Source: CICC Commentary

Author: Zhang Jundong, Fan Li, Zhang Wenlang

With the expectation of a basic stable market and interest rate cuts in September [1], trading style has changed. After the June CPI and retail sales data were released, large-cap growth stocks led by AI concepts have clearly pulled back, while gold, small-cap stocks, and real estate, consumer, manufacturing, and bank-related stocks in the Dow have performed relatively well. The trading main line behind seems uncertain, and there has been a large discrepancy in the market's judgment on whether the US economy will have a "soft landing" or a "hard landing" after interest rate cuts. Is the market currently experiencing a short-term cut in style or a long-term change in style?

We believe that with the basic expectation of interest rate cuts being largely fulfilled, the space for interest rate cut trading ("buying on expectations") may be significantly squeezed, while the "cyclical trading" after interest rate cuts is gaining momentum (see "All kinds of interest rate cut trading are the same, but the trading logic after interest rate cuts is different"). Unlike interest rate cut trading, cyclical trading mainly prices the recovery of terminal demand and the restart of the economic cycle after interest rate cutting. Its supporting logic is the resilience of US household demand, large fiscal and re-industrialization, and more deeply, the "realization from empty to real" of the total scale and structural resilience of the US economy. Under the support of total-scale resilience of the economy, the interest rate cut may be relatively limited (that is, a "shallow" interest rate cut), which is more beneficial to the real economy, especially profitable-supporting enterprises, and has a relatively limited boost to valuation.

In terms of pace, Trump Trade 2.0 may accelerate the arrival of cyclical trading, given the increasing probability of Trump's recent election victory, stronger fiscal dominance (monetary coordination), industrial return, and potential weak US dollar in his policy ideology. At the same time, we also remind that due to the uncertainty caused by the election results, US stocks may enter a relatively high volatility period in the July-October of each election year; and after the uncertainty of the election dissipates, US stocks and bond rates often rise, and on average, value stocks perform better than growth stocks after the election (see "Major asset classes in US election years: seeking certainty in uncertainty").

Today's weather is good

Today's weather is good

In the third quarter of 2024, the actual GDP growth rate in the USA quarter-on-quarter annualized was 2.8%, slightly lower than the market's expected 3.0%, and a slight decline from the second quarter's 3.0%, but still a bright report. Specifically, personal consumption expenditure was strong, business equipment investment expanded, exports and government spending accelerated, indicating that the US economic growth remains healthy. Relatively weak areas include real estate investment and construction investment, showing that high interest rates are still having a restraining effect. In addition, inflation further declined in the third quarter, indicating that the US economy is heading towards a soft landing. We believe that the Federal Reserve does not need to significantly cut interest rates for now, expecting a 25 basis point rate cut next week, and whether to skip the rate cut in December will depend on the progress of inflation.

The quarter-on-quarter annualized growth rate of GDP in the USA in the third quarter saw a slight decrease compared to the second quarter, but domestic demand projects accelerated. Although the actual GDP growth rate of 2.8% quarter-on-quarter annualized fell slightly below the market's expected 3.0%, a key indicator of domestic demand - Final sales to private domestic purchasers - rebounded from 2.7% in the previous quarter to 3.2%, reaching the highest level this year. Final sales to private domestic purchasers include personal consumption expenditure and private fixed asset investment (excluding inventory). When government spending is also considered, the quarter-on-quarter annualized growth rate of domestic final sales in the third quarter increased from 2.8% in the previous quarter to 3.5%.

Looking at the specifics, personal consumption expenditure accelerated to its highest level since the first quarter of 2023. In the third quarter, the actual consumption quarter-on-quarter annualized growth rate was 3.7%, an increase from the previous quarter's 2.8%, contributing 2.5 percentage points to GDP. Among them, commodity consumption expenditure increased significantly by 6% on a quarter-on-quarter annualized basis, with durable goods consumption accelerating from 5.5% in the previous quarter to 8.1%, mainly driven by contributions from motor vehicles and parts, as well as leisure goods. Non-durable goods consumption also accelerated from 1.7% in the previous quarter to 4.9%. The growth rate of service consumption remained relatively stable compared to the previous quarter.

Fixed asset investment showed divergence, with equipment investment continuing to expand mainly due to strong investments in aircraft and information equipment. Real estate investment and construction investment were relatively weak, with a slight decrease in inventory. The growth rate of equipment investment accelerated from 9.8% in the previous quarter to 11.1%, contributing 0.6 percentage points to GDP. In terms of industry contributions, transportation equipment (+0.29 ppt) and information processing equipment (+0.24 ppt) made significant contributions to GDP, with the latter possibly reflecting capital expenditure related to artificial intelligence (AI), such as the construction of data centers and investments in related equipment. Real estate investment declined for the second consecutive quarter, indicating that the high-interest rate environment continues to suppress residential real estate. Construction investment declined, indicating that the stimulative effect of previous fiscal policies on the return of manufacturing is waning.

