The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, Douglas Dynamics, Inc. (NYSE:PLOW) does carry debt. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company's use of debt, we first look at cash and debt together.

What Is Douglas Dynamics's Debt?

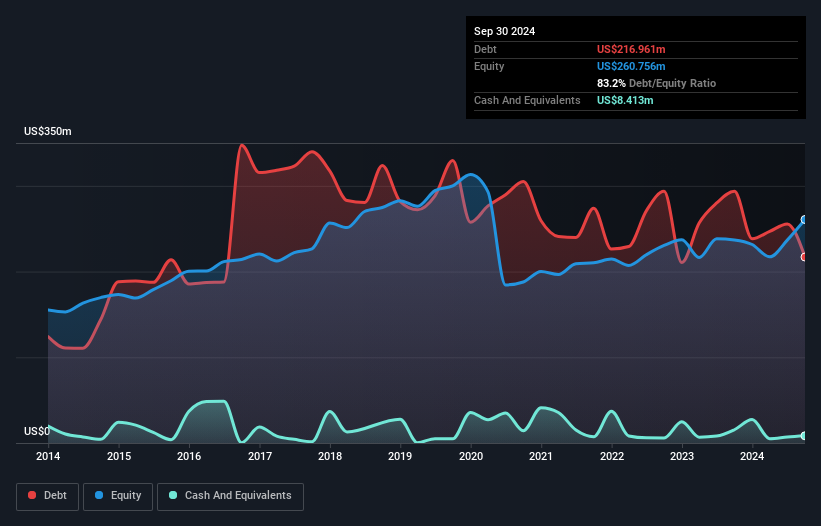

As you can see below, Douglas Dynamics had US$217.0m of debt at September 2024, down from US$293.6m a year prior. However, it also had US$8.41m in cash, and so its net debt is US$208.5m.

How Strong Is Douglas Dynamics' Balance Sheet?

We can see from the most recent balance sheet that Douglas Dynamics had liabilities of US$147.5m falling due within a year, and liabilities of US$257.3m due beyond that. Offsetting these obligations, it had cash of US$8.41m as well as receivables valued at US$153.1m due within 12 months. So its liabilities total US$243.3m more than the combination of its cash and short-term receivables.

We can see from the most recent balance sheet that Douglas Dynamics had liabilities of US$147.5m falling due within a year, and liabilities of US$257.3m due beyond that. Offsetting these obligations, it had cash of US$8.41m as well as receivables valued at US$153.1m due within 12 months. So its liabilities total US$243.3m more than the combination of its cash and short-term receivables.

Douglas Dynamics has a market capitalization of US$601.8m, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Douglas Dynamics has a debt to EBITDA ratio of 3.1 and its EBIT covered its interest expense 2.9 times. Taken together this implies that, while we wouldn't want to see debt levels rise, we think it can handle its current leverage. Even more troubling is the fact that Douglas Dynamics actually let its EBIT decrease by 3.4% over the last year. If that earnings trend continues the company will face an uphill battle to pay off its debt. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Douglas Dynamics's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. In the last three years, Douglas Dynamics's free cash flow amounted to 45% of its EBIT, less than we'd expect. That's not great, when it comes to paying down debt.

Our View

Douglas Dynamics's interest cover was a real negative on this analysis, although the other factors we considered cast it in a significantly better light. But on the bright side, its ability to to convert EBIT to free cash flow isn't too shabby at all. Taking the abovementioned factors together we do think Douglas Dynamics's debt poses some risks to the business. So while that leverage does boost returns on equity, we wouldn't really want to see it increase from here. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. These risks can be hard to spot. Every company has them, and we've spotted 2 warning signs for Douglas Dynamics (of which 1 is concerning!) you should know about.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.