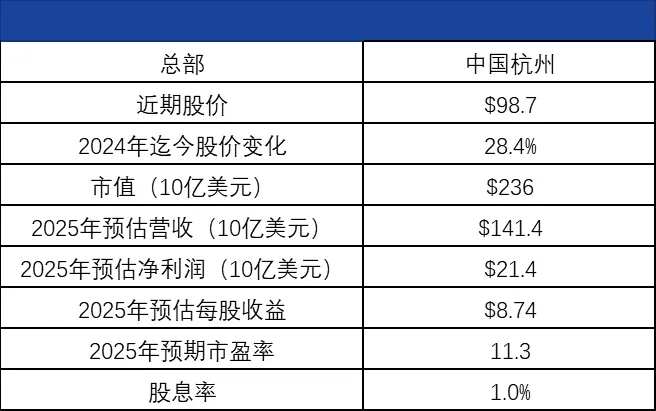

To promote sustainable economic growth, China recently introduced its largest stimulus package since the outbreak of the Covid-19 pandemic, leading to a sharp rise in the Chinese stock market. After experiencing several years of a downturn,$Alibaba (BABA.US)$under the stimulation of the package, it has regained vitality and increased by 25% in the past three months to $98.70. Some investors may wonder: is it too late to 'get on board' now?

The stimulus package reflects Beijing's determination to stimulate economic and consumer recovery at all costs, while tech companies, the main drivers of economic growth, are unlikely to be interfered with by decision-makers. Alibaba, China's leading e-commerce company and cloud service provider, is expected to benefit from the two aforementioned factors. Alibaba's balance sheet is strong, with an expected PE ratio of 10.7 times, making the stock still very cheap.

Burns McKinney, Senior Portfolio Manager at NFJ Investment Group, said, 'Alibaba's stock price is very cheap compared to historical levels and cheaper than other tech companies. The company has a large amount of cash and is creating more cash every day. Many bearish factors are turning into bullish ones.'

Burns McKinney, Senior Portfolio Manager at NFJ Investment Group, said, 'Alibaba's stock price is very cheap compared to historical levels and cheaper than other tech companies. The company has a large amount of cash and is creating more cash every day. Many bearish factors are turning into bullish ones.'

McKinney pointed out that investors are still somewhat hesitant to invest in China due to past government interventions, but Alibaba's stock price has already factored in these risks. McKinney believes that Alibaba's expected PE ratio could easily rise to 15 times. Based on a PE ratio of 15 and Wall Street's profit expectations for Alibaba over the next four quarters, the stock price would reach $138, an increase of 40%. If calculated based on the expected earnings for the next fiscal year, the stock price would reach $145, nearly a 50% increase.

Baird analyst Colin Sebastian pointed out that despite concerns about Chinese consumers, Alibaba's e-commerce core business market share continued to grow in the first quarter, with total commodity trading volume accelerating. Sebastian rates Alibaba's stock as 'outperforming the large cap,' and he believes that the first quarter performance indicates 'Alibaba is still in a transitional phase in many aspects.'

Wall Street generally expects that by 2025, Alibaba's EPS will show a recovery growth, with a year-on-year increase of 12.5% to $9.49, and revenue will grow by 8%. This will be the largest year-on-year growth in EPS that Alibaba has seen since 2021. Expectations are that online sales will grow as Alibaba balances consumer and merchant demands, rather than squeezing the latter like many competitors, which could lead to further growth and a greater boost. Derrick Irwin, portfolio manager of Allspring Global Investments' emerging markets stock team, believes that more high-quality merchants will favor Alibaba's platform, giving Alibaba an advantage in a crowded market.

Key data.

However, the real growth is in the field of cloud computing, with artificial intelligence currently driving growth in Alibaba's cloud computing business. Alibaba is the largest public cloud service provider in China and even the entire Asia-Pacific region. Currently, this business accounts for just over 10% of total revenue, but it is expected to become a significant driver of growth in the future.

Four years ago, Alibaba was the 'darling' of the market, with a P/E ratio close to 30 times. After the slowdown in the Chinese economy, Alibaba shifted from striving for growth at all costs to returning capital to investors willing to be patient. In the first two quarters of this year, Alibaba repurchased approximately $10 billion worth of stocks, with $26 billion in authorized repurchases still outstanding. Last year, the company set aside $16 billion for dividends and buybacks. Irwin said, 'Alibaba is focusing on executing specific details of a robust business, so if the Chinese economy recovers, the company will receive a significant boost.'

Alibaba's next rise may not be a straight line. As investors need to feel more confident about the growth trajectory of the Chinese economy, Alibaba's stock price will inevitably react to every data point and policy change in China. Currently, Wall Street analysts are also cautious; although 84% of analysts are bullish, the average target price is only $118.

However, Alibaba's rise is more about 'when it will rise' rather than 'if it will rise.' Even if Chinese consumers' willingness to spend increases only moderately, Wall Street will adjust Alibaba's target price upward.

NFJ's McKinnon said, "Alibaba is a good representative of China's middle class, the growth of the middle class has not stopped, it's just becoming more mature."

Alibaba's stocks are also the same.

Editor/Rocky