Fixed asset investment showed divergence, with equipment investment continuing to expand mainly due to strong investments in aircraft and information equipment. Real estate investment and construction investment were relatively weak, with a slight decrease in inventory. The growth rate of equipment investment accelerated from 9.8% in the previous quarter to 11.1%, contributing 0.6 percentage points to GDP. In terms of industry contributions, transportation equipment (+0.29 ppt) and information processing equipment (+0.24 ppt) made significant contributions to GDP, with the latter possibly reflecting capital expenditure related to artificial intelligence (AI), such as the construction of data centers and investments in related equipment. Real estate investment declined for the second consecutive quarter, indicating that the high-interest rate environment continues to suppress residential real estate. Construction investment declined, indicating that the stimulative effect of previous fiscal policies on the return of manufacturing is waning.

Looking ahead, US bond yields have risen since the fourth quarter, and 30-year fixed mortgage rates have rebounded, possibly continuing to limit the recovery of the real estate market. The Mortgage Bankers Association's (MBA) Home Purchase Index has been persistently low, indicating that real estate market recovery may not come as quickly in a slower rate-cutting environment. Equipment investment is still at a low level, with non-AI equipment investment yet to recover, waiting for signals of a global economic cycle restart. Additionally, the policy direction of the new government after the US presidential election will also impact equipment investment. If the new president adopts tariff measures, it may not be conducive to manufacturing recovery.

In terms of trade, both imports and exports have accelerated compared to the second quarter. The growth in imports partly reflects advance stocking by merchants. The drag from net exports on growth narrowed from 0.9 percentage points in the second quarter to 0.6 percentage points. The strike by dockworkers at the end of the third quarter may have led some retailers to stock up early, and concerns about tariffs may have spurred imports, causing disruptions in trade data. Additionally, capital goods imports such as computers and computer equipment have shown strong growth this year, which corroborates the investment driven by AI mentioned earlier.

Another indicator worth noting is the significant acceleration in government spending, mainly driven by defense expenditures. In the third quarter, the month-on-month annualized growth rate of US government spending accelerated from 3.1% in the previous quarter to 5.0%. Among them, the month-on-month annualized growth of federal government spending increased by 9.7%, the fastest growth since the first quarter of 2021. After a 6.4% growth in defense military industry spending in the previous quarter, it further increased by 14.9% in the third quarter, the fastest growth since 2003. This is partly related to the legislation passed by Congress to assist Ukraine. Non-defense federal government spending also accelerated to the highest level this year, partly due to increased spending by the current government before the election. Looking ahead, inertia may exist in US government spending, making it difficult to transition to fiscal order consolidation.

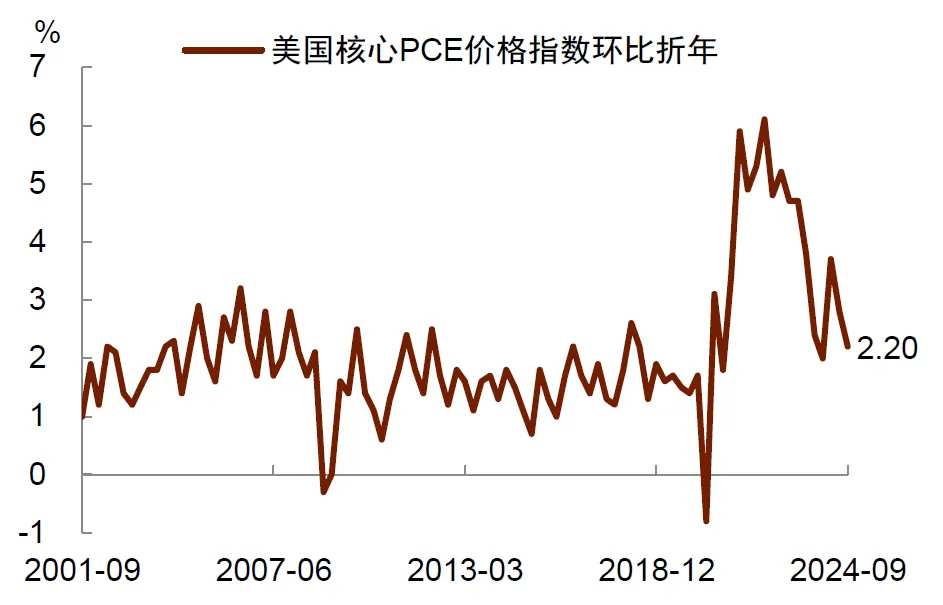

GDP data does not support a significant rate cut by the Federal Reserve. We expect the Fed to cut rates by a maximum of 25 basis points next week. In the third quarter, inflation continued to decline, with the month-on-month annualized growth rate of PCE falling from 2.5% in the previous quarter to 1.5%. The core PCE's month-on-month annualized growth rate also decreased from 2.8% in the previous quarter to 2.2%. Combining robust growth data, it shows that the US economy is still on track for a soft landing. With healthy economic growth and a stabilizing labor market, the necessity for the Federal Reserve to further aggressively cut rates is low. We expect the Fed to likely take a relatively cautious policy stance at next week's FOMC meeting, most likely implementing a moderate rate cut of 25 basis points, while retaining policy flexibility. Skipping a rate cut in December will depend on the progress of inflation.

Chart 1: US domestic demand remains robust, with accelerated rebound in the third quarter

Chart 2: Core PCE inflation slows month-on-month annualized to 2.2%

Editor / jayden